Housing affordability was one of the hottest political issues during the past year, so it’s not much of a surprise that the administration is now staking out a formal position. Yet given President Donald Trump’s real estate background, it is striking just how populist the administration’s new executive order on housing sounds.

The executive order’s title reads as if it were crafted by a disciple of Sen. Elizabeth Warren: “Stopping Wall Street from Competing with Main Street Homebuyers.” But, no, it was authored under the direction of a man who, strangely enough, made his fortune borrowing money on Wall Street. And stranger still for a Republican administration, the order directs federal agencies to define and curb large institutional investors’ purchase of single-family homes.

Not that a higher market share would necessarily indicate a problem, but large institutional investors own fewer than 1 percent of America’s homes. The share rises to about 5 to 10 percent in a handful of counties (less than one-tenth of a percent of counties), but most institutional investors invest in diverse portfolios, not single assets. The evidence also shows that, in 2025, there was less institutional interest, and small investors (owning fewer than 11 homes) made up about 90 percent of all investor-owned homes. It’s very difficult to see any kind of big problem here.

Still, nothing stirs up emotional angst like the evil specter of Wall Street, so politicians keep right on evoking it, regardless of what the data show.

Interestingly enough, the executive order still leaves many details to be decided, and it doesn’t quite seem to be the outright “ban” the administration had been floating. The administration doesn’t seem to have the authority to pull that off, so it did the next best thing—it directed federal agencies and the government-sponsored enterprises to stop insuring and securitizing mortgages that were acquired by “large institutional investors of a single-family home that could otherwise be purchased by an individual owner-occupant.”

The problem, there, for starters, is that the agencies now have a ton of room to define “large” and “institutional investor” however they like, possibly cutting out all kinds of investors. Treasury Secretary Scott Bessent did try to calm everyone’s fears by saying that the administration doesn’t want to push out “mom-and-pop” investors, but it wasn’t very reassuring.

Just who are these mom-and-pop investors whose money is still good?

Nobody knows for sure, but Bessent, who once owned this $22.25 million house in Charleston, South Carolina, and has bought and sold at least 20 properties in multiple states, thinks it might be people who bought “maybe 5, 10, [or] 12 homes.” The administration doesn’t want to keep those folks’ money out of the market; it just wants to push out “everyone else.” It’s hard to believe a Wall Street veteran like Bessent believes in this kind of rhetoric. If a mom, a pop, or any other American owns shares in a mutual fund, their money goes somewhere. Sometimes even, yes, into single-family home investments.

As policy, Trump’s move to restrict large investors from buying homes is one long past its sell-by date. Aside from its various inconsistencies, the policy largely died back in 2021 shortly after Democratic lawmakers started promoting it, partly because house prices started declining.

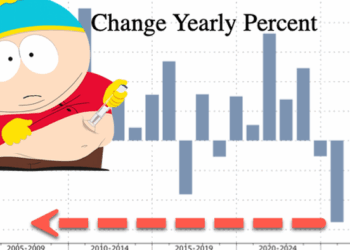

Yes, home prices spiked during the pandemic, but average new home prices actually peaked in 2022, and by October 2025 they were about $70,000 lower than the peak. The number of weeks of wages needed to cover the full price of a home is at its lowest point since 2020, and it’s now lower than during much of the 2010s. In October 2007, it took 324 weeks of wages to afford the full price of a home. In October 2025, that figure was 312. In fact, across several categories, median housing cost as a share of income has been flat or decreasing since the pandemic. (The 30-year mortgage rate is even down almost 2 percentage points since its peak in 2023.)

The other reason Democrats lost the policy battle over institutional investors’ involvement in the housing market in 2021 is because the whole idea was based on little more than misplaced anger at Wall Street. Large institutional investors own a very small share of America’s homes, and the notion that private investment in housing harms the market was—and still is—ludicrous.

For starters, if investors are buying these homes to rent because it’s a profitable business, then that’s great news. It’s a mystery why this administration would be flat-out against earning profit in the real estate market.

For a refresher: Profit is good. If people can profit from investing or running a business, it signals that people are meeting the needs of others. But that’s not the real issue. The issue is that politicians have successfully sold the idea that buying a home is always better than renting and, without a coherent policy to effectuate that, have decided to throw the kitchen sink at the issue. But their initial assumption is erroneous: Indeed, for many people, renting is the better option.

In general, renting is almost always a better option for people who live in an area for less than 10 years due to many of the unique costs associated with buying. Moreover, renting typically offers more flexibility to relocate when needed, as well as the ability to better diversify one’s investments, thus minimizing financial risks for many people.

If the administration (and Congress) want more abundant and affordable homes, for rent or purchase, they shouldn’t enact policies that keep investors’ funds out of the market. They should want the opposite, in fact: Those investments create the incentive to increase supply, which puts downward pressure on prices.

At the same time, the administration apparently sees no contradiction between shutting institutional investors out of the market for single-family homes and calling for policies that will simultaneously boost demand, further worsening the affordability problem. The administration wants, for instance, to manipulate interest rates and home prices by having Fannie Mae and Freddie Mac purchase another $200 billion in mortgage-backed securities.

So, on the one hand, the administration views real estate as a profitable thing, and it doesn’t like that. And on the other, it’s doing everything it can to boost demand for real estate. It doesn’t make much sense.

The administration has a chance to move federal housing policy in a good direction, with less government involvement and subsidies that artificially boost demand and home prices, but it appears to be lost. It’s fallen victim to the Washington, D.C., housing conundrum: Housing should be more affordable, politicians say, but everyone should own a home to build their wealth.

Whether the administration can succeed in allowing the housing market to operate efficiently depends on whether it can finally dispense with that fiction.