Life, Liberty, Property #136: Are the Fears About the Economy Justified?

Forward this issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

- Are the Fears About the Economy Justified?

- Video of the Week: SCOTUS to Kill Climate Lawsuits? – The Climate Realism Show #192

- Trump Proposes a New Entitlement

Space is limited, so act now!

Are the Fears About the Economy Justified?

Recent press reports and public-opinion poll results widely declare that the U.S. economy is in worse condition than it was in 2021 through 2024. This impression prevails despite reports of very high gross domestic product growth and falling inflation in the second and third quarters of last year, in the wake of slower growth and steady inflation numbers in the fourth quarter.

Overall, the U.S. economy is not yet where it should be, though the doom talk today is overstated and politically motivated. What is most damaging about the mismatch between today’s economic myth and reality is the false conclusions about economic policy its advocates send.

In framing the issue before President Donald Trump’s State of the Union speech last week, The Wall Street Journal typified the current winter of discontent:

The speech comes amid polling that shows voters are dissatisfied with the economy and concerned about costs. Political strategists of both parties warn those frustrations could translate into Republican losses in November’s elections. The president’s top advisers have encouraged him to focus on affordability, a message that Trump has sometimes resisted.

… While some positive signs have emerged, including cooler inflation, government data released this past week showed U.S. economic growth slowed sharply at the end of last year.

Voters have taken an increasingly negative view of Trump’s job performance since his first speech to a joint session of Congress last year. Some 41% currently approve of how he’s handling his job, with 57% disapproving, an average of polls tracked by the nonpartisan Cook Political Report finds. Last March, disapproval outweighed approval by 2 points, compared with the 16-point gap today.

The upcoming midterm elections are the obvious context for the doomsaying about the economy. For me, the question at hand is what the current state of the economy indicates about economic principles and what policy course the United States should take for the future. The two broad alternatives are more government intervention and economic management or greater economic freedom. Let’s look at the numbers with that in mind.

The topline data are always those for unemployment and inflation, especially because those are the numbers the Federal Reserves uses to determine how to deploy its currency manipulation to fine-tune the nation’s economy in line with its dual mandates to manage those two factors.

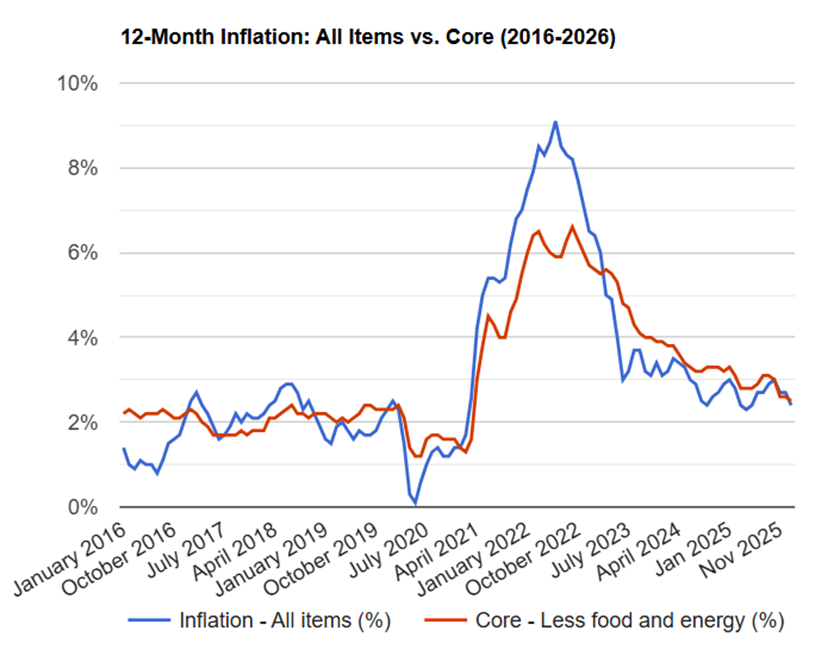

Inflation has come down far from its mid-2022 peak of 9.1 percent (as measured by the Consumer Price Index, or CPI), though progress has stalled since May of last year. Month-over-month inflation cooled to a 0.2 percent annual rate last month, with a notable moderation in prices of food (a 0.2 percent month-over-month rise, after a 0.7 percent increase in December) and fuel (a 3.2 percent decline in January after a 0.3 percent decrease in December). Headline inflation was 2.4 percent for the 12 months ending in January. (All these numbers are available at The Inflation Calculator website.)

Food and fuel are known as volatile components of the inflation rate, meaning they change more rapidly than other elements of the calculation and hence can obscure the underlying story of how rapidly the money supply is changing with respect to the supply of goods, services, investment, etc. Reported inflation of core consumer prices, which excludes those factors, was 0.3 percent in January, above the 0.2 percent December increase. Core inflation was 2.5 percent over the past twelve months, the lowest since March 2021:

Source: U.S. Inflation Calculator

January’s headline inflation rate was the lowest since May of last year and a tenth of a percentage point below economists’ expectations. Reported inflation remains above the Fed’s goal of 2 percent per year.

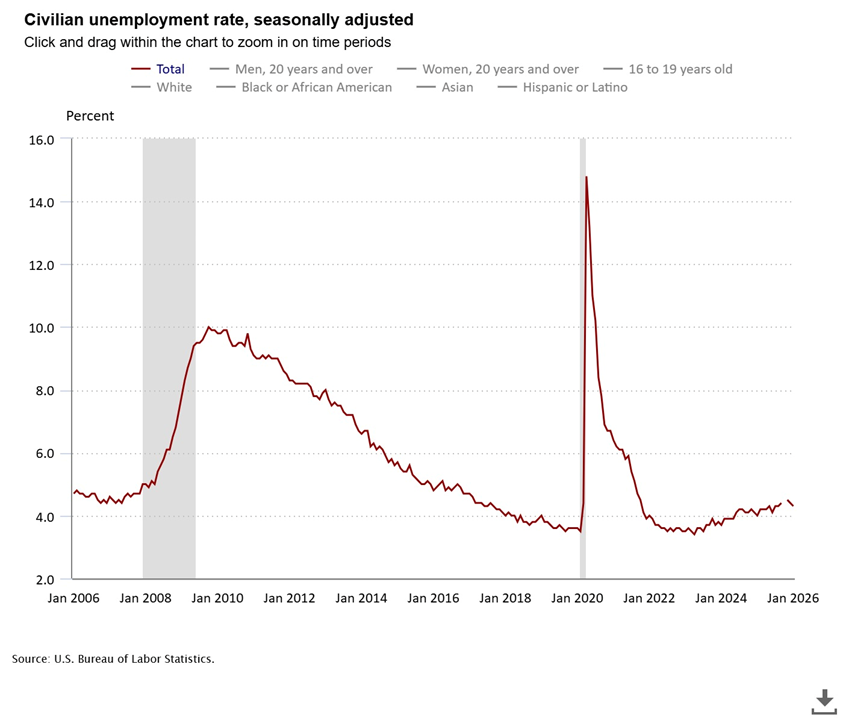

Through January, the unemployment rate was middle-of-the-road, neither alarmingly high nor encouragingly low, though continuing a reversal of the pre-pandemic trend that has now lasted three years:

Critics of the current economy are characterizing this normal but rising unemployment rate as a bad sign. “The U.S. labor market is facing another year of sluggish hiring and a further increase in the unemployment rate, a leading economist has warned,” Newsweek reported in January. This widely predicted increase in unemployment has been scaring the public, as it should if true. Thus, Newsweek reports,

Months of weak hiring have fueled fears that the U.S. labor market is in a prolonged slowdown, with surveys also charting widespread unease about its underlying strength. While many are forecasting that current conditions will persist in 2026—alongside the “low hire, low fire” trend diagnosed by Federal Reserve Chair Jerome Powell last year—some say the 2025 surge in job cut announcements could upset this fragile equilibrium and push unemployment sharply higher in 2026.

… According to the latest employment report from the Department of Labor, the economy added just 50,000 jobs in December, well below historical averages and making 2025 the weakest year for job creation since the pandemic.

The story extensively quotes a blog post by Moody’s Analytics Chief Economist Mark Zandi arguing that the current unemployment rate shows the U.S. economy is weak and heading down:

The fragility of the economy’s growth is evident in the job market. There is little to no job growth, and unemployment is on the rise. Since President Trump announced hefty reciprocal tariffs on nearly all countries this past April, job growth has come to a near standstill. Trade-sensitive industries, including manufacturing, agriculture, transportation and distribution, are suffering job losses. Health care is the only major industry still adding significantly to payrolls. And the job market’s difficulties will come into even sharper relief as the jobs data are ultimately revised down.

Those predictions proved wrong in January, as total nonfarm employment rose by 130,000 and the unemployment rate “changed little,” at 4.3 percent, according to the Bureau of Labor Statistics (BLS). Federal government employment decreased by 34,000, which means a transfer of workers out to the productive private sector. Federal Reserve Governor Christopher Waller called the job report “a surprise to the upside” that “suggests that the labor market may be turning a corner.”

Employment continued to rise in February, Ph.D. economist Robert Genetski reported in his weekly newsletter on Friday: “ADP’s job data show employment continues to improve. The four weeks ending February 13 reported total employment increased by 51,000 jobs This is up from an increase of 22,000 ADP jobs for the month of January.”

Unemployment remains nearly a percentage point above the recent low of 3.4 percent in January and April of 2023, the lowest in 55 years. It rose to 4.1 percent in December 2024, close to where it ended up in January of this year. The important question is whether the current unemployment rate indicates weakness in the U.S. economy. The short and correct answer is that it does not.

Unemployment is generally a lagging indicator of economic conditions. It tends to be the last thing to rise when the government and central bank inflict economic damage, and it is usually among the last things to return to normal after those agents of misfortune relent on the policies that caused the trouble.

“Quant Hacker” outlines this very well at his Substack:

First and foremost, one of the fundamental flaws of using the unemployment rate as a tool for market forecasting is its nature as a lagging indicator. A lagging indicator is one that reflects changes in the economy after those changes have already occurred. The unemployment rate, in particular, tends to rise after the economy has already entered a downturn and, conversely, it typically begins to fall well after economic recovery is underway.

For example, Loungani, Rush, and Tave (1990) found that stock market declines can actually cause unemployment to rise, reinforcing the idea that the unemployment rate reflects past economic damage rather than providing early warnings. By the time unemployment rises significantly, the worst of a downturn may already have passed. …

Consequently, “when compared to other economic variables, the unemployment rate lacks the predictive power necessary to serve as a robust market forecasting tool,” Quant writes.

This bulleted list from the StemTA company identifies specific factors that slow the reaction of unemployment to changing economic conditions:

Here are five reasons why the unemployment rate is a lagging indicator:

- Hiring and Firing Delays: Companies typically react to economic changes with a delay. During an economic downturn, businesses might take time before laying off employees, and similarly, they may be cautious about rehiring until they are confident in a recovery.

- Reporting and Data Collection: The process of collecting, analyzing, and reporting unemployment data takes time, resulting in a delay between the actual economic events and their reflection in the unemployment rate.

- Labor Market Inertia: The labor market doesn’t adjust immediately to changes in economic activity which is why the unemployment rate is a lagging indicator. Workers may remain unemployed for extended periods, and job creation may be slow even after economic recovery begins.

- Government Policies: Interventions such as unemployment benefits and job protection laws can influence the unemployment rate by either delaying layoffs or supporting employment during economic downturns, thus not reflecting immediate economic conditions.

- Structural Changes: Shifts in industry demand or technological advancements can affect employment patterns over time, leading to the unemployment rate [being] a lagging indicator as the workforce adjusts to new realities.

The economic trends and reversals of the past five years make sense when we view unemployment as a lagging indicator of economic health. The inflationary federal-deficit expansion in 2021 and 2022 created sharp inflation almost instantly. Higher business costs caused by inflation and the harsh tightening of regulation throughout 2021 through 2024 began pushing up the unemployment rate in 2023, as the BLS chart above shows.

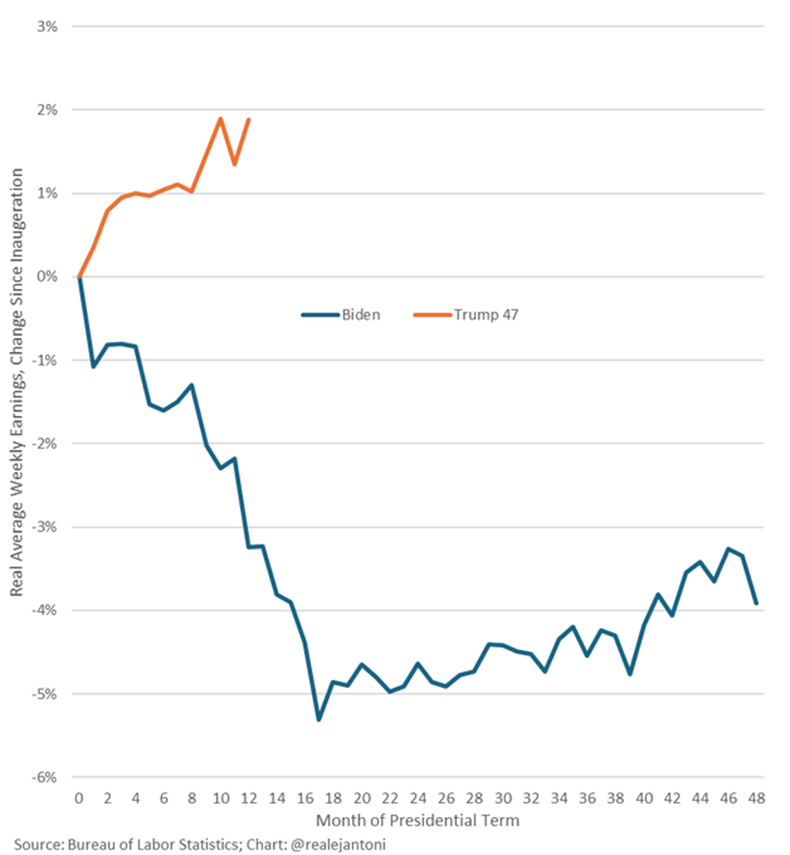

Unemployment has yet to move down much since then. Meanwhile, inflation has receded, private-sector employment is rising, and GDP has been growing. Real wages for U.S. private-sector workers rose by almost $1,400 in 2025, after having fallen by $3,000 in the prior four years, which was compounded by the 21.5 percent rise in prices during that period. The last two numbers concisely identify the cause of the affordability crisis.

Now the “[a]verage American’s weekly paycheck buys ~2% more than it did 1 year ago when Trump was inaugurated, after falling ~4% during the Biden years,” writes Heritage Foundation economist E. J. Antoni at X:

The lack of improvement in the unemployment rate does not contradict the fact that the U.S. economy has improved in the past year. CNN Business Executive Editor David Goldman reports that the economy is doing well overall:

Jobs, wage growth, consumer spending and inflation under Trump look pretty decent or have been mostly stable. The stock market is near a record high.

The US economy grew 2.2% in 2025, very much in line with the last three years of robust economic growth. The economy slowed down more than expected at the end of the year, but the longest-ever government shutdown stymied growth that should be made back this quarter.

The Atlanta Fed now estimates that first quarter 2026 economic growth will be a solid 3 percent. Goldman continues his assessment of the economy by addressing unemployment, along with inflation:

Last year wasn’t a great year for the labor market by any stretch. But unemployment remains low, and stronger-than-expected hiring in January suggests 2026 could be a much better year for job creation.

Inflation appears to be on the downswing again after a bumpy ride in 2025. And paycheck growth has been outpacing inflation for nearly three years, helping Americans stretch their dollars further.

Goldman argues that the U.S. economy is currently not as healthy as Trump claims, because affordability remains a problem for most Americans, though it is better than the president’s detractors say.

An accurate gauge of the overall health of the economy is critically important in light of the federal government’s assumption of authority and control over the nation’s economic well-being. A false diagnosis will lend credence to bad policy choices. Public pressure for monetary and fiscal stimulus (greater government spending, with higher tax rates and more debt) will intensify. Those measures would bring on the same consequences as the 2021-2022 stimulus created: inflation and stagnation.

So, which is it—doom and gloom, or the approach of a glorious summer? Much depends on whether you recognize that the reported unemployment rate is not always a trustworthy economic indicator. The future of the nation’s economy depends on that choice.

Sources: The Wall Street Journal; The Inflation Calculator; Bureau of Labor Statistics; Newsweek; Quant’s Substack; StemTA; CNN

Video of the Week

The Supreme Court has agreed to hear a case that could end the practice of cities suing energy companies, claiming their businesses harm the public by increasing greenhouse gas emissions and causing global warming. In 2018, Boulder County, Colorado, sued ExxonMobil and Suncor, blaming them for contributing to worldwide emissions, with the aim of collecting a massive damage award. If this case goes against Boulder County, it could be a landmark decision that clarifies that national energy policy is set by the federal government through the people’s elected representatives—not radical activists who find a friendly court.

Get the latest best-seller from Heartland’s Justin Haskins!

America’s economy is teetering on the edge of disaster. Hidden beneath record stock market highs and reassuring headlines lies a fragile system riddled with debt, reckless speculation, and decades of political negligence. When the next big crash strikes—and it will—the fallout could be unlike anything we have ever experienced.

Click here to get it at Amazon.

Trump Proposes a New Entitlement

During his State of the Union speech, President Donald Trump announced a plan to provide federal matching grants for contributions to new retirement plans for the approximately 56 million American workers who do not have an employee-sponsored savings plan such as a 401(k) account:

[H]alf of all of working Americans still do not have access to a retirement plan with matching contributions from an employer. To remedy this gross disparity, I’m announcing that next year my administration will give these oft-forgotten American workers—great people, the people that built our country—access to the same type of retirement plan offered to every federal worker. We will match your contribution with up to $1,000 each year, as we ensure that all Americans can profit from a rising stock market.

“We” means current and future federal taxpayers, of course.

Trump’s plan would build on a federal program already scheduled to go into effect at the end of this year, CBS News reports:

The Trump administration’s new plan would expand on a bill signed into law by President Biden in 2022 called the Securing a Strong Retirement Act, or Secure Act 2.0. That bill itself was built on prior legislation passed during Mr. Trump’s first term, according to Axios.

The Secure Act 2.0 created a so-called Savers Match program, set to launch in 2027, under which the federal government will provide a 50% matching contribution up to $1,000 for low- to moderate-income workers.

If Trump’s plan is intended to take over the Savers Match program and the latter is already included in projections of government spending, that means Trump’s proposal will not increase the federal budget deficit and debt. The specifics on the matter are unclear at present, however, and CBS News suggests that Trump’s plan will require new spending:

Some experts questioned how Mr. Trump’s proposed retirement program would be funded and expressed doubt it would fundamentally address the country’s retirement crisis.

“Not only does the administration lack the fiscal authority to seed 401(k)s with a $1,000 taxpayer match, nor is this a good idea,” Romina Boccia, director of budget and entitlement policy at the san Cato Institute [sic], a nonpartisan public policy think tank. “Americans need a simpler system of tax-advantaged savings via universal savings accounts, not more tax-advantaged accounts (ie Trump accounts) or related handouts.”

Regardless of whether the program will involve new spending, creating another entitlement in a time of unprecedented federal deficits and debt is exceedingly ill-advised. It is true that half of all working Americans do not have access to employer-sponsored retirement plans and do not save money for that purpose on their own. The average American worker has saved less than $1,000 for retirement, CBS News notes.

That is a tragedy, and the high rate of federal spending in recent decades is going to worsen that by making it impossible to avert a 20 percent cut in Social Security that is scheduled to become necessary in 2034. On top of all that, adding $2,000 a year to people’s retirement savings is not going to accomplish much, though of course it is better than nothing: $2,000 plus interest better.

Increasing government spending will only bring on that crisis sooner. This new entitlement is a bad idea.

Sources: State of the Union transcript at U.S. News and World Report; CBS News

Important Heartland Policy Study

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Contact Us

The Heartland Institute

1933 North Meacham Road, Suite 559

Schaumburg, IL 60173

p: 312/377-4000

f: 312/277-4122

e: [email protected]

Website: Heartland.org