Introduction: New York’s Fiscal Exposure

New York State’s revenue-raising strategy since the Great Recession could be summed up by a frequent chant at then-candidate Zohran Mamdani’s campaign rallies: “Tax the Rich!” Starting in 2009, with a misnamed “millionaire tax,”[1] the state has piled a growing share of its total personal income tax (PIT) burden on its highest-earning taxpayers.[2] The tax shift culminated in 2021, with the enactment of New York’s biggest marginal income tax rate increase in decades.[3]

Residents with incomes starting just over $1 million now are subject to New York’s highest statutory tax rates since the early 1980s. Net of federal deductions, taxes at the apex of the income pyramid are now the highest ever levied by the Empire State and among the highest in the nation. In New York City, political epicenter of the tax-the-rich movement, resident income millionaires already are hit with the highest tax rates in the country.

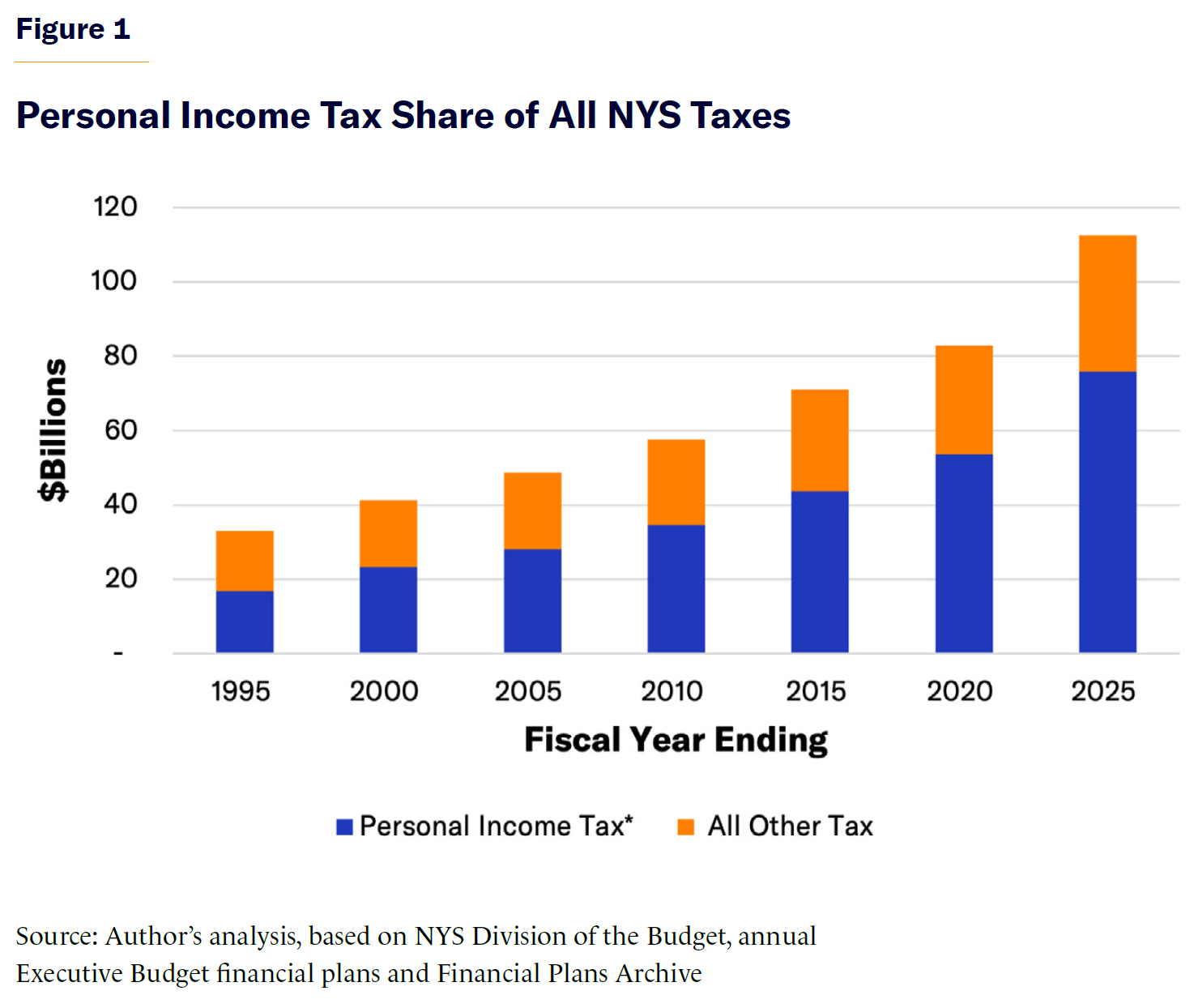

Net taxes on personal income (including, in recent years, earnings separately taxed as “pass-through” profits from closely held businesses) have accounted for a rising share of all state taxes over the past 30 years (Figure 1). In fiscal year 2027, Governor Hochul’s Executive Budget projects that the income tax share will reach a record high of 69% of the total.[4] In 16 fiscal years since the end of the Great Recession, a period coinciding with New York’s latest cycle of millionaire tax increases, PIT receipts have grown three times faster than all other taxes combined.[5]

New York’s most recent income tax hikes underwrote a 40% expansion of state operating funds spending over the past five years, including an 11% rise in fiscal 2026 alone. Bigger budgets aside, higher taxes on high earners also have subsidized temporary tax givebacks and permanent tax breaks for New Yorkers in lower income brackets, effectively shifting more of the net tax burden to the top of the income distribution.[6]

As of 2023, the 68,570 New York households with incomes above $1 million represented 0.7% of all resident PIT filers and earned 26% of adjusted gross income (AGI) while generating 41% of the total income taxes paid by state residents, according to the state Department of Taxation and Finance.[7] Preliminary data from the department indicate that taxpayers earning more than $1 million from New York sources paid 45% of the income tax in 2024. Likewise, in 2023 the 34,280 income millionaires living in New York City were 0.9% of all filers and earned 34% of AGI while generating 37% of the city’s total income tax.[8]

As a result, the state’s revenue base is more volatile than ever, since top earners draw more of their income from capital gains on stocks and other assets whose values can fall as well as rise sharply. Volatility risk was vividly illustrated during the Great Recession market crash of 2007–09, when the taxable incomes of New York’s highest-earning 1% collapsed by 37% in two years—prompting the first in a series of tax-the-rich hikes that have left the state even more reliant on high earners.[9]

As New York’s dependence on income millionaires has grown, so has their financial incentive to spend less time in the state. Facing higher tax rates exacerbated by the 2017 federal law tightly capping state and local tax (SALT) deductions,[10] New York’s population of taxpayers earning over $1 million has dropped sharply, relative to national trends since 2010. Tax data indicate that New York’s share of financial wealth among U.S. millionaire earners has dropped sharply over the past decade—while Florida’s has increased.[11]

Despite these very high stakes, demands to raise taxes on high earners have grown louder than ever in the state capitol and in city hall. The most popular tax-the-rich measure now pending in the legislature is a bill cosponsored in 2025 by 24 state senators and 27 assembly members (including Mamdani), which would more than double the state’s current top income tax rate and further increase taxes across nine other new brackets, starting at incomes of $500,000.[12]

In addition, the new mayor’s legislative allies have introduced a state bill that would implement his campaign proposal to increase New York City’s top income tax by 51%.[13] It would raise the combined top state-city rate to 16.8%, nearly double the effective net-deductibility level prior to the 2017 federal cut.

Beyond raising revenue for expanded social programs, advocates often frame higher taxes on top earners as a moral imperative, a way of offsetting income inequality through stepped-up income redistribution. But at the same time, they downplay or ignore the potential impact on New York’s economic competitiveness and the destabilizing impact on government finances.

The erosion in New York’s tax base is evidence that the piling-on process already has gone too far. To stabilize its tax base and to promote economic growth, New York State should commit to reversing the rate hikes of 2021—and, in the process, to reforming an increasingly cluttered and complicated income tax code. State policymakers should return to the principles that guided the state’s bipartisan income tax reforms in the 1980s: efficiency, equity, simplicity, and transparency.

Origins of and Fluctuations in the New York City Income Tax

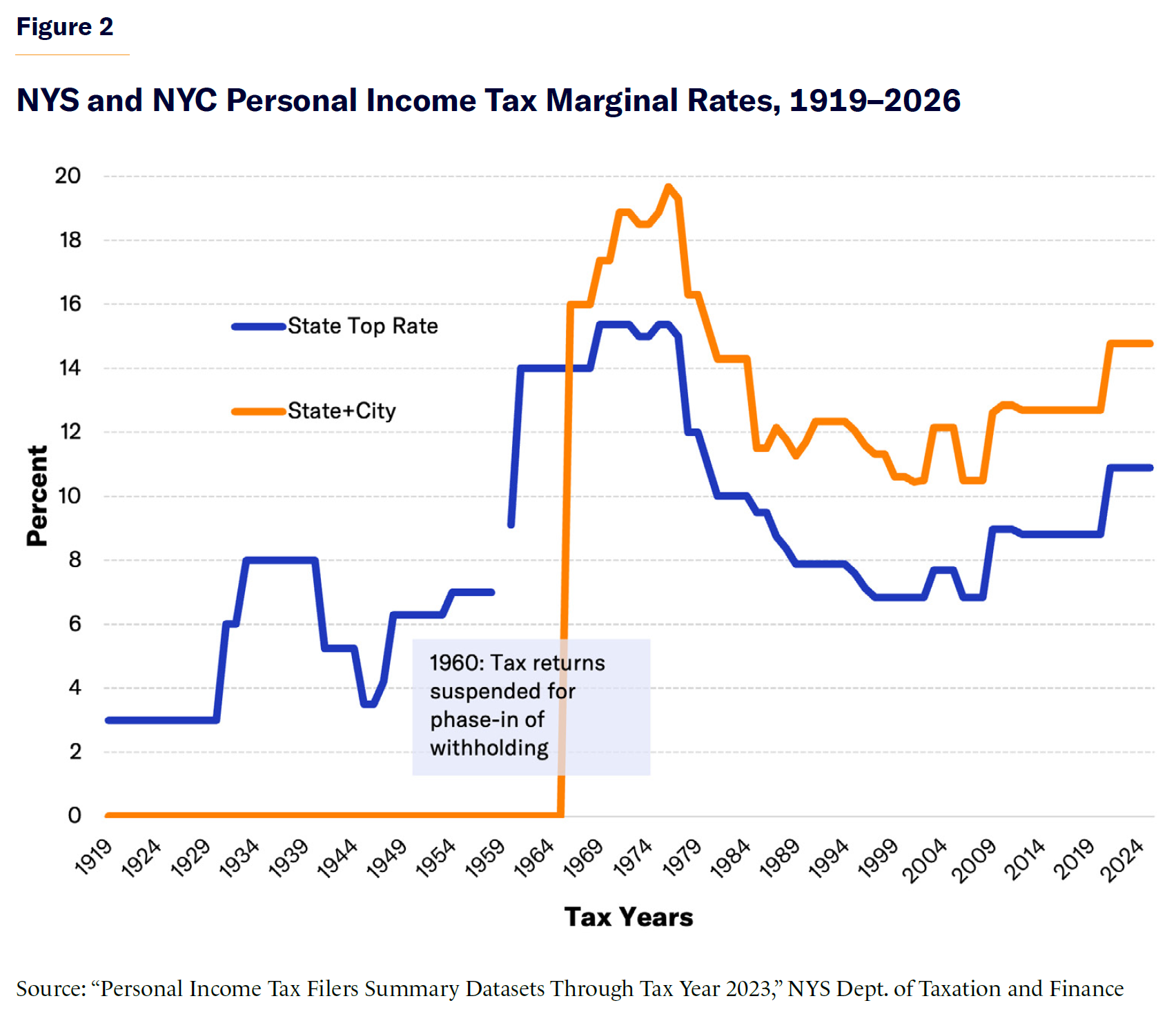

In 1919, anticipating a significant loss of alcohol-related taxes under the impending federal prohibition law, New York became the eighth state to adopt its own PIT. The top PIT rate initially was set at 3% on taxable incomes above $50,000, equivalent to nearly $1 million in mid-2020s terms. It stayed at 3% through the 1920s but would fluctuate widely over the next 25 years, rising as high as 8% during the Great Depression, dropping to 3.5% following the end of World War II, and then rising again in stages to 7% by 1954 (Figure 2). Top brackets by then had fallen to income levels equivalent to the low six figures in 2025 dollars.

Under Governor Nelson Rockefeller (1959–73) the top rate more than doubled, reaching 14% by the early 1960s and 15% by the end of that decade, ultimately hitting its all-time high of 15.35% with the addition of a surcharge for a few years in the early 1970s. By then, the state’s steeply graduated rate structure featured 14 tax brackets, with the top rate kicking in at incomes equivalent to $155,000 in 2025 terms.[14]

In 1966, meanwhile, the state legislature had authorized New York City’s first resident income tax, calculated on the same tax return forms as the state PIT and imposed on top of (and not deductible from) the state tax.[15] Initially set at 2%, the city’s top rate was raised to 3.5% in 1971 and to 4.3% starting in 1976.[16] Because the state income tax was so steeply progressive, the city income tax from its inception has been imposed on a much flatter rate structure, with its top bracket peaking at lower income levels than the state PIT.

The reversal of the Rockefeller-era income tax hikes began under Governor Hugh Carey, a Democrat who took office in 1975. Between 1978 and 1981, with bipartisan legislative support, the top rate on “earned” income (from wages, salaries, and business profit) ultimately was reduced to 10%.[17] Despite that one-third cut in the top rate, New York State PIT revenues increased by 6.8% on an inflation-adjusted basis during this period, reflecting a combination of economic growth and the impact of “bracket creep,” through which the high inflation rates of the era pushed more taxpayers into higher tax brackets.[18]

During the 1980s, New York was effectively nudged into further rate cuts by the enactment of steep reductions in federal taxes. Under Governor Mario Cuomo, the top rate was dropped to 9% in 1985.[19] Two years later, New York’s more sweeping 1987 Tax Reform and Reduction Act reduced the top rate to 7%, coupled with the elimination of many tax brackets, generous standard deductions, and the elimination of a marriage penalty in the previous law.[20] A phased reduction of New York City’s income taxes also began in 1987,[21] ultimately taking the city rate to a 19-year low of 3.4% in 1989.

Neither the state nor the city income tax cuts of 1987 proved to be lasting, however. The five-year phase-in of the new tax law was interrupted after its second year, leaving the top rate at 7.875% for 1989 and 1990.[22]

Meanwhile, at the request of the city council in 1991, New York City’s income tax was raised with an across-the-board 12.5% surcharge, in order to fund the hiring of additional police. Also in 1991, an additional 14% surcharge was added to all tax brackets at the behest of Mayor Dinkins.[23] The combined surcharges raised the city’s top rate to 4.46%, bringing the combined pre-deduction state and city marginal rates to 12.3% through the early 1990s.

New York’s progress in reforming and reducing income taxes resumed in 1995, when newly elected Governor George Pataki (1995–2006) pushed a modified version of the unfinished 1987 tax cut through the legislature,[24] reducing the top rate to 6.85% atop a relatively flat bracket structure.

Income taxes were also cut in New York City in the late 1990s. The 12.5% income tax surcharge was allowed to expire at the end of 1998, and a further reduction in the city’s top rate was subsidized by the state under its new School Tax Relief (STAR) program starting in 2000.

By 2002, the city’s top rate had been lowered to 3.65%, and the maximum combined state and city tax rate had fallen to 10.5%, close to its lowest level since the adoption of the city income tax in 1966. However, Pataki’s Taxpayer Relief Act of 1995 represented New York’s last effort at broad-based tax reduction. All subsequent changes to the state tax law have raised top tax rates, sometimes in combination with cuts to lower rates.

Tax Policy in the Wake of the Great Recession

The 2001 recession, followed by the stock market downturn of 2002, opened a sizable hole in state and city revenues by the end of fiscal year 2003.[25] Overriding Pataki’s veto but with support from Mayor Michael Bloomberg, the legislature in 2003 filled the hole with temporary income tax increases at the state and city levels.[26] The state rate was raised to 7.7% on incomes above $500,000 for all filers and to 7.5% on joint filer incomes above $150,000, while the city’s top rate was boosted to 4.45%, also for joint filer incomes above $150,000.

Amid a moderate economic recovery and a strong Wall Street bull market, those tax increases were allowed to expire on schedule at the end of 2005.[27] But New York’s income tax rates had reset to 2003 levels for only three years when the 2008 onset of the financial crisis and Great Recession blew a hole in projected state revenues for the next four fiscal years. Governor David Paterson and the legislature responded in early 2009 by temporarily raising the top PIT bracket to 8.97%, matching what was then New Jersey’s top rate. The measure was widely described as a “millionaire tax,”[28] although the new top rate kicked in at incomes as low as $350,000 for single filers. Rates below that level were raised to 7.85%, starting at $200,000 for single filers and $300,000 for married couples.

Governor Andrew Cuomo initially pledged not to extend the 2009 increase, which was due to expire at the end of 2011, his first year in office.[29] In December 2011, however, Cuomo initiated a three-year extension of the tax increase on a modified basis, resetting the top rate at 8.82%. The new tax bracket replicated the existing “benefit recapture” language, meaning that, as a taxpayer’s income exceeds certain thresholds, the state adds extra tax that gradually removes, or “recaptures,” the effect of lower marginal brackets so that higher earners’ tax more closely resembles a flat rate on most of their income. And it turned the 8.82% marginal rate into a flat rate on taxable incomes exceeding a narrow phaseout range above the $1 million–$2 million statutory thresholds.

In contrast to the 2009 tax increase, the 2011 changes coupled a higher tax rate on high earners with tax rate reductions in brackets below $1 million. The temporary 7.85% bracket rate was returned to 6.85%, and two new brackets were inserted below that level, setting rates of 6.45% to 6.65% on taxable incomes ranging from $40,000 to $300,000 for married couples and correspondingly lower levels for single filers. In addition, for the first time, New York’s tax brackets, dependent exemptions, and standard deduction were indexed to rise with inflation.

The 2011 changes initially were framed as temporary and scheduled to expire in 2014.[30] Ultimately, the 8.82% top rate would be temporarily extended three times over the next eight years, and rate cuts in brackets below $1 million were succeeded by additional cuts in lower brackets on a long-term phase-in schedule approved in 2016.[31] However, automatic inflation indexing of tax brackets ended in 2017.[32]

Pressure for significant further tax increases on millionaire earners increased after Democrats assumed control of the state senate in 2019, but Governor Cuomo continued to oppose the idea. “Tax the rich. Tax the rich. Tax the rich. We did that. God forbid the rich leave,” he said.[33] Even in the fall of 2020, after the pandemic disruption had given rise to large potential deficits, Cuomo continued to reject proposals for extensive new taxes on the wealthy.[34]

But in January 2021, in what would turn out to be his final state budget, the governor proposed a temporary three-year income tax increase that would have supplemented the 8.82% tax on millionaire earners with rates above 9% on incomes between $5 million and $10 million, rising above 10% for incomes starting at $25 million.[35]

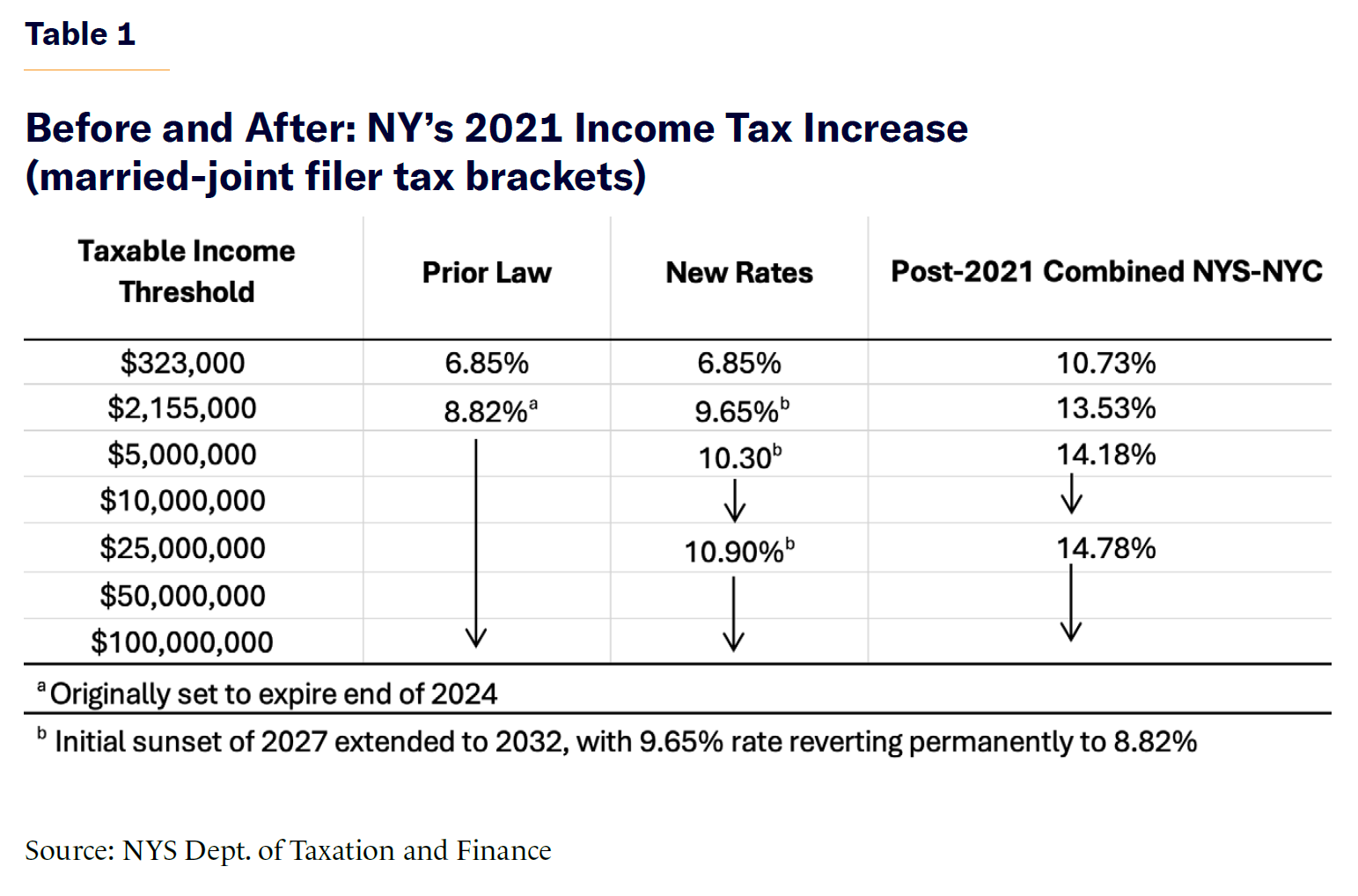

The legislature significantly added to Cuomo’s proposed tax hike in a revenue bill signed by the governor as part of the budget that year (Table 1). The previously time-limited 8.82% rate was made permanent—a move equivalent, all by itself, to New York State’s largest tax increase since 1961—and temporarily raised to 9.65%. New rates of 10.3% and 10.9% were added at income levels of $5 million and $25 million, respectively. All three higher rates were subject to “benefit recapture” language converting them into flat taxes.[36] The 2021 tax increases originally were set to expire at the end of 2027, but Governor Kathy Hochul’s FY 2026 budget package extended the higher rates through 2032.[37]

New York City’s income tax was not increased as part of the 2021 package, but the city tax had already risen over the previous decade. In 2010, the rate cut previously subsidized by the state STAR program, which provided a tax rebate, was eliminated for residents with incomes above $500,000, effectively raising the marginal rate to 3.88%. The STAR-subsidized rate cut was eliminated for all city residents in 2017,[38] raising the rate to 3.88% in the city’s established top brackets of $90,000 for joint filers and $50,000 for individuals.[39]

SALT Seasoning

For most of the first 100 years following its 1913 enactment, the federal income tax allowed for unlimited state and local tax (SALT) deductions. The deduction provided a substantial net discount equivalent to the taxpayer’s federal bracket rate; the higher the federal rate, the greater the discount on state and local taxes. During the 1970s, when the top federal income tax rate was 70%, the SALT deduction effectively reduced New York State’s 15% rate to 4.5%, or a combined 5.8% for residents of New York City.

The first broad limitation of SALT deductibility at the federal level came in 1991, with the enactment of a cap on itemized deductions by high earners, which effectively added up to 1 percentage point to effective marginal rates for the highest-income earners.[40] But even after that change, the SALT deduction provided a significant discount on New York taxes.

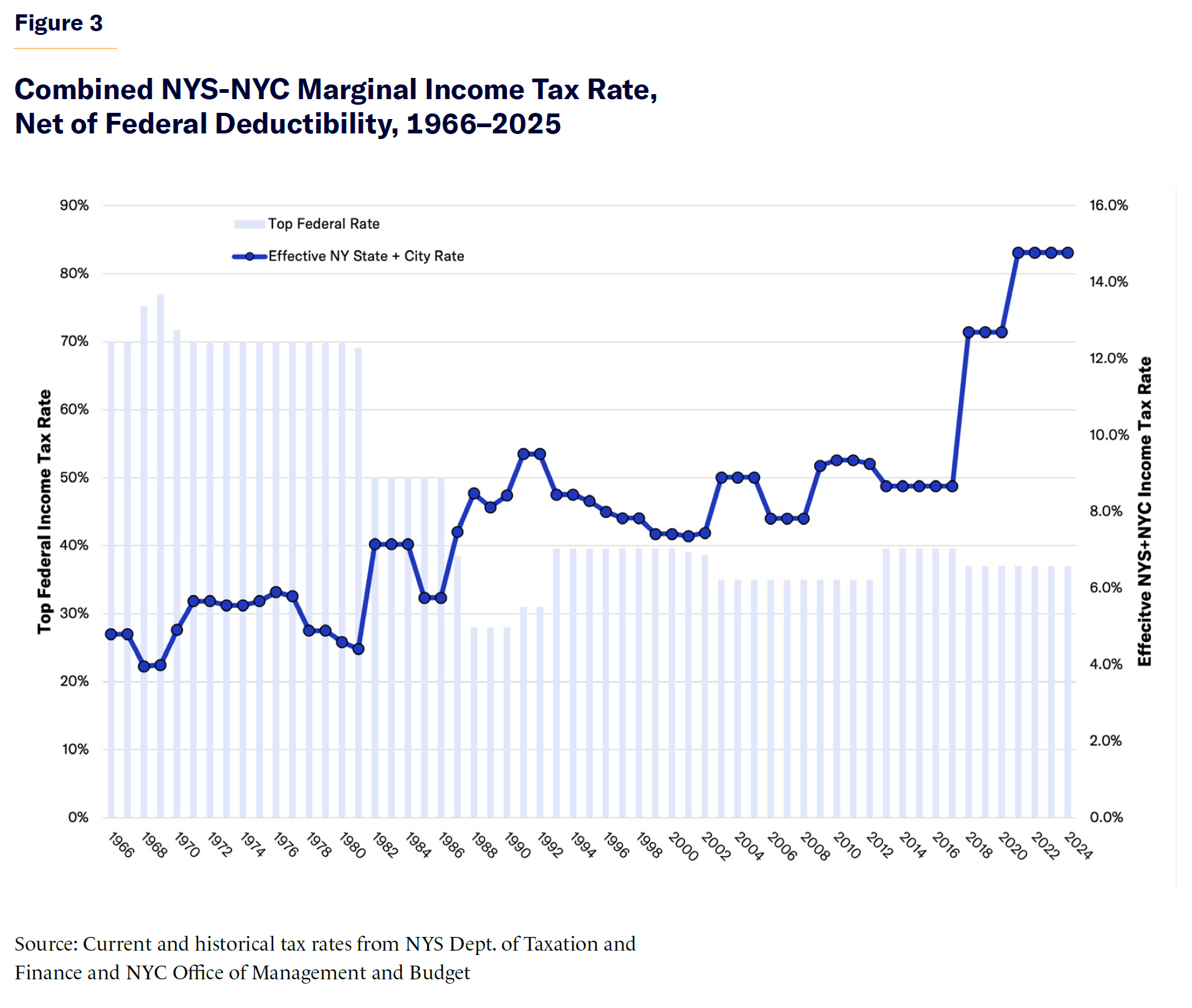

The discount all but vanished with the enactment of the 2017 Tax Cuts and Jobs Act (TCJA). Starting in 2018, the law repealed the 1991 deduction limit but also capped all SALT deductions at $10,000,[41] pushing New York’s effective state and city income tax rates to their highest levels ever. New York’s own 2021 state income tax increase pushed them even higher. The interplay of these tax rates is illustrated in Figure 3.

The New York Difference

The 2017 federal tax law targeted its biggest tax savings at low- and moderate-income families, which benefited from significantly larger child credits, a near-doubling of the standard deduction, and a broadening of tax brackets below the top levels. For higher earners, TCJA’s principal benefit was a cut in the top federal tax rate on ordinary income from 39.6% to 37%. The rate cuts and other major changes in the law were permanently extended by Congress as part of the 2025 tax law amendments.

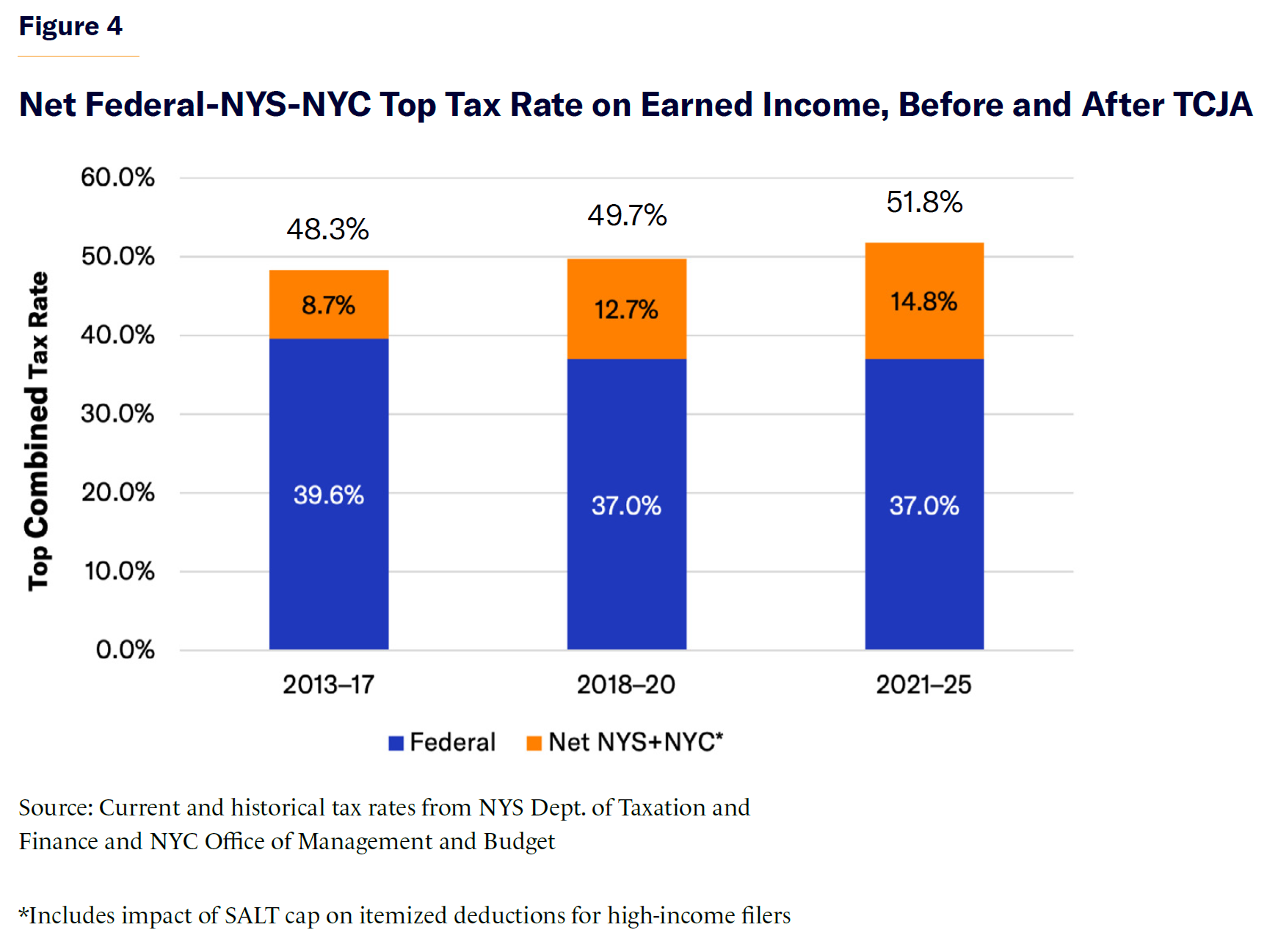

The SALT cap prevented top-bracket New York taxpayers from realizing the full benefit of the 2003 rate reduction. As illustrated in Figure 4, the combined tax rate for New York City–based millionaire earners increased, from 48.3% to 49.7%. When New York raised taxes on high incomes in 2021, the combined state and local rate in New York City rose to 51.8%—higher than at any point since the late 1980s.

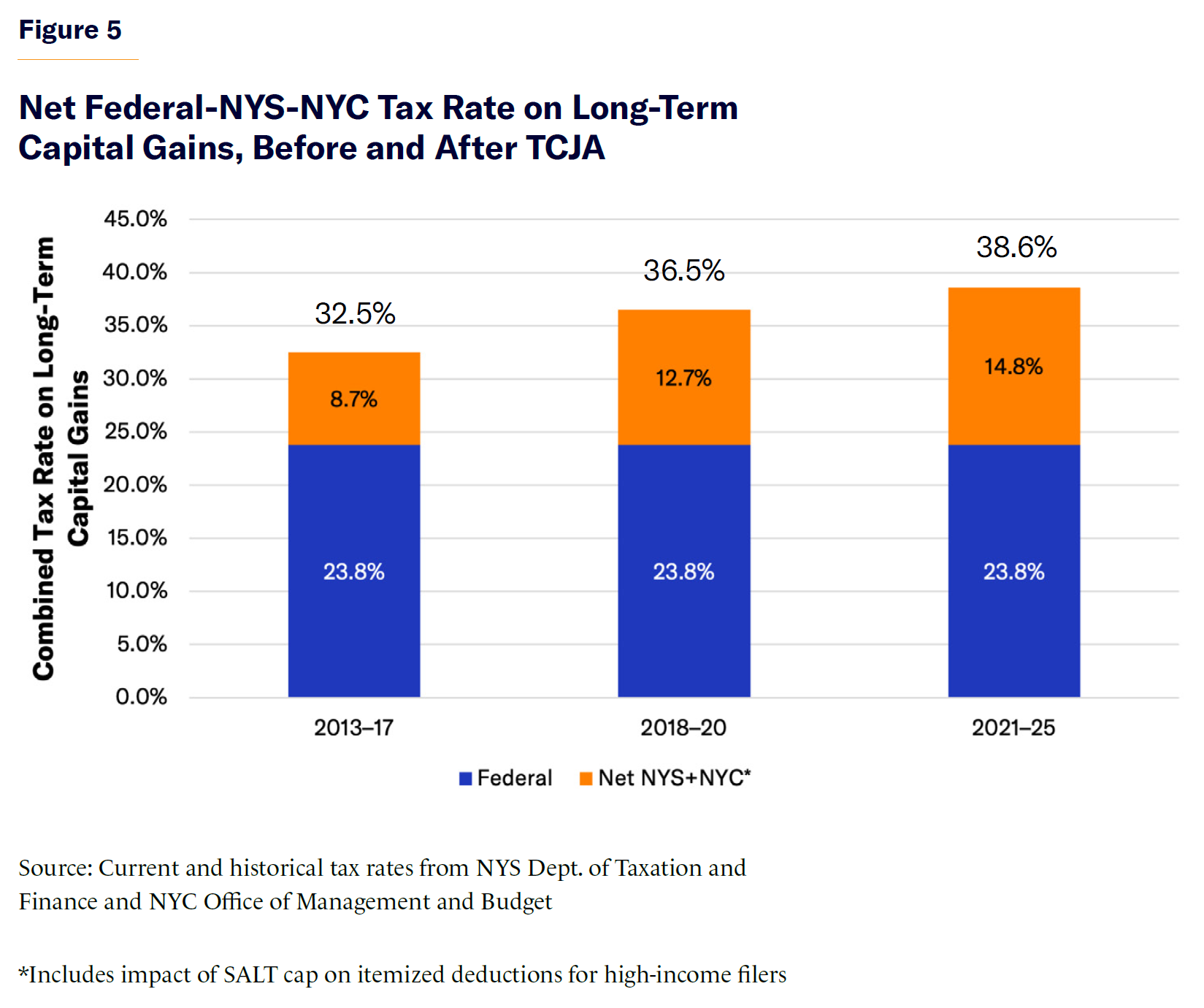

The federal Tax Relief Reconciliation Act of 2003 (TRRA) left the 23.8% federal tax rate on long-term capital gains untouched. However, because New York’s income tax does not differentiate between income types or sources, the 2021 rate increases on wages and salary income also amounted to a significant tax hike on capital gains. As shown in Figure 5, the SALT cap compounded this increase, raising long-term capital gains taxes to 36.5% for residents of New York City in the immediate wake of TRRA’s adoption. The 2021 state tax increase raised it to 38.5%—one of the highest capital gains tax rates in the world.[42]

The 2025 extension and renewal of TCJA made the $10,000 SALT cap permanent while temporarily raising the SALT cap to $40,000 for tax years 2025–29.[43] But this change did nothing to reduce the marginal state and city tax rates faced by New York income millionaires, whose pre-2017 SALT deductions averaged $500,000.

Working Around the Cap

Decrying the SALT cap as “an economic missile aimed at New York,” Governor Cuomo announced in January 2018 that the state would seek to devise at least two avenues to help taxpayers “thwart” the cap: a federally deductible corporate payroll tax fully offset by state PIT credits; and special state and local “trust funds” that could receive payments in lieu of taxes that could be deducted as charitable contributions.[44] These ideas never panned out, but a third concept ultimately did: the creation of an optional entity-level state tax on unincorporated businesses, such as partnerships and wholly New York–based and New York–owned Subchapter S corporations. Exploiting what was then a gray area in federal tax law, lawmakers hoped that such “pass-through entities” might fully deduct the state tax as a business expense on federal tax reforms, as incorporated businesses have long done.[45]

On November 9, 2020, the Internal Revenue Service (IRS) issued a regulatory notice signaling its intent to issue regulations allowing pass-through entities to fully deduct state and local taxes from income distributed to their profit participants. Following the lead of neighboring Connecticut and several other states, New York responded in 2021 with the creation of its own optional pass-through entity tax, or PTET. New York City enacted a local PTET the following year to provide a workaround of the city income tax.

Thirty-six states, including New York, currently have pass-through entity workarounds on their books, according to the Tax Foundation.[46] Because New York’s PTET is fully refunded to partners and shareholders via PIT credits offsetting their portion of entity payments, it neither reduces nor increases their net tax burden. It does, however, generate a significant federal tax savings for those who opt into it—upward of $5 billion for New York PTET payers in 2025, assuming that virtually all were in the 37% federal income tax bracket.[47]

As of 2025, according to the state Department of Taxation and Finance, nearly 100,000 entities had opted to pay New York’s state PTET tax, which, in fiscal year 2026, is expected to raise $16 billion. All that money ultimately will be refunded to entity partners and shareholders via PIT credits. PTET business tax returns must be filed by March 15, two weeks before the end of the state fiscal year, while the deadline for PIT returns claiming credits is April 15, two weeks after the start of a new fiscal year. As a result, PTET payment and credit totals do not line up in the same fiscal year, which has muddied the picture of PTET-PIT impacts on the annual state budget.

Further obscuring the impact of the workaround, the state has not released statistical data on the timing, incidence, or distribution of the tax itself or of PTET credits. Based on annual state PIT data before and after PTET’s enactment, it appears that over 90% of the credits were claimed by millionaire earners, including residents and nonresidents.[48] This is consistent with New York City data[49] indicating that millionaire earners qualified for 95% of the city’s own PTET credits as of 2023.

While PTET essentially restores the pre-2018 SALT deduction (plus a little extra, since it is not subject to the old Pease limit), New York State and New York City remain among the most heavily taxed jurisdictions in the country, even after the PTET workaround, adding up to 9.3% to what the same business owners would owe in lower-taxed states.[50] Adjusted state data indicate that credits for PTET payments offset less than half the total pre-credit tax liability of filers with incomes above $1 million in 2023.[51] Over half the total income of resident millionaire earners does not originate with pass-through business sources and is taxed at the full, nondeductible state rate.

More Millionaires or Fewer?

Emerging from the Great Recession and financial crisis in 2010, New York State was home to 33,828 full-year resident taxpayers with AGIs above $1 million. By 2022, the number had more than doubled, to 67,189. The largest single-year increase in the number of filers in the $1 million+ bracket came in 2021, the same year that income millionaires were targeted by New York State’s biggest tax rate increases in decades.

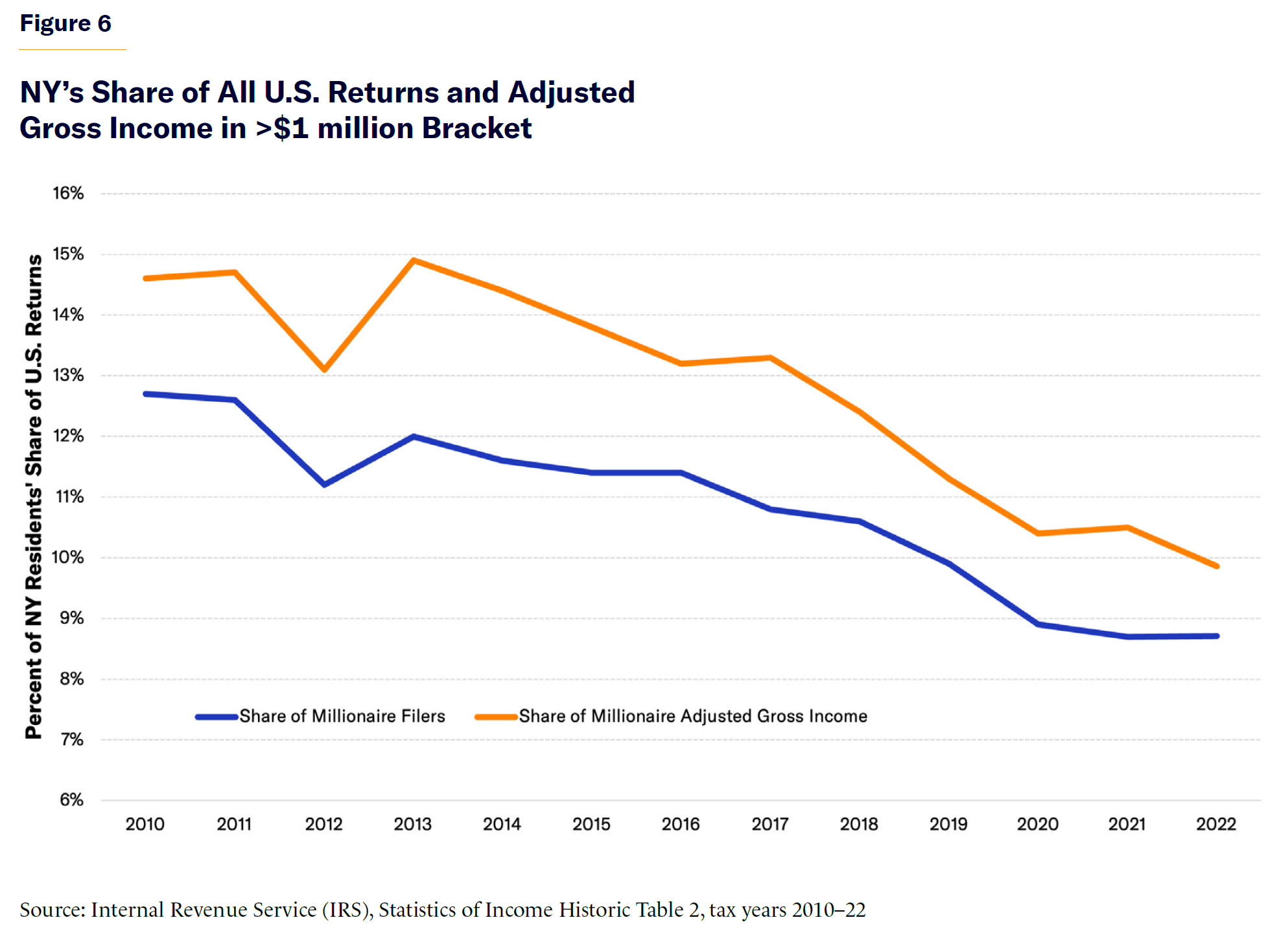

Tax increase advocates often cite New York’s higher 2021 millionaire population as evidence that sharply higher taxes did not cause wealthy residents to leave the state. However, a fuller statistical picture tells a very different story (Figure 6). Evaluated in a national context, the post-2010 trend in New York’s millionaire taxpayer count has been decidedly negative.

Based on IRS data, the Empire State share of all U.S. income millionaire earners declined from 12.7% in 2010 to 8.7% in 2022. The drop in the state’s share of total AGI among millionaire earners was more pronounced, from 14.6% in 2010 to 9.86% in 2022.

A large segment of New York State’s highest earners is not subject even to the lowest of the state’s elevated post-2009 tax rates. As of 2023, nearly 61% of 68,577 full-year resident income millionaires had AGIs of $1 million–$2 million, according to state tax data. Within that group, 34,967 households were married couples filing joint returns, who are not taxed at the lowest millionaire rate of 9.65% unless their taxable incomes (i.e., AGI minus deductions) exceed $2.155 million. The upshot: fully half the state’s resident income millionaires were still paying a 6.85% marginal rate, which now kicks in at a taxable income of $323,000 for married couples.

Many of these single-digit millionaire earners surely are aware (or reminded by their accountants) that they are brushing up against a significantly higher tax bracket. But in assessing their incentive to move to a lower-taxed state or to minimize income subject to New York tax, another factor needs to be considered: as of 2023, tax filers in New York State’s $1 million–$2 million bracket draw over half their total income from wages and salaries, indicating that they work for someone else. Where they work is ultimately decided by their employers—corporate executives, senior partners, and business owners in higher tax brackets.

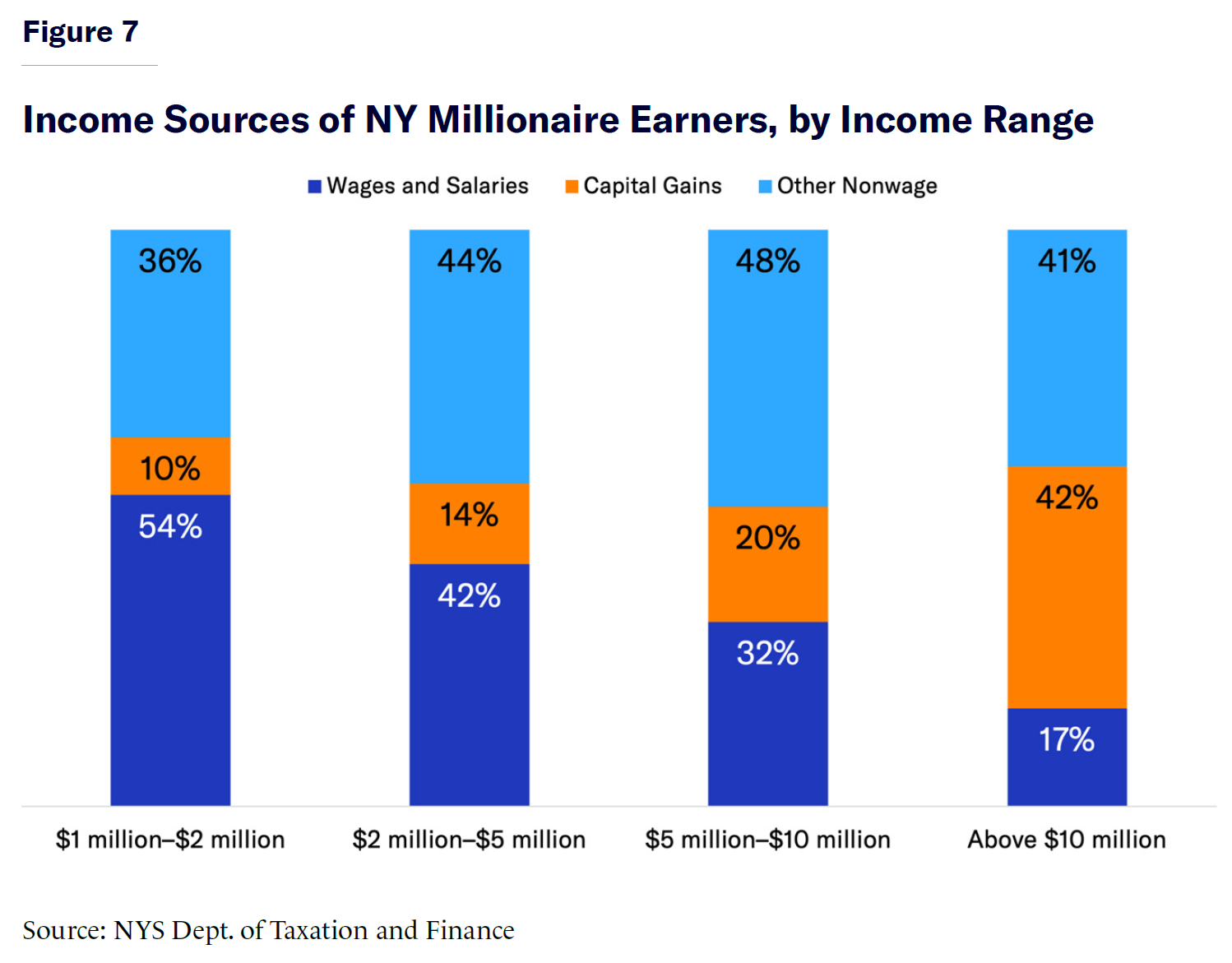

In contrast to the $1 million–$2 million group, taxpayers in the top three income brackets have become progressively less reliant on wages and more reliant on capital gains and other nonwage sources, including interest, dividends, business profits, and rents (Figure 7). Among New York taxpayers with AGIs above $10 million, the highest bracket measured by state and federal tax statistics, capital gains, and other nonwage sources averaged 83% of income as of 2023, with wage incomes constituting just 17%. Capital gains are the most portable form of income, generally subject to taxation based on the taxpayer’s place of residence rather than place of work.

The 3,172 full-year New York resident filers with incomes above $10 million represented a microscopic 0.03% of all resident income tax filers in 2023. They reported about 11% of total gross income—but accounted for 19% of pre-credit tax liability. The estimated $10 billion[52] in state income tax liability incurred by these 3,172 filers, an average of $3.1 million per household, was more than double the total income tax paid that year by 5.45 million New York households with incomes below $100,000. On average, every 32 filers in the $10 million+ bracket represent nearly $100 million from state income tax revenues, based on 2023 data. At that level, the outmigration of just 320 households would cost the state nearly $1 billion.

State data indicate that the highest-earning cohort of New York State’s full-year resident income millionaires has been shrinking fastest relative to national totals derived from federal tax data. Between 2015 and 2022, the state’s count of full-year New York resident tax filers earning $1 million–$2 million was down 21% relative to federal taxpayer count in the same bracket. During the same period, the number of New York resident taxpayers with incomes above $10 million decreased by 31% relative to the national total.

Capital Gains—and Losses

Growth in New York State’s tax base of income millionaires is strongly correlated with trends in net capital gains realizations, which, in turn, are driven largely by the performance of the stock market. Like stock market indexes, capital gains income is highly variable—the primary source of volatility in revenue generated by income taxes on top earners.

Investment returns recovered and stabilized in the decade following the stock market crash of 2007–09. Defying market doomsayers during the early phase of the Covid-19 pandemic, the stock market surged and capital gains rose strongly in the final three quarters of 2020. The boom continued into 2021, when capital gains nearly doubled.

Nationally and at the state level, the stock market created more new income millionaires in 2021 than ever before. Yet despite its status as a global financial center and investment banking hub, New York’s population of resident income millionaires declined slightly as a share of the national total.

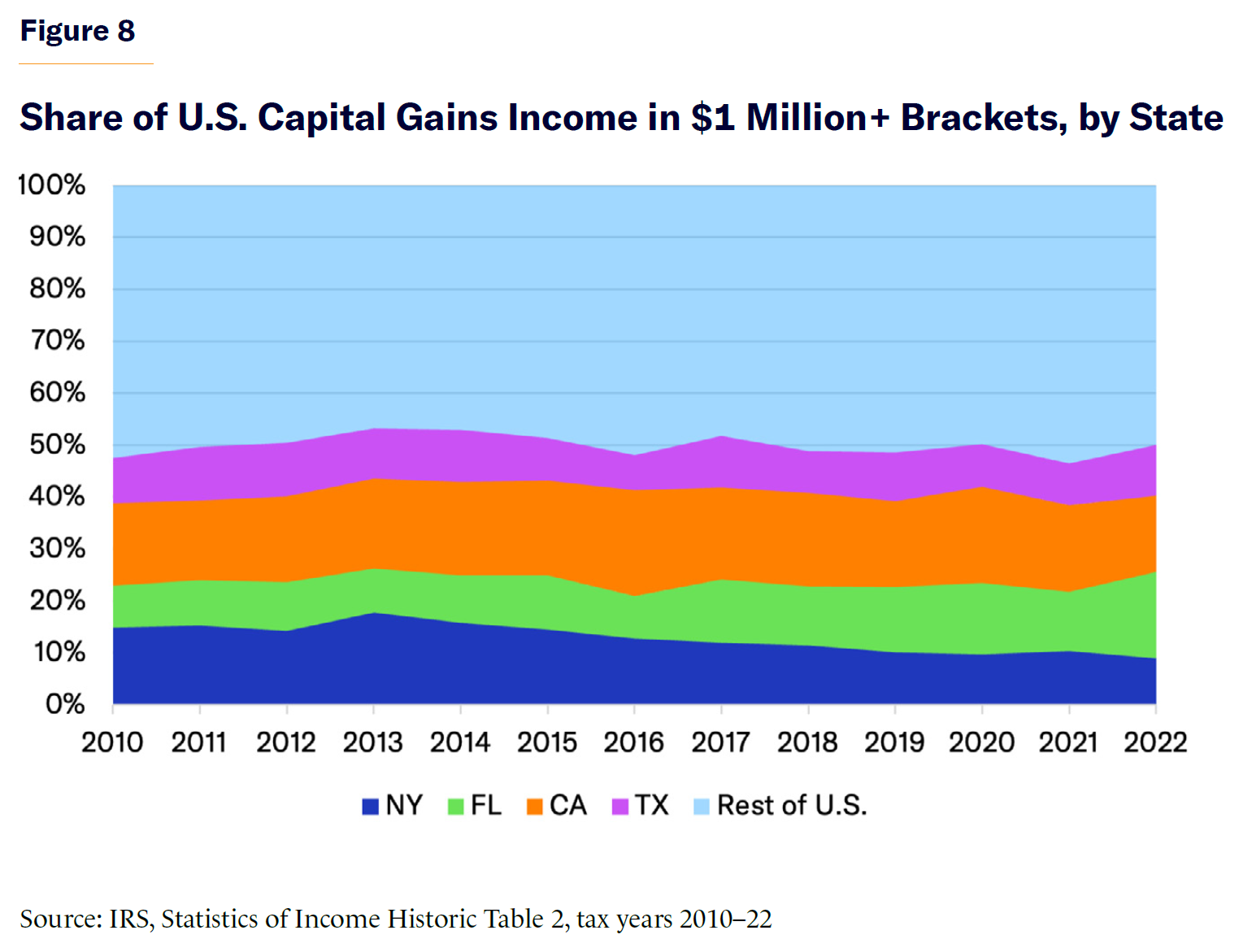

The distribution of financial asset wealth across the country is reflected in annual data on capital gains realizations by income class. As the nation emerged from the Great Recession in 2010, the capital gains of income millionaires were disproportionately concentrated in the four most populous states: California, New York, Texas, and Florida. Between 2010 and 2022, taxpayers earning $1 million or more in these states accounted, on average, for 50% of the nation’s total capital gains realizations.

At the start of the period, California led all states, with 16% of capital gains among all U.S. income millionaires (Figure 8). New York ranked second, at 14%, while Texas and Florida trailed at 8.7% and 8%, respectively. The next 12 years saw a significant shift in the rankings. By 2022, Florida had topped the list, with 16.7% of capital gains income among millionaire earners, followed by California at 14.9% and Texas at 9.7%. New York had dropped to fourth place, with 8.9%—essentially changing places with Florida.

As shown, Florida’s capital gains share fluctuated but generally headed upward before 2021–22, when it jumped 5.4 percentage points in a single year. New York’s share peaked in 2013, an exceptionally strong year for the stock market, then declined steadily through 2020, ticking up in 2021 before declining again in 2022. The totals for New York and Florida crossed paths in 2017–18 and have since headed in opposite directions.

The numbers are consistent with significant wealth migration from New York to Florida, starting several years before the well-documented increase in southward outmigration of high earners from the Empire State during the Covid-19 pandemic.

Conclusion and Recommendations

The Wall Street boom that has pumped up financial-sector bonuses and profits since 2020 has obscured an ongoing erosion at the pinnacle of New York’s income pyramid—as reflected in the state’s declining relative share of income millionaires and capital wealth, dating back to the early 2010s.

The state’s tax base is more reliant than ever on income taxes paid by a tiny number of income millionaires. This is reflected in recent revenue trends: from fiscal 2010 through fiscal 2025, personal income–based tax revenues increased nearly $43 billion, while all other tax receipts rose just $13.6 billion. Since 2020, the last year before the latest and largest marginal tax rate increases, personal income–based taxes rose $24 billion, and all other taxes were up just $7.3 billion.

But repeated “tax the rich” policies are not the only problem. Sporadic tax cuts for low- and middle-income filers have complexified the state tax code while delivering only fleeting savings—because even a low rate of inflation erodes the value of these cuts and pushes more people into higher tax brackets. Tax gimmicks have added complexity and opacity to the state’s tax code over the past 30 years.

Consistent with the principles guiding the state’s last major wave of bipartisan tax reform in the 1980s—which aimed for a tax code that was competitive, equitable, and efficient—the state should embrace two tax policy priorities:

1. Roll back the tax increases of 2021.

Instead of extending the higher rates through 2032—which would be tantamount to making them permanent—the governor and legislature should adopt a schedule for incrementally phasing out these rates over the next five years.

2. Permanently resume inflation indexing of tax brackets and standard deductions.

Temporary and one-shot cuts in middle-bracket tax rates—including yet another rate cut scheduled for 2027—should be replaced with the permanent reinstitution of automatic inflation-indexing of tax brackets, personal exemptions, and standard deductions, which have been features of the federal income tax code for 45 years. Inflation indexing is the most substantial step that New York’s leaders can take to truly safeguard the “affordability” of state government for all taxpayers.

New Yorkers deserve a clear and competitive tax code. Doubling down on “tax the rich” policies will only further undermine the state and city.

Endnotes

Photo by Kyle Mazza/Anadolu via Getty Images

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).