In Wednesday’s episode of The Peter Schiff Show, Peter responds to the Fed’s latest rate cut, laying out why the Fed’s attempts to normalize policy have failed and how that failure ripples across markets, housing, and wages. He walks listeners through the permanence of the Fed’s bloated balance sheet, what that means for mortgage-backed securities and rate expectations, why gold still matters as a sanity check, and how market concentration and inflation interact with workers’ hopes for higher pay.

He opens by returning to an argument he made years ago about the Fed’s inability to unwind its interventions, calling out past assurances that now look impossible to keep in 2025:

Back then I said there’s no way that the Fed is going to reverse this, that this is a monetary roach motel the Fed checked in, and it ain’t never checking out. Well here we are now in 2025 and the balance sheet is 6.7 trillion, and the Fed says we’re not making it any smaller. Which proves that Ben Bernanke lied or just was completely incompetent if he actually believed what he was saying. I at least was smart enough to know that what he was saying was impossible.

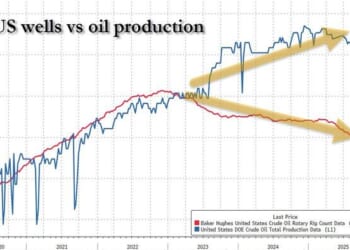

Peter then explains one technical but consequential detail about how the Fed is handling its holdings, and why that nuance matters for the housing market rather than being a small bookkeeping change:

Also what the Fed mentioned is that to the extent that bonds mature they will continue to roll over the principal. But if it is a mortgage backed security that matures the Fed won’t roll that over into more mortgage backed securities. It will roll it into treasuries. And so this instead of helping the housing market a lot of people thought that hey if we stop quantitative tightening it’s going to really help the mortgage market because the Fed won’t be selling mortgage backed securities. Well they’re not going to be buying them either.

He also breaks down the market’s reaction and what Jerome Powell’s comments mean for rate-cut expectations, noting how quickly investor bets can shift and why many still cling to hopes for a December cut:

Now before today’s announcement a December cut was virtually a lock. And so now the odds have gone down considerably, although it’s still favored. Now it’s a bit surprising that the markets didn’t react even more negatively to Powell basically rug pulling a December rate cut when the markets are pretty much banking on that. So I think maybe a lot of people believe that we’re still going to get a cut in December. I would put myself in that camp.

To show how distorted market prices can become when policy is loose, Peter points to the extreme concentration in today’s stock market and the absurdity of a single company approaching the total value of entire national exchanges:

Especially considering that today, Nvidia not only hit a new all-time record high, Nvidia now has a market cap of over $5 trillion, $5 trillion. To put that into perspective, there are only three countries in the world that have a total stock market capitalization. That means all the publicly traded stocks in the entire country. There’s only three countries where the whole stock market is worth $5 trillion, the United States and China, and the third one is Japan.

Finally, Peter tackles the perennial hope that policymakers can engineer higher wages to catch up with past price inflation, explaining why you can’t reliably inflate your way to prosperity without creating a self-defeating cycle:

So in other words, he wants more inflation so that people can get higher wages to afford the higher prices that resulted from the inflation of the past. But of course, the policies that he is pursuing to increase wages will also increase prices. So it’s going to be like a dog trying to catch his own tail. It’s never going to happen.

This article was originally published on SchiffGold.com.