This week is all about central banks in general, and specifically the Fed decision on Wednesday which will see the continuation of the US rate cutting cycle that started exactly a year ago (two months before the election) and got as far as one 50bps and two 25bps cuts (after Trump won), with the last being 9 months ago now (after Trump won, again).

The Fed is not the only big central bank meeting this week with the Bank of Canada also meeting on Wednesday with the BoE and Norges Bank on Thursday, and the BoJ on Friday being the other main ones deciding on rates. Markets are pricing in an 85% probability of a Canadian cut, a 61% of a Norwegian one but minuscule probabilities of a change in Japan or the UK. Overall, Deutsche Bank’s Jim Reid calculates that there are 16 global central banks deciding on rates this week with Brazil and Indonesia on Wednesday the largest of the rest, with markets expecting both to stay on hold.

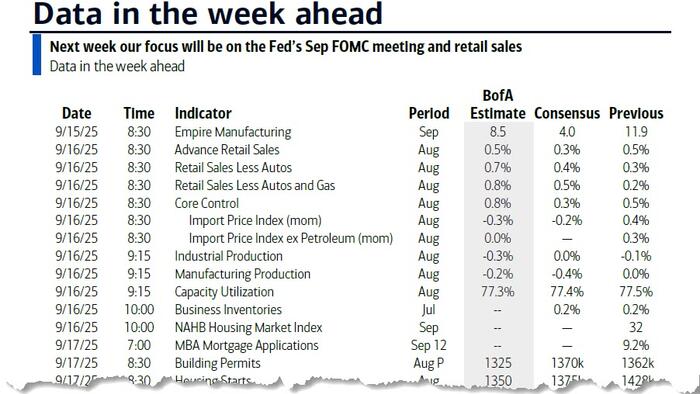

Other highlights through the week are speeches from the likes of Lagarde and Schnabel from the ECB today; US retail sales, industrial production, and the NAHB index, alongside the UK employment data, Canadian CPI, the German ZEW survey and a 20yr UST auction tomorrow; US housing starts and permits, and UK inflation on Wednesday; the US Philly Fed, jobless claims and a 10yr TIPS auction on Thursday; and Japanese CPI, German PPI and UK, French and Canadian retail sales on Friday (full day by day calendar of events below).

Previewing the Fed now: markets are pricing in 26bps worth of cuts and haven’t ever gone beyond 29bps (just after payrolls 10 days ago) for this meeting. So, assuming no big surprises, this FOMC is all about the signalling via the statement, Powell’s press conference, and the SEP. Last week, DB economists changed their view to 75bps worth of cuts this year, 25bps at each of the remaining meetings. This path would leave the fed funds rate at 3.5-3.75% by year end, consistent with their view of neutral. The weaker labor market data and slightly lower inflation than they anticipated has led them to this view, but they don’t expect further cuts in 2026 although the risks are on the downside, and much might depend on how the Fed leadership and board composition evolves. Markets are pricing in 141bps of cuts by next December, so significantly above DB’s forecasts, with Goldman among the most vocal banks expecting continued rates cuts next year.

Taking a closer look, DB economists believe that the median dot of the updated SEP will likely show 75bps of total reductions for 2025, 25bps more than in June. However, there is likely to be differing views within the committee. On the dovish side there could be three calling for a 50bp cut and possibly one or two voting for no change. It has the potential to be the first meeting where three governors dissent since 1988, and the first with dissents on both sides since September 2019.

Powell’s discussion of the labor market is likely to sound materially different compared to the July meeting and closer to his communications at Jackson Hole, but he could still allude to some of the slowdown in job gains reflecting supply-side dynamics driven by immigration policies. His tone on inflation will likely be more dovish as although August CPI was somewhat hotter than expected the details from PPI and CPI point to a more subdued reading on core PCE later this month, likely in the 20-24bps range. Overall the meeting’s most important theme will be what it signals going forward.

Courtesy of DB, here is a day-by-day calendar of events

Monday September 15

- Data: US September Empire manufacturing index, China August retail sales, industrial production, home prices, property investment, Germany August wholesale price index, Italy July trade balance, general government debt, Eurozone July trade balance, Canada August existing home sales, July manufacturing sales

- Central banks: ECB’s Lagarde, Kocher and Schnabel speak

Tuesday September 16

- Data: US August retail sales, industrial production, import price index, export price index, capacity utilisation, September New York Fed services business activity, NAHB housing market index, July business inventories, UK July average weekly earnings, unemployment rate, August jobless claims change, Japan July Tertiary industry index, Germany September Zew survey, Eurozone September Zew survey, July industrial production, Q2 labour costs, Canada August CPI, housing starts

- Central banks: ECB’s Escriva speaks

- Auctions: US 20-yr Bond (reopening, $13bn)

Wednesday September 17

- Data: US August building permits, housing starts, UK August CPI, RPI, July house price index, Japan August trade balance, Canada July international securities transactions, New Zealand Q2 GDP

- Central banks: Fed decision, BoC decision, ECB’s Lagarde, Muller, Escriva, Cipollone and Nagel speak

- Earnings: General Mills

Thursday September 18

- Data: US September Philadelphia Fed business outlook, August leading index, July total net TIC flows, initial jobless claims, Japan July core machine orders, Italy July current account balance, ECB July current account, Eurozone July construction output, Australia August labour report

- Central banks: BoE decision, Norges Bank decision, ECB’s Lagarde, Guindos, Escriva, Nagel and Schnabel speak

- Earnings: FedEx, Lennar

- Auctions: US 10-yr TIPS (reopening, $19bn)

Friday September 19

- Data: UK September GfK consumer confidence, August retail sales, public finances, Japan August national CPI, Germany August PPI, France September manufacturing confidence, August retail sales, Canada July retail sales

- Central banks: BoJ decision

Looking at just the US, Goldman writes that the key economic data releases this week are the retail sales report on Tuesday and the Philly Fed manufacturing index on Thursday. The September FOMC meeting is this week. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM.

Monday, September 15

- 08:30 AM Empire State manufacturing survey, September (consensus 4.9, last 11.9)

Tuesday, September 16

- 08:30 AM Retail sales, August (GS +0.2%, consensus +0.3%, last +0.5%); Retail sales ex-auto, August (GS +0.3%, consensus +0.4%, last +0.3%); Retail sales ex-auto & gas, August (GS +0.3%, consensus +0.5%, last +0.2%); Core retail sales, August (GS +0.3%, consensus +0.4%, last +0.5%): We estimate core retail sales increased 0.3% in August (ex-autos, gasoline, and building materials; month-over-month SA). Our forecast reflects sequentially slower measures of card spending growth. We estimate headline retail sales increased 0.2%, reflecting a decline in auto sales.

- 08:30 AM Import price index, August (last +0.4%): Export price index, August (last +0.1%)

- 09:15 AM Industrial production, August (GS -0.1%, consensus -0.1%, last -0.1%); Manufacturing production, August (GS -0.2%, consensus -0.3%, last flat); Capacity utilization, August (GS 77.4%, consensus 77.4%, last 77.5%): We estimate industrial production declined by 0.1% in August, as declines in non-auto manufacturing, natural gas, electricity and mining production outweighed a modest rebound in auto production. We estimate capacity utilization edged down to 77.4%.

- 10:00 AM Business inventories, July (consensus +0.2%, last +0.2%)

- 10:00 AM NAHB housing market index, September (last 32)

Wednesday, September 17

- 08:30 AM Housing starts, August (GS -3.0%, consensus -3.7%, last 5.2%); Building permits, August (consensus +0.6%, last -2.2%)

- 02:00 PM FOMC statement, September 16-17 meeting: We expect the FOMC to lower the fed funds rate by 25bp at its September meeting, followed by 25bp cuts at the October and December meetings and two additional cuts in 2026 for a terminal rate of 3-3.25%. We expect the statement to acknowledge the softening in the labor market but do not expect a change to the policy guidance or a nod to an October cut. We expect the median dot to show just two cuts in total in 2025 to 3.875%, though by a narrow margin, two more cuts in 2026 to 3.375%, one cut in 2027 to 3.125%, no change in 2028, and an unchanged longer-run or neutral rate of 3%. In the 2025 economic projections, we expect the median to continue to show 1.4% GDP growth, a 4.5% unemployment rate, and 3.1% core PCE inflation, all close to or in line with our own forecasts.

Thursday, September 18

- 08:30 AM Initial jobless claims, week ended September 13 (GS 236k, consensus 240k, last 263k): Continuing jobless claims, week ended September 6 (last 1,939k): After fraudulent unemployment insurance applications in Texas drove the national series sharply higher last week, we forecast a retrenchment in initial claims to their two-week-ago level of 236k.

- 08:30 AM Philadelphia Fed manufacturing index, September (GS 2.5, consensus 3.0, last -0.3)

Friday, September 19

- There are no major economic data releases scheduled.

Source: DB, Goldman

Loading recommendations…