As has become customary for Monday, we have seen a dramatic surge in risk assets (3rd Monday in a row) on what at least superficially appears to be de-escalation after Trump announced strikes against Iran’s power plant would be delayed by 5 days as a result of talks with Iran, talks which at least Iran’s domestic news sources have so far denied.

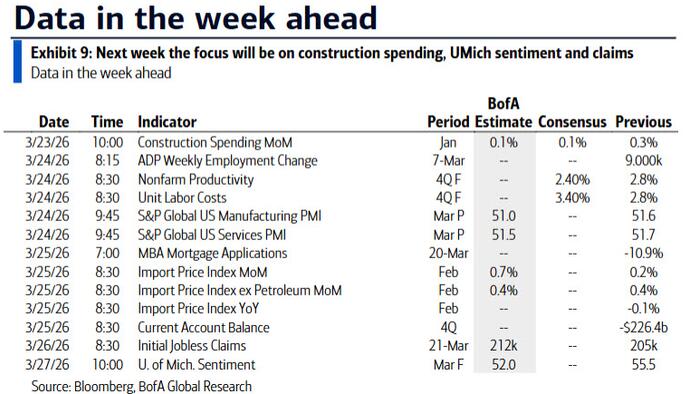

And the market lurches from headline to headline, it feels somewhat trivial to focus on the week ahead data calendar, but there will nevertheless be interest in the global flash PMIs for March, due tomorrow. As DB’s Jim Reid notes, these surveys cover the period through roughly the end of last week and should therefore be heavily influenced by developments in the conflict. Elsewhere, inflation indicators are due in the UK, Japan and Australia, although these will now be quite backward looking. The German IFO survey on Wednesday may provide another timely read on sentiment, and Lagarde’s speech the same day will also be closely watched. The week concludes with the final March reading of the University of Michigan US consumer sentiment survey, which incorporates an additional couple of weeks of responses from the initial reading. DB’s economists expect a modest downward revision to 55.0 from the preliminary 55.5 as more respondents reflect heightened geopolitical uncertainty related to Iran. More important for policymakers, however, will be the inflation expectations components. Both one year and five to ten year expectations have historically tracked energy prices closely, making them particularly relevant in the current environment.

Overall the data calendar is light in the US, and even if it were busier it would likely pale in significance relative to events in the Middle East. On the policy front, scheduled Fed appearances are limited, with only three officials due to speak. The first comes from Vice Chair Jefferson, who is set to deliver an outlook speech on Thursday. He is likely to broadly echo the themes laid out by Chair Powell at the post meeting press conference, where Powell placed greater emphasis on inflation dynamics and the outlook than on potential labor market weakness, giving the discussion a distinctly hawkish tone. Inflation, rather than employment, clearly remains the Fed’s primary concern at this stage of the cycle.

Any divergence by Jefferson from Powell’s messaging would more likely be aimed at tempering expectations of imminent tightening rather than endorsing them, particularly given the sharp repricing from roughly 62bps of cuts before the strikes on Iran to around 7bps of hikes this morning (although that number has also reversed after this morning’s newsflow). The same logic applies to remarks expected on Friday from San Francisco Fed President Daly and Philadelphia Fed President Paulson, both of whom are non voters this year and are also scheduled to deliver outlook speeches. In markets where incoming data is increasingly backward looking, there is limited value in dwelling on the remainder of the week ahead calendar, which is set out day by day at the end as usual.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 23

- Data: US February Chicago Fed national activity index, January construction spending, Japan first survey of shunto results, Eurozone March consumer confidence

- Central banks: ECB’s Escriva and Lane speak

- Other: UK PM Starmer faces the House of Commons’ Liaison committee

Tuesday March 24

- Data: US, UK, Japan, Germany, France and the Eurozone flash March PMIs, US March Philadelphia Fed non-manufacturing activity, Richmond Fed manufacturing index, business conditions, Japan February national CPI, EU27 February new car registrations,

- Central banks: ECB’s Kocher, Sleijpen, Cipollone and Lane speak

- Auctions: US 2-yr Notes ($69bn)

- Other: General election in Denmark

Wednesday March 25

- Data: US February import price index, export price index, Q4 current account balance, UK February CPI, RPI, PPI, January house price index, Japan February PPI services, Germany March Ifo survey, Australia February CPI

- Central banks: ECB’s Lagarde, Lane, Rehn and Kocher speak, BoE’s Greene speaks, BoJ minutes of the January meeting

- Earnings: Jefferies, PDD Holdings

- Auctions: US 2-yr FRN (reopening, $28bn), 5-yr Notes ($70bn)

Thursday March 26

- Data: US March Kansas City Fed manufacturing activity, initial jobless claims, Germany April GfK consumer confidence, France March business confidence, consumer confidence, Italy March consumer confidence index, economic sentiment, manufacturing confidence, Eurozone February M3

- Central banks: Norges Bank decision, Fed’s Jefferson speaks, ECB’s Guindos and Muller speak, BoE’s Breeden, Taylor and Greene speak, BoC’s Rogers speaks

- Earnings: Meituan

- Auctions: US 7-yr Notes ($44bn)

- Other: G7 foreign ministers meeting (through Friday)

Friday March 27

- Data: US March Kansas City Fed services activity, UK March GfK consumer confidence, February retail sales, China February industrial profits

- Central banks: ECB consumer expectations survey, Fed’s Daly and Paulson speak

- Earnings: Carnival, BYD

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the productivity and costs report on Tuesday and the University of Michigan report on Friday. There are several speaking engagements by Fed officials this week, including events with Governors Miran, Barr, and Cook, and Vice Chair Jefferson.

Monday, March 23

- 08:45 AM Fed Governor Miran speaks: Fed Governor Stephen Miran will appear on Bloomberg TV. On February 26, Miran said, “Four cuts [in 2026] I think are appropriate. I’d rather get them sooner than later.” Additionally, on March 6, Miran said, “Labor demand is not strong enough because monetary policy is too tight… I think the labor market could use some more support from monetary policy.”

- 10:00 AM Construction spending, January (GS +0.3%, consensus +0.1%, last +0.3%)

Tuesday, March 24

- 08:30 AM Nonfarm productivity, Q4 final (GS +1.7%, consensus +1.8%, last +2.8%); Unit labor costs, Q4 final (GS +4.3%, consensus +3.4%, last +2.8%): We estimate that nonfarm productivity growth will be revised down by 1.1pp to +1.7% quarterly annualized in the second release for 2025Q4. Since 2019Q4, labor productivity has grown at an annualized rate of 2.2%, or 2.0-2.1% after adjusting for measurement distortions in the productivity statistics, a much stronger pace than the 1.5% average pace in the pre-pandemic cycle.

- 09:45 AM S&P Global US manufacturing PMI, March preliminary (consensus 51.2, last 51.6): S&P Global US services PMI, March preliminary (consensus 52.0, last 51.7)

- 06:30 PM Fed Governor Barr speaks: Fed Governor Michael Barr will speak on the economic outlook and community development at the National Community Investment Conference in Phoenix. Speech text is expected. On February 17, Barr said, “Based on current conditions and the data in hand, it will likely be appropriate to hold rates steady for some time.” He also said, “With very low levels of job creation and also a low firing rate, there seems to be a tentative balance in labor supply and demand. But it is a delicate balance, and that means that the labor market could be especially vulnerable to negative shocks.”

Wednesday, March 25

- 08:30 AM Import price index, February (consensus +0.6%, last +0.2%); Export price index, February (consensus +0.6%, last +0.6%)

- 04:10 PM Fed Governor Miran speaks: Fed Governor Stephen Miran will participate in a conversation on digital assets at the 2026 Digital Asset Summit in New York.

Thursday, March 26

- 08:30 AM Initial jobless claims, week ended March 21 (GS 205k, consensus 210k, last 205k); Continuing jobless claims, week ended March 14 (consensus 1,853k, last 1,857k): We estimate that initial jobless claims were unchanged around 205k. Initial claims remain below their average level in 2025H2 and the layoff rate edged down in January, suggesting that nationwide layoffs remain low despite the increase in alternative layoff measures in Q4 of last year.

- 04:00 PM Fed Governor Cook speaks: Fed Governor Lisa Cook will speak on financial stability at the Yale School of Management. Speech text and Q&A are expected. On February 4, Cook said, “[Recent] readings indicate that progress on inflation essentially stalled in 2025… After nearly five years of above-target inflation, it is essential that we maintain our credibility by returning to a disinflationary path and achieving our target in the relatively near future.” She also said, “The labor market is roughly in balance, but I am highly attentive to developments, knowing it can shift quickly.”

- 06:30 PM Fed Governor Miran speaks: Fed Governor Stephen Miran will speak on the Fed’s balance sheet at the Economic Club of Miami. Speech text and Q&A are expected.

- 07:00 PM Fed Vice Chair Jefferson speaks: Fed Vice Chair Philip Jefferson will speak at the Dallas Fed. On February 6, Jefferson said “I am cautiously optimistic about the economic outlook. I see signs suggesting that the labor market is stabilizing, that inflation can return to a path toward our 2% objective, and that sustainable economic growth will continue.”

- 07:10 PM Fed Governor Barr speaks: Fed Governor Michael Barr will participate in an event at the Brookings Institution. Speech text and Q&A are expected.

Friday, March 27

- 10:00 AM University of Michigan consumer sentiment, March final (GS 52.0, consensus 54.0, last 55.5): University of Michigan 5-10-year inflation expectations, March final (GS 3.5%, last 3.2%)

- 11:30 AM San Francisco Fed President Daly (FOMC non-voter) speaks: San Francisco Fed president Mary Daly will give introductory remarks at the San Francisco Fed’s Macroeconomics and Monetary Policy Conference. On March 6, Daly said, “We really have to keep our eye on the labor market. But we also have inflation printing above our target and oil prices rising. How long it will last we don’t know. But both our goals are at risk now and we have to keep our eye on both.”

- 11:40 AM Philadelphia Fed President Paulson (FOMC voter) speaks: Philadelphia Fed president Anna Paulson will give remarks at the San Francisco Fed’s Macroeconomics and Monetary Policy Conference.

Source: DB, Goldman