As we highlighted in our regional bank meltdown summary post, there was a common theme between the two banks that got hammered yesterday, ZION and WAL: a single bankrupt counterparty that led to bad debt impairments at both banks. Now, thanks to Bloomberg, we can identify who that counterparty was.

According to BBG, the bad loans reported by Zions Bancorp and Western Alliance Bancorp can be traced back to the bankruptcy of one commercial real estate investment firm in Southern California earlier this year. In the lawsuit filed on Wednesday – which also spooked investors and sent the stock plunging – Zions listed 16 addresses of properties pledged as collateral to more than $60 million loaned to an investor group. And when the Newport Beach, California-based real estate firm MOM CA Investco LLC filed for bankruptcy in February, six of those properties were listed as investments.

So what happened with the loans?

Well, as Bloomberg reports, back in 2016 and 2017, when bankers at Zions subsidiary California Bank & Trust underwrote the loans they made sure the usual cushion to protect the lender was in the contract: Zions should be first in line for repayment should the borrower default and liquidate its assets, according to this week’s complaint, filed in LA County Superior Court against defendants including Gerald Marcil, Andrew Stupin and Deba Shyam.

But two things went wrong simultaneously. First, MOM CA Investco filed for bankruptcy protection, leading to a planned sale of some its properties. Second, it turned out that, for those buildings that served as collateral for the loans Zions issued, other firms actually were ahead in line of the Salt Lake City-based bank to be paid should the real estate be liquidated.

A similar situation hit Western Alliance. The Phoenix-based bank sued an investor group including Marcil and Stupin, claimed they manipulated loan structures in a way that wrongly stopped the lender from receiving debt repayments before anyone else.

Western Alliance said the investor group still owes it more than $98.6 million. Those loans were meant to be secured by real estate in Stupin and Marcil’s investment funds, but the properties were already in foreclosure, which wasn’t disclosed to the bank, according to a complaint filed in August in Los Angeles.

In response, Marcil and Stupin’s lawyer said in a statement that “my clients vehemently deny all the allegations of wrongdoing… These claims are unfounded and misrepresent the facts. We are confident that once all the evidence is presented, our clients will be fully vindicated.”

Digging deeper we find that behind the bankruptcy of MOM CA Investco is a group of Southern California commercial real estate investors who were friends before they became foes in court. The firm’s portfolio included a hotel in the exclusive enclave of Laguna Beach and an apartment complex worth $65 million in the town of Redlands, according to the February bankruptcy filing.

The MOM CA Chapter 11 was dismissed in August. In the weeks leading up to the dismissal, the federal judge overseeing the case warned the property investors that the inability to get a deal wasn’t in their interest. And throwing the case out of bankruptcy, said US Bankruptcy Judge Brendan Shannon said, wasn’t the best option.

That’s because, once the case was over, creditors would be free to file actions in state court to try seize various properties and sell them at fire-sale prices. After several court hearings in which the two main players in the real estate empire remained at odds, Shannon dismissed the Chapter 11.

Mohammad Honarkar and Mahender Makhijani founded MOM CA Investco in 2021 as a joint venture. At the time, Honarkar also ran a business selling mobile phones, while Makhijani acquired and managed distressed real estate for investors through an entity called Continuum Analytics. Among the largest investors in Continuum were Marcil and Stupin, and its legal owner is Shyam.

But the partnership soon went south, with Honarkar accusing his partners, who controlled the company, of fraud. At one point during their dispute, Makhijani used armed guards to take over some of the properties, and hired mobile billboards to drive around Laguna Beach displaying pictures of Honarkar and accusing him and two city employees of corruption, according to court filings.

It gets even more bizarre: the investors sued by Zions and Western Alliance, Marcil, Stupin and Shyam, have additional ties to a variety of investment vehicles linked to Makhijani, court filings show. The three were among the founding investors of Nano Banc, for which Makhijani is one of the largest referral sources.

Nano Banc had loaned the founders more than $100 million, according to a March arbitration filing. And Zions found that for one property it had a first lien on, a building in Laguna Beach, the deeds were assigned to Nano Banc.

And the piece de resistance: another asset, an apartment complex in Bellflower, had a deed assigned to the other bank suing the investors: Western Alliance.

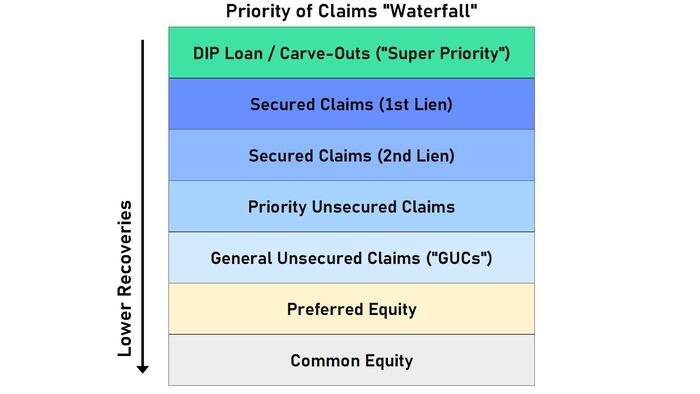

In short: unprecedented chaos… but it wasn’t just a busted bankruptcy and potential fraud on behalf of a shady investor group. It was also a bizarre absolute priority rule waterfall shitshow, in which nobody knew whose claims were subordinated or priority, and the result was a free-for-call collateral grab which was not quite rehypothecation, but was very close, and the result is that the secured lenders – Zions and Western Alliance – have now ended up chasing the assets pledged to their loans in court as the assets are, as the South Park cartoon puts it so well, gone… all gone.

The good news is that we now know what happened in this particular case. The question now is why did the banks not figure all of this ahead of time, and more importantly, how many more such instances of a manged absolute priority rule are there?

Loading recommendations…