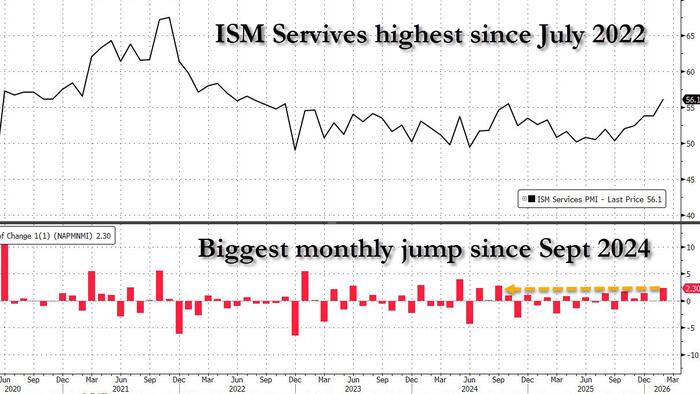

After the Manufacturing ISM print earlier this week came modestly stronger than expected (albeit with the Prices Paid component spiking and sending 10Y yields higher), some were expecting a similar improvement in today’s Services ISM print. What they got instead, was a blowout number, and one suggesting that whatever weakness the US economy was in for much of the latter part of 2025, is now over.

At 10:00am ET, the ISM Services print came out at 56.1, the highest print since July 2022, and was 2.3 higher than the 53.8 reported in January – the biggest monthly increase since Sept 2024

Economists expected a print of 53.5. Not only did the number come above the highest estimate, it was a six-sigma beat to the consensus estimate.

The breakdown shows improvements across virtually every category (a decline in prices paid is actually a good thing, as it means less inflation/stagflation risk).

Digging into the report we find that three demand indicators (the New Orders, Backlog of Orders and New Export Orders indexes) are in expansion, and the Customers’ Inventories Index remains in ‘too low’ territory, contracting at a slightly slower rate. That said, a ‘too low’ status for the Customers’ Inventories Index is usually considered positive for future production.

Regarding output, the Production Index is in expansion for the fourth month in a row, and the Employment Index, though still in contraction, improved by 0.7- percentage points. However, 45% of panelists still indicate that managing head counts is the norm at their companies as opposed to hiring.

Finally, inputs (defined as supplier deliveries, inventories, prices and imports) all increased since the previous month’s reading. The Supplier Deliveries Index indicated slower deliveries, Inventories Index contraction has slowed, and the Prices Index took a huge leap to 70.5 percent from 59 percent in January.

And while both employment and new orders posted gains, perhaps the most important indicator was that Prices Paid tumbled from 66.6 to 63.0, the lowest print in 11 months.

Here is a snapshot of what the ISM respondents are saying:

- “India tariffs are anticipated to provide some measure of cost relief once current inventory levels are worked through. At a high level, we are addressing price/value perception which continues to drive negative sales impact.” [Accommodation & Food Services]

- “Our industry seems to have adapted to the tariffs. The costs are embedded into the import cost the company has to shoulder.” [Agriculture, Forestry, Fishing & Hunting]

- “Residential homebuilding continues to lag due to affordability and interest rate issues. While we saw improved sales last month due to further discounts, we struggled to achieve similar results in February. More material cost increases have rolled in for beginning of the second quarter, so margins continue to be reduced.” [Construction]

- “Higher education institutions are operating cautiously due to enrollment fluctuations and uncertainty in state and federal funding and name, image and likeness licensing. While supply chains have improved, costs remain high for technology, facilities, utilities, and contracted services. Labor expenses are also increasing due to competitive hiring. As a result, purchasing decisions are focused on essential needs, cost control, and maintaining key operations, with some noncritical projects being delayed.” [Educational Services]

- “Tariff volatility and shifting bilateral trade agreements are materially impacting our purchasing operations. Changes in U.S. semiconductor supply constraints continue to pressure component pricing and availability. The combination of tariff exposure and semiconductor market instability is increasing procurement risk, compressing margins, and requiring more aggressive supplier diversification and contractual protections to maintain cost competitiveness.” [Mining]

- “The business climate remains solid overall, but significant unknown risks from further potential tariff actions by the U.S. government are dampening business investment.” [Real Estate, Rental & Leasing]

- “Due to random-access memory shortages, we are seeing increased cost and lead times from key technology providers. Quotes that were normally secure for 90 days are now 30 days or less.” [Retail Trade]

- “Transportation/truck capacity has been extremely tight, causing rates to spike 30 percent to 40 percent. Some of this can be attributed to the weather; some can be attributed to the Federal Highway Administration’s push to make sure all drivers are proficient in English and others can be attributed to an increase in commerce.” [Transportation & Warehousing]

- “Mid-first quarter business conditions are good. The unseasonable cold weather has helped to increase demand and boost revenues. All else is on track so far.” [Utilities]

- “Overall, our business performance in January and February has been solid (minus some winter storm hurdles). Our upstream oil and gas business has stalled for two years and is not supporting our growth. On the other hand, all data center-related activity continues to grow substantially. Downstream is always steady, but we are taking more market share within it. The business here is busy. All industries are doing well, minus the oil field business.” [Wholesale Trade]

The report listed the following commodities as going up in price: Cement Products; Chips; Computers; Copper (3); Fuel; Labor (7); Lumber (2); Memory Products (2); Software; Software — Licensing; Software Maintenance; and Wire & Cable.

There were two commodities that dropped in price: Diesel Fuel (3); and the all important Gasoline which is now down 12 months in a row.

Commenting on today’s ISM report, Bloomberg says that it comes as close as it possibly can to goldilocks as “the headline reading posted its highest level since the summer of 2022, with lower-than-expected prices paid (63 versus 68.3 forecast) and nice jumps in new orders and employment, both of which comfortably exceeded market forecasts. If you are a believe that AI will drive non-inflationary growth, this is the survey for you, and it’s given equities a bit of a fillip as a result.”

Judging by the positive market reaction which has sent stocks sharply higher after the report, the market agrees.

Loading recommendations…