Petrochemicals and plastics.

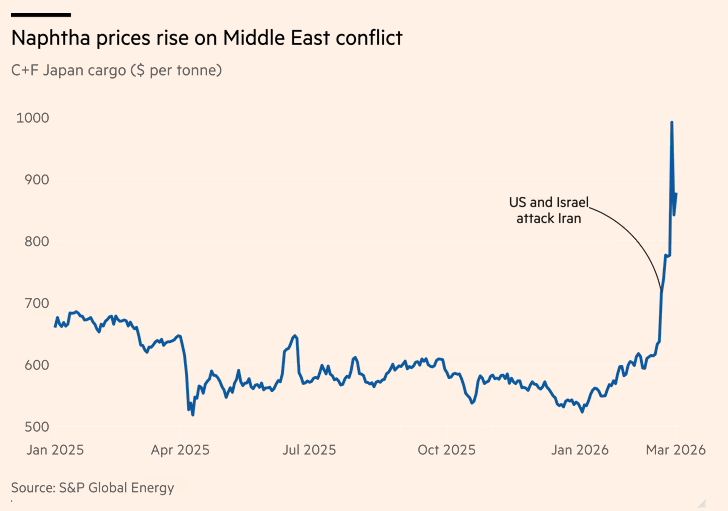

Perhaps the most obvious point of stress is for petrochemical products directly derived from oil and gas and on which plastics, clothing, and other products today depend. Gulf oil producers began diversifying downstream years ago and are today some of the world’s largest petrochemical producers and exporters. The Gulf Cooperation Council states (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, and Oman), for example, produce about 26.5 million tons of ethylene annually—or around 12 percent of the world’s total. They’re also major players for other petrochemical building blocks, such as propylene and butadiene, and supply 70-80 percent of the naphtha feedstock on which major Asian petrochemical producers rely. Most of the latter passes through the Strait of Hormuz, and prices have jumped from around $600 per ton to start February to almost $900 per ton last week.

The Iran conflict has thus caused a double-whammy for global petrochemical production: The Hormuz closure stopped Gulf shipments of the aforementioned petrochemicals, along with polyethylene, polypropylene, ethylene glycol, and methanol, and Iran’s drone attacks have taken certain Qatari facilities offline entirely. Blocked naphtha shipments, meanwhile, have caused Taiwanese, Korean and Japanese petrochemical producers to reduce output or stop production entirely, further stressing global supplies. (Asian facilities typically have just one month of feedstock in inventory, and it takes up to two weeks for them to restart.)

Force majeure declarations—uncontrollable, unforeseeable events that prevent parties from fulfilling their contractual obligations and thus allow them to cancel—have cascaded through the petrochemical supply chain, especially in Asia and Europe. The U.S. is more insulated because we’re a massive producer and less reliant on naphtha feedstock, but petrochemical prices have risen here too because of high energy prices, reduced global supplies, and heightened geopolitical uncertainty. Prices for plastics, packaging, auto parts, clothing (synthetic textiles), and medical supplies would be the next shoe to drop if the conflict persists. Raw materials account for up to 70 percent of plastic products’ manufacturing costs; so, when those costs spike, manufacturers absorb margin hits or consumers pay more. It’d likely be a bit of both.

Fertilizer, agriculture, and food.

Fertilizer may be the best example of the war’s knock-on effects in the U.S. Most industrial fertilizers are energy-intensive, and Gulf states have become large global producers. As Fortune reported last week, for example, “About one-third of global seaborne fertilizer passes through the Strait of Hormuz, where Persian Gulf nations export nearly half of the world’s urea and 30% of its ammonia—key plant nutrients.” Phosphate fertilizer, meanwhile, needs a lot of sulfur to produce, and “roughly half of the world’s exported sulfur moves through the Strait of Hormuz.”

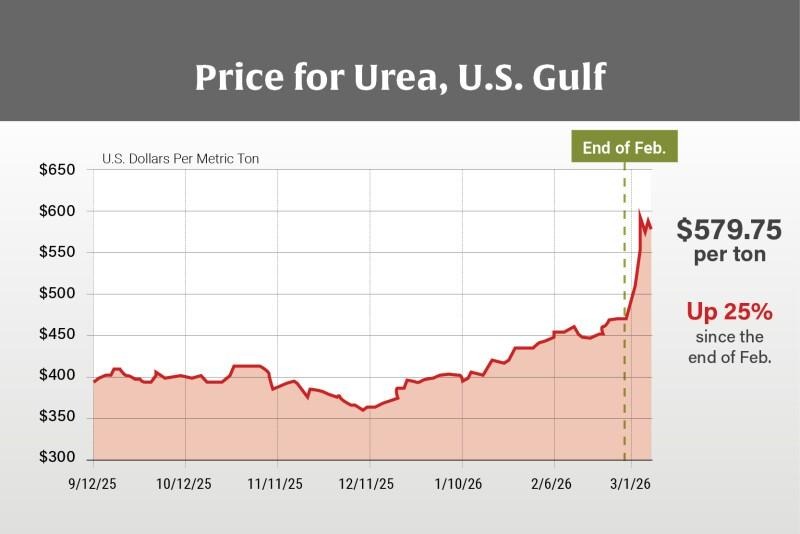

With these and other supplies now threatened, if not halted entirely, fertilizer prices have predictably skyrocketed—including in the United States. Two weeks into the war, AgWeb reports, the U.S. price of urea was up $140 per ton (around 25 percent); ammonia (NH3) rose $100 per ton; and urea ammonium nitrate (UAN) was also up $10 per ton.

As AgWeb goes on to explain, substantial domestic fertilizer production hasn’t shielded American farmers from these higher prices because urea, ammonia, and major fertilizer inputs (including energy) are globally traded commodities, and the U.S. market—imports and exports, upstream and down—is globally integrated. Thus, much line crude oil, “even when the United States is not directly importing fertilizer from the Middle East, domestic prices still follow global markets.”

The timing of the fertilizer price shock also couldn’t be worse for farmers. Not only do prices remain elevated because of U.S. tariffs (and trade remedy measures), but American corn and soybean farmers are also now entering their spring planting window, which requires them to lock in fertilizer purchases. Some are considering changing what they plant to reduce their costs, and the American Farm Bureau’s president even warned that the nation “risks a shortfall in crops.” Higher food prices could follow: Wolfe Research estimates the fertilizer disruption alone could “raise ‘food-at-home’ inflation by roughly 2 percentage points, adding about 0.15 percentage points to headline inflation in the U.S., on top of roughly 0.40 percentage point increase from energy.”

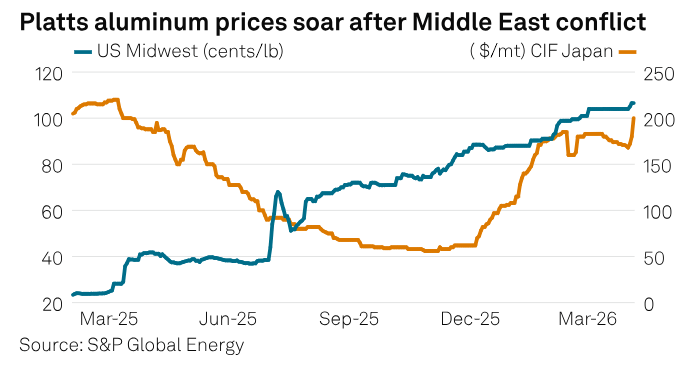

Aluminum.

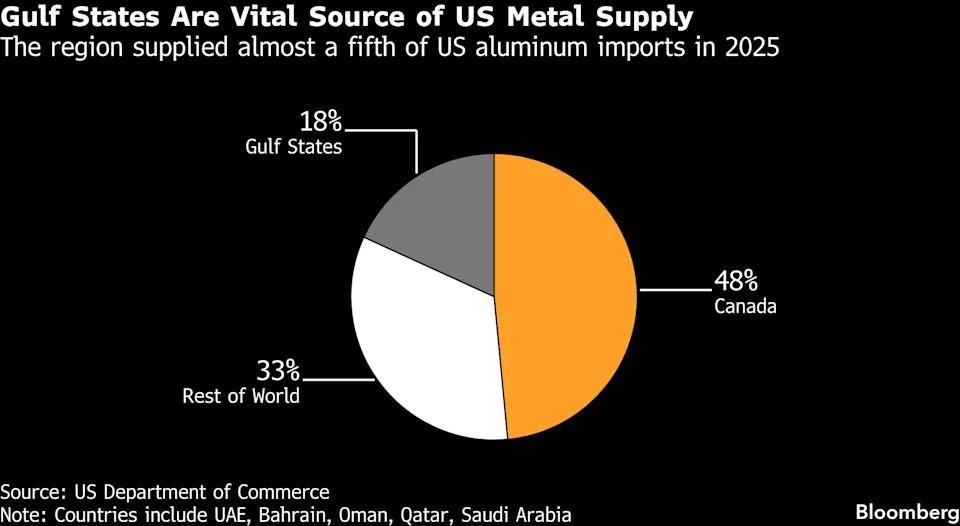

Another energy-intensive commodity, aluminum, has had a similar experience. Gulf states produce around 8 percent of global aluminum output, and the strait is a major thoroughfare for both aluminum exports (5 million tons to 70 countries last year) and imported inputs (bauxite and alumina). Due to both the strait’s closure and Iranian missile attacks, major aluminum producers across the region have stopped shipments and idled capacity—including the world’s largest smelter in Bahrain. Global prices have soared, with the London Metal Exchange hitting its highest level since 2022.

Things are even worse in the United States, thanks to Trump’s 50 percent “national security” tariffs and the fact that U.S. aluminum demand far exceeds domestic production. Because of the tariffs, U.S. prices (inclusive of the “Midwest Premium” that American consumers pay to have aluminum delivered) were already well above global prices. Even worse, Trump’s tariffs had caused the largest foreign supplier—Canada—to turn to Europe and other markets, making American companies more reliant on… wait for it… Middle East producers.

The Midwest Premium unsurprisingly hit a fresh record after the war began, and it’s climbed even higher since.

Like fertilizer and chemicals, high aluminum prices could cascade into other downstream products. U.S. manufacturers in automotive, aerospace, food, and other industries have already faced tariff-inflated metals prices, and some now have contracted aluminum shipments stranded in the Middle East with no quick alternatives available. Higher consumer prices could follow: Trump’s steel and aluminum tariffs, for example, pushed up prices of canned food and beverages last year, and the Iran war could do more of the same.

Semiconductors (and their inputs).

The Iran war’s fallout isn’t limited to basic commodities like metals and fertilizer and could, in fact, hit one of the most complex and important industrial inputs in the world: semiconductors. For starters, chipmaking is energy-intensive, and producers in Asia rely heavily on Middle Eastern oil and gas to power their economies. Per Bloomberg, “Taiwan has a 97% dependence on foreign imports for its energy needs, Goldman Sachs Group Inc. analysts led by Alvin So estimated in a note on Sunday, with about 37% of LNG supply coming from the Middle East.” As the Financial Times reported last week, moreover, global chipmaking is also reliant on helium, sulfur, and bromine from Gulf region:

Semiconductor companies use sulphuric acid to clean wafers and rely on helium, which is also heavily produced in the Gulf, to help cool them during manufacturing. The semiconductor industry accounts for about a fifth of global helium demand, according to consultancy TechInsights.

“About a third of the global helium supply is from Qatar, which is used in things like cooling and leak detection in chip fabs,” said Mohammad Ahmad, chief executive of supply chain intelligence platform Z2Data.

Meanwhile, one of the world’s largest sources of bromine — used in the etching of patterns on to silicon wafers — is the Dead Sea. A 2023 report from the Korea International Trade Association found that the country imported more than 99 per cent of its bromine from Israel.

These bottlenecks will strain chipmaking giants like TSMC, Samsung, and SK Hynix, each of which have seen their shares drop since the Iran war began. If they persist, global semiconductor output, which has already been stretched thin by the global AI infrastructure build-out, will take a big hit. American tech giants are slated to spend roughly $650 billion on AI infrastructure in 2026, and a deep and prolonged Iran conflict could threaten those plans—and the U.S. economic growth that depends on them.

And then there’s shipping.

The war has also hit global shipping in several ways, pushing rates higher around the world. The Wall Street Journal reports, for example, that about 100 container ships are stranded in the Gulf waiting for the strait to reopen, and major shipping companies like Maersk and MSC have canceled key routes in the Middle East region. This has, in turn, put stress on alternative shipping lanes and nearby ports (which are now “almost full”), while causing new global shipping delays and increased shipping rates.

Making matters worse is the fact that, contrary to Trump’s claims last year, the Red Sea crisis has never been fully resolved, and right after the first Iran strike, the Houthis promised to attack commercial vessels looking to use the Suez Canal. Many ships had been avoiding the area already, and they’re now being joined by others. Alternate routes between Asia and Europe will take an extra 10 to 20 days, and “war risk surcharges” of $1,500 to more than $3,000 per container are now standard.

Air freight is in no better shape. Dubai and Doha are two of the world’s largest air cargo hubs, and both have been hit directly. Drones have damaged Bahrain’s international airport, and airspace has been closed across the region. Several major carriers—Emirates SkyCargo, Etihad, Qatar Airways Cargo, and Cathay Pacific—have suspended operations, and global air cargo capacity dropped 18 percent during the war’s first week.

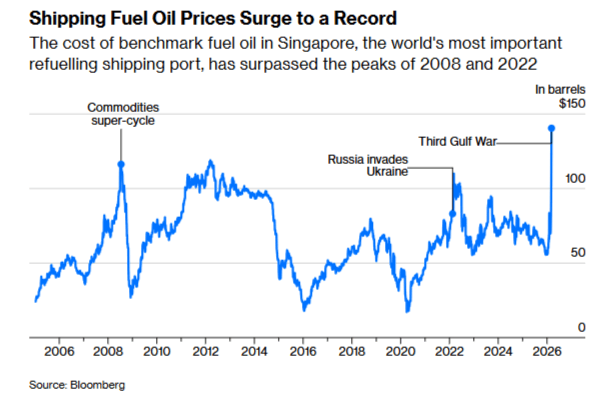

Both container ships and air freight have also faced much higher fuel costs. As Bloomberg’s Javier Blas reports, the fuel oil that powers most container vessels is getting “crazy expensive,” and supplies are running very low at several top refueling locations.

Jet fuel costs, meanwhile, have more than doubled since the Iran conflict began, affecting both shipping and tourism.

Reduced vessel capacity and higher fuel costs have caused shipping rates to spike—and the U.S. hasn’t been entirely spared. According to Pulse Logistics, for example, “air freight rates from China to the US have already climbed 15%, and we expect them to climb further if the conflict persists.” North American air cargo rates from Europe, as well as for retail and pharmaceuticals from India and semiconductors from Asia, are also up substantially. Rates for container ships from Asia to the U.S. have also risen, albeit to a less significant degree. The reason, along with higher fuel costs, is simple supply and demand: “Even if none of a shipper’s freight touches the Strait of Hormuz, they’re competing for space on a global vessel network that just got significantly tighter.” Higher shipping costs, Maersk’s CEO recently promised, will be passed on to companies and eventually make their way to consumers, at least in part.

Summing it all up.

In all these cases, and in others like them (see, e.g., zinc, nickel, copper, and uranium), the takeaways are the same as oil: The Gulf region is a major supplier of a commodity that’s priced on global markets, an essential input in numerous products made here and abroad (food, semiconductors, fabrics, etc.), and now restricted due to the Iran war. As a result, prices have increased substantially, even for goods and services not made in the Gulf or directly affected by the war.

Given these facts, it’s a(nother) testament to the global economy that markets have responded to the Iran war with only modest alarm. As DHL’s latest Global Connectedness Tracker just demonstrated again (and what I’ve argued since 2020), globalization is far more resilient than critics claim, and supply chains adjust to economic shocks far more effectively than doomsayers routinely predict. Right now, in fact, shippers are exploring alternative routes around the Gulf hostilities, producers are on the hunt for alternate supplies, insurance markets and strategic reserves are being tapped, and higher prices are encouraging conservation and substitution.

But resilience isn’t immunity. Every day the strait remains effectively closed and the war rages on, production costs rise, inventories deplete, and supply chains tighten. Farmers, chipmakers, and others are making important business decisions right now and don’t have the luxury of waiting for clarity. Uncertainty will weigh on markets and, even if the war ends soon (fingers crossed), more lasting damage has already been done. Many commodities, for example, follow a “rocket and feather” pattern—they spike fast and fall slowly—so higher prices could be with us for a while. Certain facilities, like Qatar’s damaged helium production hub or Asian petrochemical factories, will need months to restart, with supply chains only returning to “normal” several months after that. And the longer the conflict drags on, the more likely backup supplies run dry, supply chains grind to a halt, and contracts get rewritten, locking in higher prices as the new normal and seriously denting global growth. This explains Trump’s urgency to resolve the Hormuz standoff and get Gulf trade flowing again.

The Iran war has again shown that U.S. tariffs and trade barriers don’t insulate Americans from global disruptions and, by adding costs or foreclosing alternatives, can often make things worse. The president might not be able to reopen the Strait of Hormuz today, but he could remove tariffs that are compounding the supply shock. Instead, he’s actively pursuing new trade barriers—including against the same allies whose help he (apparently) needs to get Middle East trade flowing again. Apparently, the president’s desperation only goes so far.

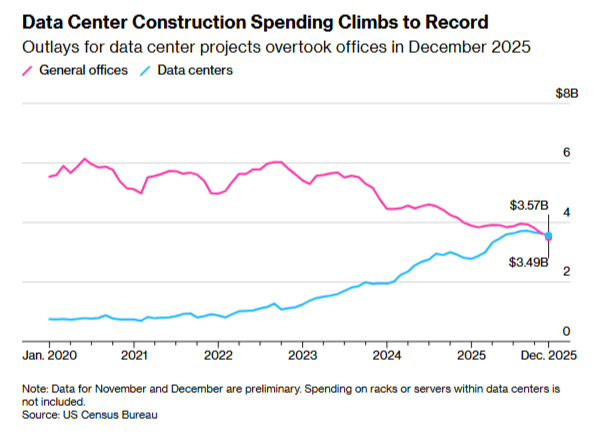

Chart(s) of the Week