We’d appreciate your input on a few questions about environmental and energy policy. This brief survey should only take one minute to complete.

Your responses will help us better understand different perspectives on these important issues. All responses are confidential.

Welcome to Dispatch Energy! The Trump administration has been betting big on energy dominance achieved through the nation’s vast reserves of fossil fuels, so how has that been going? In a word, “meh,” as American fossil fuel industries under the second Trump term seem to be faring worse than under the first. This could be just a temporary blip in the data, but it also points to the possibility that the new administration’s executive-heavy approach introduces new risks to energy investors.

My boss at the R Street Institute has a saying I’ve grown fond of: “Make America burn whale oil again.” While ridiculous, it pithily captures why approaching energy policy through a lens of technological tribalism is bad economics. The joke came about during the first Trump administration, when officials were contemplating market interventions to force increased consumption of coal and nuclear power—a move that they eventually backed away from in favor of a more conventional, limited-government approach. But the second Trump administration has taken the opposite tack and is aggressively pursuing market interventions to bolster its favored energy sources of oil, coal, and natural gas. Naturally, this approach raises the question: Are Americans, or even those industries, faring better than they did during Trump’s first term?

The administration’s energy market actions are too numerous to list. But, put simply, if the first Trump administration’s motto was “end the war on coal,” then the current Trump administration’s motto is “wage war against every energy source we don’t like.” Some highlights include using the Defense Production Act to subsidize the production of critical minerals, and then designating coal a critical mineral; creating an “alternative” federal permitting arrangement for energy sources that are not wind or solar; and, of course, revoking previously issued permits for renewable energy projects.

While I’ve always been skeptical of anyone who claims to know President Donald Trump’s motives, it seems to me that the administration’s actions are colored by over-ascribing current market conditions to the policies of Presidents Joe Biden and Barack Obama. Many conservatives have latched onto a persistent narrative that says the only reason renewable energy is used at all is because of subsidies, regulations, and mandates. More even-keeled economists argue that while these policies have aided renewables, they only partially explain their growth in recent years. Another factor is that good old-fashioned productivity gains lower costs and make these energy sources more competitive. My own research has shown that subsidies have been very inefficient at stimulating the deployment of renewable energy.

California oil family: “We can’t drill new wells”

Imagine waking up to learn the government blocked your access to your own oil-rich land. The mineral rights that have been in your family for generations are suddenly worthless.

That’s the nightmare John and Melinda Morgan have faced since California enacted a sweeping ban on oil and gas drilling. Tune in below to hear from John Morgan on what it’s like to get hit by government overreach—and how to hit back.

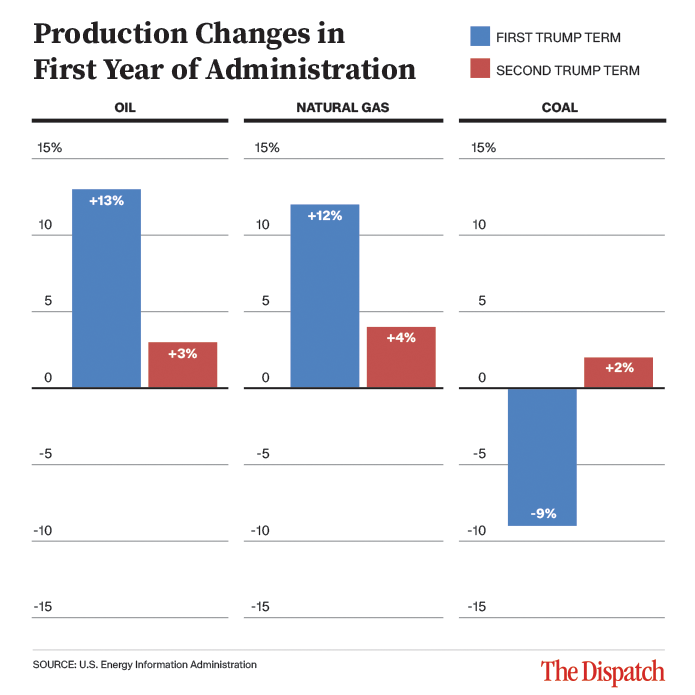

Unfortunately, the current administration seems to have bought into the idea that government interventions are very effective at propping up renewables, so applying the same policies to fossil fuels ought to have similar benefits. Let’s check the data and see if that is happening. The following chart shows the year-over-year change in fossil fuel production during the first year of the first and second Trump administrations.

While oil and natural gas enjoyed a renaissance under the first Trump administration, production has not grown as much under Trump 2.0. This trend is particularly interesting for natural gas, which has risen in price. Coal is the only industry that seems to be doing better under the second Trump administration than the first, but it’s worth noting that coal output is so low relative to historical highs that the actual volume of recent increase is negligible compared to coal’s overall decline (the U.S. went from producing 68 million short tons in January 2017 to 46 million short tons in January 2026). But of course, a year-over-year snapshot should always be taken with a grain of salt, as many factors can affect energy production from one month to the next.

Beyond the data, the administration has made several announcements unveiling new fossil fuel projects, including coal mines, natural gas plants, and refineries. However, these events haven’t caught up to the market yet. It is possible that, given more time, these projects will come to fruition and vindicate the administration’s energy strategy.

It could be that we are just too early into the Trump administration’s fossil fuel revival strategy to see much success. But there is an alternative explanation: Government interventions are just bad at stimulating productivity growth. We have a lot of experience on this front. Simply put, politicians operate with limited information and tend to be worse decision-makers than investors who have skin in the game.

One other and perhaps underappreciated point is that because of how the administration implements policy actions—primarily via executive orders and new regulations—there is a cloud of uncertainty over the very industries it is seeking to bolster. The fossil fuel industry is likely worried that this administration’s executive orders could be just as easily erased by a subsequent administration’s executive orders, which is particularly important given that building new infrastructure requires permits and investments that live beyond the remaining years of the Trump administration.

These policies were implemented too recently to evaluate them empirically. But one point of evidence that the administration’s interventions may be creating more risk than reward for the fossil fuel industry is that many of the large new projects mentioned earlier are backed by foreign investors. If the U.S. is on the precipice of a fossil fuel renaissance, we would expect American capital to flow to fossil fuels, yet the financing is coming from countries that may have ulterior motives for their investments (such as averting higher tariffs or staying under the American security umbrella).

It’s important to remember that the policies Trump is using to assail renewable energy and prop up fossil fuels can be inverted. Investors who could be harmed by such moves—like oil and gas producers leasing from federal land, or exporters who require permits for liquefied natural gas terminals—would probably see the administration’s current strategy as risky for them in the long run. And the closer we get to the next general election, the more the policies of the next administration will be top of mind for industry. The fossil fuel industry is likely worried that the White House is building the very machine that will be used to destroy it.

More to the point, Americans just don’t seem to feel like things are getting better right now. As Jonah Goldberg recently noted, Americans today are much less satisfied with the economy than they were during Trump 1.0. A simple explanation could be that the first Trump administration relied on traditional establishment Republican free-market economic principles, and the second one has rejected those themes in favor of a more active government role.

Basic economics remain true regardless of who is in power or what policies are applied. Critiques of government interventions are rooted in the notion that the remedy for scarcity in the economy is to let innovators find ways to produce, and government interventions that either create red tape or prop up specific industries distort investments and lead to suboptimal allocation of capital. Notice that this theory holds true regardless of which technologies government officials are restricting or favoring. Central planning makes for bad energy policy, even if aimed at boosting the “correct” industries.

Before Trump was reelected, he promised to cut utility bills in half. Instead, residential prices rose 9 percent between January 2025 and January 2026. To the extent that presidents have the power to influence utility bills, the reason for this failure is probably policy. In his first term, Trump promised to surround himself with the “best” people to get the job done, and the economic successes during that time would show that, to a certain extent, he did. It is no accident that Trump not only beat Kamala Harris in the 2024 election but overperformed in practically every voter category, as Americans reckoned with the fact that four years of Bidenomics had failed. But Trump has not emulated the economic successes of his first term, and polling certainly reflects that: A majority of Americans believe that the president’s policies have made the economy worse. Energy affordability—which used to be one of Republicans’ strongest issues—is now polling in favor of Democrats.

To sum it all up, fossil fuels are gaining some advantages from Trump’s favorable posture toward them—but not enough to offset the headwind against the necessary long-term investment that’s created by the president’s interventions. This investor fear is reflected in production data, which shows slower gains under Trump 2.0 than his first term despite market conditions that should be favorable to new producers.

Thankfully, if the White House does seek to course-correct, the fix is quite simple: Restore the power of markets, rein in the ability of current and future politicians to interfere in the economy, and focus on big-picture data rather than using the government to negotiate deals on behalf of industry. In short, adopt the policies of the first Trump administration.

Policy Watch

- As Iran continues to throttle tanker traffic through the Strait of Hormuz, Ukraine is concerned about the resulting boost in Russian oil revenue as global buyers seek out alternative suppliers. In apparent response, the Ukrainian military has ramped up its attacks on Russian oil infrastructure. Russian oil sales represent a relatively sanctions-resistant source of revenue because the resource can be traded in foreign currencies, allowing the Kremlin to fund the country’s military.

- The natural gas industry is optimistic that Congress may be closing in on a permitting reform deal over the next few months, according to a recent report by S&P Global. This news comes as Democratic Sen. Sheldon Whitehouse of Rhode Island, the ranking member of the Senate Environment and Public Works Committee, resumes negotiations with Republicans toward a deal that makes it easier to build energy infrastructure. Talks had repeatedly stalled amid Whitehouse’s refusal to negotiate in response to the Trump administration’s decision to rescind permits for five offshore wind projects, which have since been restored following court rulings.

Innovation Spotlight

- Glomar Minerals, a deep-sea mining firm founded in 2025, and the Australian mining company Cobalt Blue recently announced a plan to build a refinery in the United States to process critical minerals extracted from proposed undersea mines in the Pacific Ocean. If the project comes to fruition, it would mark the first time that the U.S. could tap into undersea sources for its mineral supply. Relatedly, the Rainier—a research vessel operated by the National Oceanic and Atmospheric Administration—plans to conduct surveys of undersea critical mineral deposits in the Pacific Ocean beginning in early April.

Further Reading

- Dispatch Energy contributor Lynne Kiesling recently co-authored a research paper examining the causes of decarbonization in the power sector. For her Substack Knowledge Problem, Kiesling explains her core findings, which show that while cheaper natural gas and clean energy subsidies have contributed to clean energy growth, there are other important market factors at play. A big factor determining whether grids have gotten cleaner is their participation in wholesale markets, showing that the competitiveness of electricity markets is an underappreciated variable for clean energy growth. As Kiesling notes, “Electricity markets determine how generators compete, how prices convey information, how dispatch works, how new technologies enter, and how investment incentives are structured. Those institutional features are part of the mechanism through which the generation mix changes.”

ICYMI: On Tuesday, Pacific Legal Foundation hosted a live debate between Dispatch Energy contributors—Alex Trembath and Roger Pielke Jr.—on the future of American energy policy. Watch the full debate here.