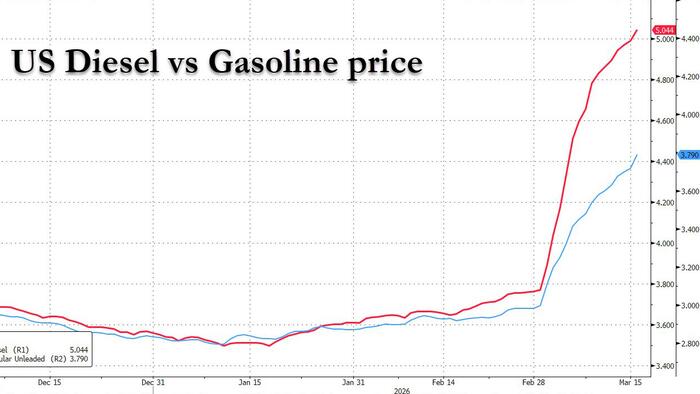

While US gasoline prices have risen substantially since the start of the Iran war (although RBOB futures suggest there is much more upside should oil prices remain around $100), the average price of diesel has already soared above $5 per gallon in the US, the highest since 2022, and pushing up supply chain costs and setting the stage for broader inflation for consumers.

The price spike is increasing costs for farmers, truckers and construction firms.

With diesel at $5 per gallon, these industries are on track to spending around $6.1 billion this week on the fuel, according to BloombergNEF forecasts.

The same amount of fuel would have cost just $4.5 billion ahead of the war, a 35% increase.

According to BNEF, road diesel accounts for roughly 66% of US diesel consumption, with large trucking fleet operators like Walmart and Amazon highly exposed to fuel cost swings.

The fuel also powers agricultural machinery, ships and trains hauling goods across the country.

The widespread use of diesel feeds into the cost of goods across the economy.

However, unlike gasoline, where consumers feel the pinch immediately at the pump, the higher diesel costs show up indirectly over time.

Rapidan Energy’s Director of Refined Products, Linda Giesecke, offered insight into the diesel market:

Diesel prices have surged globally to levels last seen since 2022, when Russian exports were at risk. But unlike 2022, the current tightness reflects physical supply disruptions rather than policy risk and trade reshuffling.

Because of the Hormuz outage in the Gulf, global diesel prices are on track to average about $150/bbl this month. That’s a 60% increase vs. February, vastly outpacing crude’s 40% rise to near $100, with diesel’s price risk skewed sharply to the upside – especially if Hormuz reopening takes longer than the early-April timeline we assume in our base case.

We have global diesel prices easing toward $120/bbl in April, but only if shipping flows begin to normalize. If Hormuz flows do not resume in the coming weeks and diesel prices remain at $150/bbl into the second quarter, global economic growth will suffer because of diesel’s close link to industrial production and freight activity.

As the war on Iran extends into the third week and oil prices remain elevated, inflation pressure in the US will likely broaden beyond fuel and into consumer goods.