On Friday, day seven of the conflict, commercial traffic through the Strait of Hormuz remained virtually nonexistent, with activity largely limited to Iranian vessels.

Unable to move crude through the waterway, JPM reminds its clients that producers have effectively shifted storage onto the sea and other facilities. Since the end of February, roughly 76 million barrels (mb) of crude have accumulated—about 46 mb on tankers, 22 mb at refiners, and 8 mb in commercial storage, or about 4.5 days of regional crude exports; most of the inventory build appears to be concentrated in Saudi Arabia.

And yet, despite disruptions around the strait, alternative export routes remain underutilized, with both Saudi Arabia and the UAE operating their bypass pipelines below available spare capacity: according to JPMorgan, roughly 1.6 mbd of spare export capacity is currently going unused.

Saudi Arabia has leaned heavily on the East–West pipeline (discussed yesterday) to bypass Hormuz and move barrels to the Red Sea. Loadings from the port of Yanbu have surged to about 2.5 mbd, up 1.8 mbd month-on-month, with an additional 1.3 mb/d flowing to refineries on the west coast.

This implies that roughly 3.8 mbd of crude is currently moving through the pipeline system, substantially below its 5 mbd nameplate capacity. The pipeline can temporarily increase its run to 6.5–7 mbd, however, logistics at Yanbu and tanker availability in the Red Sea are constraining Saudi Arabia’s ability to fully reroute Gulf exports. In the UAE, exports from the Fujairah terminal remain broadly stable, with no visible increase so far, despite the Abu Dhabi crude pipeline providing a bypass to the Strait of Hormuz with roughly 400 kbd of spare capacity.

Houthis remain a key variable. If Iran were to pursue a broader blockade effect through its regional proxies, Red Sea routes may prove less insulated than assumed.

Meanwhile, in keeping with her analysis yesterday, JPM’s Natasha Kaneva writes today that the market is shifting from pricing pure geopolitical risk to grappling with tangible operational disruption, as refinery shutdowns and export constraints begin to impair crude processing and regional supply flows. Only six days into the conflict, Iraq has already cut supply by about 1.5 mbd and Kuwait appears to be reaching tank tops. The country has reduced refinery runs by nearly 600 kbd, effectively shutting most export-oriented refining capacity and maintaining only what is needed for domestic consumption.

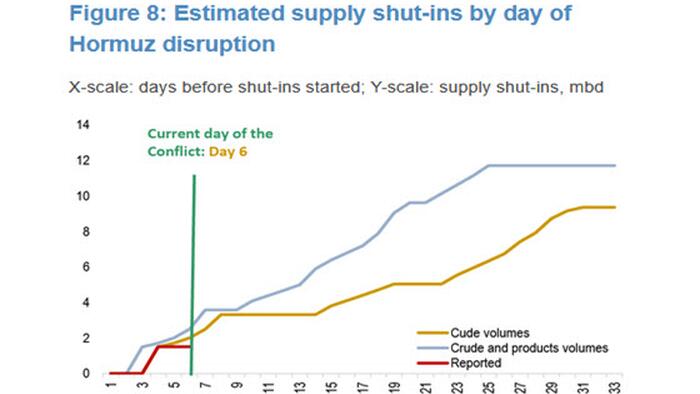

As explained yesterday, markets are now counting down to the next wave of shut‑ins, driven by export bottlenecks and refinery constraints. On current trajectories, disruptions of roughly 1.5 mbd could rise toward 3 mbd by week‑end; by the end of next week, cuts could exceed 4 mbd and potentially approach 6 mbd if refined‑product storage reaches capacity (Figure 8).

Kuwait is likely next to curtail upstream supply following today’s run cuts: based on current flows, JPM estimates about four days until shut‑ins begin, or up to nine days if product storage remains available. Beyond Kuwait, the first signs of supply constraints in the UAE should emerge next week.

Governments across Asia are already moving to protect domestic fuel availability.

- China has instructed refiners to suspend exports of diesel and gasoline.

- Japanese refiners are urging the government to consider a strategic petroleum reserve release.

- Thailand has activated an emergency energy plan and temporarily halted petroleum exports to preserve domestic inventories.

- The International Energy Agency has stated it stands ready to coordinate a global release from strategic stocks if disruptions persist, although for now the agency appears to be waiting to assess whether the closure of Hormuz becomes prolonged. The Trump administration has also indicated it is not yet considering tapping the US SPR to alleviate pressure on oil prices.

- China—which sources about 45% of its oil via the Strait of Hormuz and accounts for roughly 28% of Persian Gulf crude transiting the strait—is also reportedly urging Iran to ensure safe passage for vessels (Figure 7).

- The US has temporarily loosened sanctions against Russian oil shipments to India through April 4. Russian Urals cargoes to India are reportedly priced at a $4-5/bbl premium to Brent on a delivered basis for March-early April arrivals, reversing February’s $13/bbl discount.

The Trump administration is weighing a range of options to head off a potential energy crisis, including waivers of fuel-blending requirements and even potential US Treasury participation in oil futures markets. To reopen the Strait of Hormuz and ensure safe passage for oil tankers in the Gulf, President Trump said the US will provide insurance guarantees and naval escorts.

Still, while assurances from the US administration have helped reduce some of the risk premium in oil markets, they are unlikely on their own to restore tanker flows through the strait. The US pledges to provide insurance backstops and naval escorts will have limited impact unless Iran’s extensive disruption capabilities are first neutralized. That would require degrading Iran’s ability to threaten shipping from both the coastline and nearby islands—ranging from anti-ship missile batteries and drone launch sites to naval mines, fast-attack boats, and the command-and-control networks used by the IRGC to coordinate such operations. While US forces appear to be moving in that direction, the conditions for commercial confidence have not yet been fully established. Until they are, the oil market faces a clear asymmetry in price outcomes: prices may decline by $10 on reassuring headlines, but they could rise by $30 once Gulf production shut-ins begin to materialize and ripple through the market.

More in the full JPMorgan note available to pro subs.

Loading recommendations…