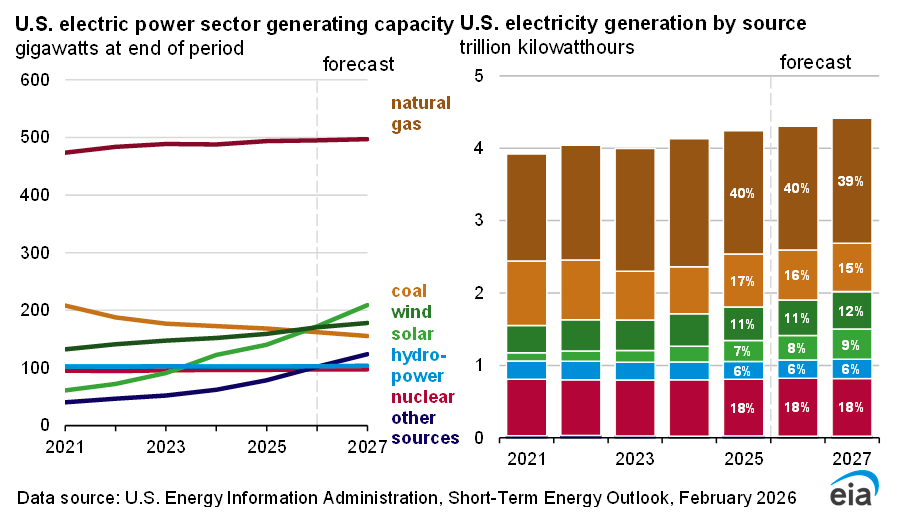

While natural gas is preferred by data centers and manufacturers, the Energy Information Administration (EIA), in its Short-Term Energy Outlook, reports that solar power is expected to supply the largest increase in power generation over the next two years, increasing by about 20% a year in both 2026 and 2027, following the addition of almost 70 gigawatts of new solar capacity. Solar and wind developers are rushing to bring online new capacity before the One Big Beautiful Bill Act phases out the Biden administration’s Inflation Reduction Act’s tax credits for renewables. Under the act, tax credits pay for as much as 30% of the cost of solar installations. Solar also has other challenges, including hefty land requirements, intermittency, and grid integration issues, requiring hard-to-source transmission lines to get power from generation sites to demand centers.

Natural gas, however, is still the major source of generation and the fuel of choice for data centers and manufacturers, supplying around 40% in both 2026 and 2027, according to EIA’s forecasts. Solar is expected to supply less than 10% as it is not as efficient, providing only about a quarter of the energy that natural gas can supply with the same amount of capacity. EIA projects only three gigawatts of new natural gas capacity coming online in 2026 and 2027.

According to the Federal Energy Regulatory Commission (FERC), U.S. utilities installed about 4.5 gigawatts of natural gas capacity in 2025, and the agency is forecasting that 44.9 gigawatts of proposed new capacity, including 22.7 gigawatts of high-probability projects, will come online in the near future. Those figures are more than the 12.7 gigawatts of gas retirements FERC expects through November 2028. Natural gas currently makes up 42% of the installed electric-generating capacity in the United States, with wind making up 11.9% and solar, 12%. As mentioned above, capacity numbers are not comparable, as both wind and solar are less efficient than natural gas, only performing when the wind is blowing and the sun is shining.

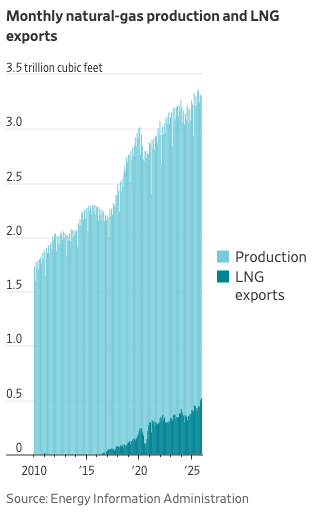

Due to the shale drilling boom, U.S. natural gas production continues to reach new records, and the United States is now the world’s largest exporter of liquefied natural gas, but manufacturers still are cut off from natural gas supplies during extreme weather days due to insufficient pipeline capacity because priority goes to residential customers when demand rises. That is also why the Northeast had to rely on oil for 40% of its electricity generation during Arctic storm Fern last month. Due to long-term supply deals guaranteeing space on pipelines, overseas buyers are also not cut off from supplies.

Manufacturing Gas Curtailments

The Wall Street Journal reports that pipelines, curtailed or otherwise, restricted the flow of gas to manufacturers more than 40 times last year. Paul Cicio, chief executive of Industrial Energy Consumers of America, expects it may be worse this year. Some manufacturers had to wind down their operations when high gas prices made their operations unprofitable. On-the-spot gas deliveries at trading hubs in areas hardest hit by Fern soared to some of the highest prices on record.

According to the Journal, Cicio’s organization asked FERC to shorten the length of pipeline supply contracts to a few years, from more than a decade, since very few industries can make a commitment lasting that long. The group also requested that the Energy Department restrict uncontracted LNG shipments during heat waves and winter storms. American manufacturers have a large advantage over global competitors due to cheap natural gas fueled by the shale gas boom, but supply interruptions interfere with that advantage, particularly when they can last up to a week as they did for some manufacturers during winter storm Fern.

Data Center Electricity Demand

Via the World Resources Institute, data centers are being accused of increasing electricity demand and causing electricity prices to escalate. According to Rystad Energy, the United States is expected to have over 100 gigawatts of data center demand coming online between 2024 and 2035, which is about 10 times New York City’s summer peak demand in 2023, when air conditioners were operating at full blast. In comparison, an Electric Power Research Institute paper from 2024 found that electricity demand for data centers could consume anywhere between 4.6% and 9.1% of all U.S. electricity generation by 2030. The difference with the Rystad projection is around 200 terawatt-hours. Most data center use projections through 2030 range from 200 terawatt hours per year to over 1,050 terawatt hours per year, with most being between 300 and 400 terawatt hours. One study, however, found no evidence of national electricity demand growth, but certain regional and utility demands are expected to increase.

Clearly, the amount of demand arising from data centers is still a question mark. But, unlike the technology boom in the 2000s, most forecasters believe there will be an increase, although by how much is unknown.

Analysis

Data centers want reliable power, not power produced from intermittent wind and solar sources. Developers require sources that can power these centers decades into the future and are, therefore, looking to natural gas generation, either from utilities or from dedicated on-site sources.

Moreover, data center demand is not the primary driver of higher electricity rates. For instance, Texas and Virginia have built more data centers than anyone else and their electricity rates are below the national average. As IER’s Alex Stevens and Samuel Peterson explain for the Washington Post, “The machines aren’t the main problem. The red tape strangling the U.S. grid is. Remove it, and America can have both cutting-edge AI and abundant electricity.”

For inquiries, please contact [email protected].