In addition to Iran war developments, this week’s economic calendar will focus on the inflation side of the Fed’s dual mandate following a solid March employment report. The key data releases this week are the February durable goods report on Tuesday, the February PCE report on Thursday, and the March CPI report on Friday. Fed Vice Chair Philip Jefferson will deliver a speech on the economic outlook on Tuesday. The minutes to the FOMC’s March meeting will be released on Wednesday.

Briefly recapping the latest employment data, both headline (+178k vs. -133k) and private (+186 vs. -129k) payrolls far exceeded consensus expectations. To be sure, the rebound from strike- and weather-related weakness in February payrolls was somewhat less impressive due to the downtick in average hourly earnings (+0.2% vs. +0.4%) and hours worked (34.2hrs vs. 34.3hrs). The same can be said of the surprise decline in the unemployment rate (4.26% vs. 4.44%), which was largely a function of a 332k decline in unemployment, as well as a 64k drop in employment lowering the labor force participation rate by a tenth to 61.9%. Indeed, some of the strength in the March payroll gains likely came at the expense of April given the early Easter Holiday date (April 5). Averaging through the Q1 employment reports, headline (68k) and private (79k) payroll gains are tracking up from their six-month averages of +15k and 52k, respectively. In addition, the Q1 unemployment rate averaged 4.34%, a slight improvement from the six-month average of 4.395%. In addition, Q1 ADP private employment gains averaged 46k – in line with their six-month average of 45k. Lastly, jobless claims have been stable with initial claims, on average, down 3.8% from Q1 2025 and continuing claims down 0.9%. In short, the picture that Fed officials should be getting of the labor market – at least prior to the latest geopolitical developments – is one of stability, albeit at uncomfortably low levels of activity driven by a combination of supply and demand factors.

Turning to the week ahead, it’s sparse on the Fedspeak calendar: the only scheduled appearances by Fed officials are on Tuesday, when Vice Chair Jefferson and Chicago’s Goolsbee are set to give speeches on the economic and monetary policy outlook. We have heard from both officials recently, so we will be most focused on how they have internalized last Friday’s stronger-than-expected jobs report into their expectations for monetary policy. We expect that the latest data, particularly the decline in the unemployment rate to 4.26%, will reinforce the notion that the Fed is in wait-and-see mode and that risks to the two sides of the dual mandate have come into much closer balance – if they aren’t already balanced.

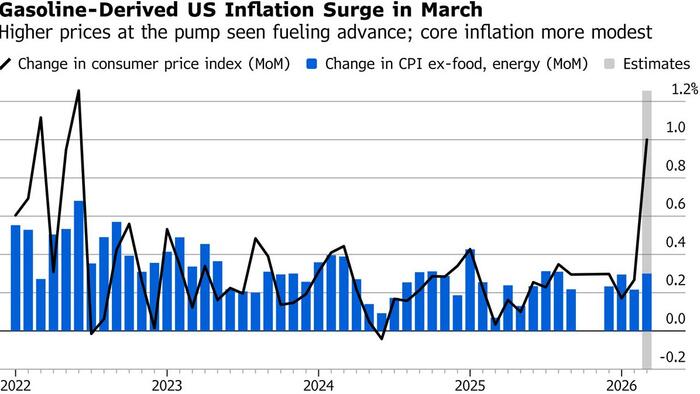

The key highlight of this week’s data docket will be Friday’s March CPI where the impact of the largest energy supply shock since the 1970s will certainly be on full display. Deutsche Bank’s expectations are for a roughly 25% increase in gasoline prices to yield a 0.95% monthly gain in headline CPI (vs. +0.27% in February), well above the bank’s forecast for the gains in core (+0.33% vs. +0.22%).

Should DB’s forecasts hit the mark, year-over-year rates for both would increase, the former from 2.4% to 3.4% and the latter from 2.5% to 2.7%. Shorter-run trends in core would also pick up under our forecast, with the three-month annualized rate rising from 3.0% to 3.4% and the six-month rate gaining three-tenths to 2.6%. In terms of the subcomponents, look for further signs of tariff-related price pressures on the goods side, particularly in apparel. Unlike prior months when declines in used car and truck prices helped to mask tariff-related increases in other core goods, this month should see lagged gains in wholesale used car prices feeding through and adding to CPI. On the services side, our focus will be on any potential bleed-through from higher gasoline prices into core, particularly from airline fares and delivery services.

Thursday’s February personal income (+0.3% vs. +0.4%) and consumption (+0.5% vs. +0.4%) release will provide monetary policymakers a snapshot of where the trend in core PCE inflation (+0.39% vs. +0.36%) stood on the eve of the Iran war. If our February forecast for the core PCE deflator – the Fed’s preferred inflation metric – is close to the mark, the three-month annualized rate will rise by 80bps to 4.5%, the six-month annualized trend will rise by 40bps to 3.5%, though the year-over-year rate should slip by a tenth to 3.00%. To be sure, some of the recent deterioration in the short-term core PCE inflation trends is due to outsized strength in some volatile goods categories. However, we expect “supercore” services inflation (+0.3% vs. +0.4%) to remain elevated in year-over-year terms (+3.3% vs. +3.5%). Indeed, supercore PCE inflation has shown virtually no improvement over the past five quarters and remains firmly above its 20-year

average of 2.7%.

Other data points this week will provide insights into business and consumer attitudes, as well as inform Q1 GDP forecasts. Monday’s services ISM (54.5 vs. 56.1) and Friday’s preliminary University of Michigan consumer sentiment (51.1 vs. 53.3) could be depressed by the latest geopolitical developments. However, the inflation components of the aforementioned surveys will likely garner more attention than the headline readings – in particular, the University of Michigan survey where we are likely to see one-year and longer run inflation expectations rise noticeably on the back of the surge in gasoline prices. While monetary policymakers would typically look through upticks in inflation driven by temporary supply shocks, that assumes that inflation expectations are well anchored. Given that the Fed has been missing on its inflation goal for the better part of the last five years, officials are acutely concerned about further increases in inflation expectations. Note that University of Michigan one-year and 5-10 year inflation expectations averaged 3.7% and 3.3%, respectively, in Q1 – roughly 40bps and 50bps above their 20-year averages (though some of that increase is due to a change in methodology).

Tuesday’s durable goods orders (-0.3% headline, +0.6% ex-transportation, +0.4% core), Thursday’s final print on Q4 real GDP (+0.7% final vs. +0.7% preliminary), as well as the above-mentioned February income/consumption release, will all inform the market’s Q1 real GDP growth forecast (currently 2.8% annualized). To be sure, the US economy is dealing with several cross currents at present and it is simply too early to determine the net impact on the broader outlook for growth this year. As Chair Powell noted at his March FOMC press conference, “a number of people mentioned, if we were ever going to skip an SEP, this would be a good one because we just don’t know.”

This week will also feature the minutes to the March FOMC meeting. As a reminder, at that meeting, the Fed held rates steady and the key elements were in line with expectations. In particular, the dot plot showed the median unchanged at one rate cut for this year and the long-run dot rose slightly to 3.1%. While Powell’s messaging skewed hawkish on inflation, he did not actively push for a balanced description of the policy outlook. DB’s takeaway was that rate cuts may be less likely but are still more likely than hikes. Within the minutes, expect to hear continued hawkish signals, with some officials pushing for more balanced language around the policy outlook, including with some openness to the potential to raise rates, as we saw in January.

The key economic data releases this week are the February durable goods report on Tuesday, the February PCE report on Thursday, and the March CPI report on Friday. Fed Vice Chair Philip Jefferson will deliver a speech on the economic outlook on Tuesday. The minutes to the FOMC’s March meeting will be released on Wednesday.

Here is a day by day summary of key events, courtesy of Goldman

Monday, April 6

- 10:00 AM ISM services index, March (GS 54.5, consensus 54.9, last 56.1); We estimate that the ISM services index declined 1.6pt to 54.5 in March, reflecting convergence to our non-manufacturing survey tracker (which declined by 0.5pt to 51.8).

Tuesday, April 7

- 08:30 AM Durable goods orders, February preliminary (GS -5.0%, consensus -1.0%, last flat); Durable goods orders ex-transportation, February preliminary (GS +0.4%, consensus +0.4%, last +0.4%); Core capital goods orders, February preliminary (GS +0.5%, consensus +0.5%, last +0.1%); Core capital goods shipments, February preliminary (GS +0.4%, consensus +0.4%, last -0.1%): We estimate that durable goods orders declined by 5% in the preliminary February report (month-over-month, seasonally adjusted), reflecting a decline in commercial aircraft orders. We forecast a 0.5% increase in core capital goods orders and a 0.4% increase in core capital goods shipments—the latter reflecting the rise in orders in recent months.

- 12:35 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will take part in a moderated Q&A on the economy and monetary policy at the Economic Club of Detroit. Moderated Q&A is expected. On April 2nd, Goolsbee said that “if [the recent increase in oil prices] is an extended increase in costs, it’d be a pretty tough supply shock for the US economy.” He also noted that the high salience of energy price increases could increase inflation expectations, which “will potentially put us into a tougher spot still.”

- 05:50 PM Fed Vice Chair Jefferson speaks: Fed Vice Chair Philip Jefferson will deliver a speech on the economic outlook at the University of Detroit. Text and audience Q&A are expected. On March 26th, Jefferson said that “the increase in energy prices to date should have relatively modest effects on inflation, though consumers are seeing higher gas prices at the pump now.” He also noted that “an extended bout of elevated energy prices could put upward pressure on a variety of other products.” Jefferson said he continued to see “our current policy stance as appropriately positioned to allow us to assess how the economy evolves.”

Wednesday, April 8

- 02:00 PM FOMC meeting minutes, March 17-18 meeting: The minutes to the FOMC’s March meeting will be released on Wednesday. The FOMC left the policy rate unchanged at 3.5-3.75% at the March meeting, and the median participant continued to project one cut in each of 2026 and 2027. We saw the meeting as a bit hawkish because only one participant dissented in favor of a cut and Powell expressed a bit less concern about the labor market than at previous meetings but took the risk from the oil price shock to inflation seriously.

Thursday, April 9

- 08:30 AM Personal income, February (GS +0.4%, consensus +0.3%, last +0.4%); Personal spending, February (GS +0.6%, consensus +0.6%, last +0.4%); Core PCE price index, February (GS +0.32%, consensus +0.4%, last +0.4%); Core PCE price index (YoY), February (GS +2.93%, consensus +3.0%, last +3.1%); PCE price index, February (GS +0.34%, consensus +0.4%, last +0.3%); PCE price index (YoY), February (GS +2.77%, consensus +2.8%, last +2.8%): We estimate that personal income and spending increased by 0.4% and 0.6%, respectively, in February. We estimate that the core PCE price index rose 0.32% in February, corresponding to a year-over-year rate of +2.93%. Additionally, we expect that the headline PCE price index increased 0.34% in February, or increased 2.77% from a year earlier.

- 08:30 AM Initial jobless claims, week ended April 4 (GS 210k, consensus 210k, last 202k); Continuing jobless claims, week ended March 28 (consensus 1,833k, last 1,841k)

- 08:30 AM GDP, Q4 third release (GS +0.8%, consensus +0.7%, last +0.7%); Personal consumption, Q4 third release (GS +2.1%, consensus +2.0%, last +2.0%): We estimate a 0.1pp upward revision to Q4 GDP growth to +0.8% (quarter-over-quarter annualized), reflecting an upward revision to consumer spending (+0.1pp to +2.1%) and stronger residential investment.

Friday, April 10

- 08:30 AM CPI (MoM), March (GS +0.87%, consensus +1.0%, last +0.3%); Core CPI (MoM), March (GS +0.28%, consensus +0.3%, last +0.2%); CPI (YoY), March (GS +3.28%, consensus +3.4%, last +2.4%); Core CPI (YoY), March (GS +2.69%, consensus +2.7%, last +2.5%): We estimate a 0.28% increase in March core CPI (month-over-month SA), which would raise the year-over-year rate to 2.69%. We expect mixed autos inflation, reflecting a 1% increase in used car prices, unchanged new car prices, and a 0.1% increase in the car insurance category. We forecast a benign 0.20% increase in the rent category, reflecting a continued slowdown in its underlying trend, but an acceleration to 0.30% in the OER category, reflecting upward pressure from the unwind of an unusually soft reading six months prior. We expect increases in the travel services categories (airfares: +4%; hotels: +0.5%), reflecting the signals from alternative price data. We expect upward pressure from tariffs on categories that are particularly exposed (such as recreation) worth +0.03pp. We estimate a 0.87% rise in headline CPI—reflecting higher food prices (+0.3%) and sharply higher energy prices (+9.4%)—which would raise the year-over-year rate to +3.28% from +2.43%.

- 10:00 AM Factory orders, February (GS -0.1%, consensus -0.2%, last +0.1%)

- 10:00 AM University of Michigan consumer sentiment, April preliminary (GS 51.5, consensus 51.8, last 53.3); University of Michigan 5-10-year inflation expectations, April preliminary (GS 3.3%, consensus 3.5%, last 3.2%)

Source: DB, Goldman