Life, Liberty, Property #114: Fiat Money and the Phony Housing Boom

Forwardthis issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

IN THIS ISSUE:

Fiat Money and the Phony Housing Boom

Video of the Week: Peace vs. Big Government – In The Tank #507

Young U.S. Adults Missing Milestones

Poor, Poor Pitiful UBI Performance

Cartoon

Bonus Video of the Week: COVID Was the Test Run… Climate Lockdowns Are the Goal (Guest: Matthew Wielicki) — TCRS #170

Fiat Money and the Phony Housing Boom

Decades of devaluation of the dollar through inflation have created a phony housing boom that’s impeding homeownership.

There is a simple reason why housing costs so much more these days, in real terms, than in decades past, writes economic historian Brian Domitrovic at Forbes:

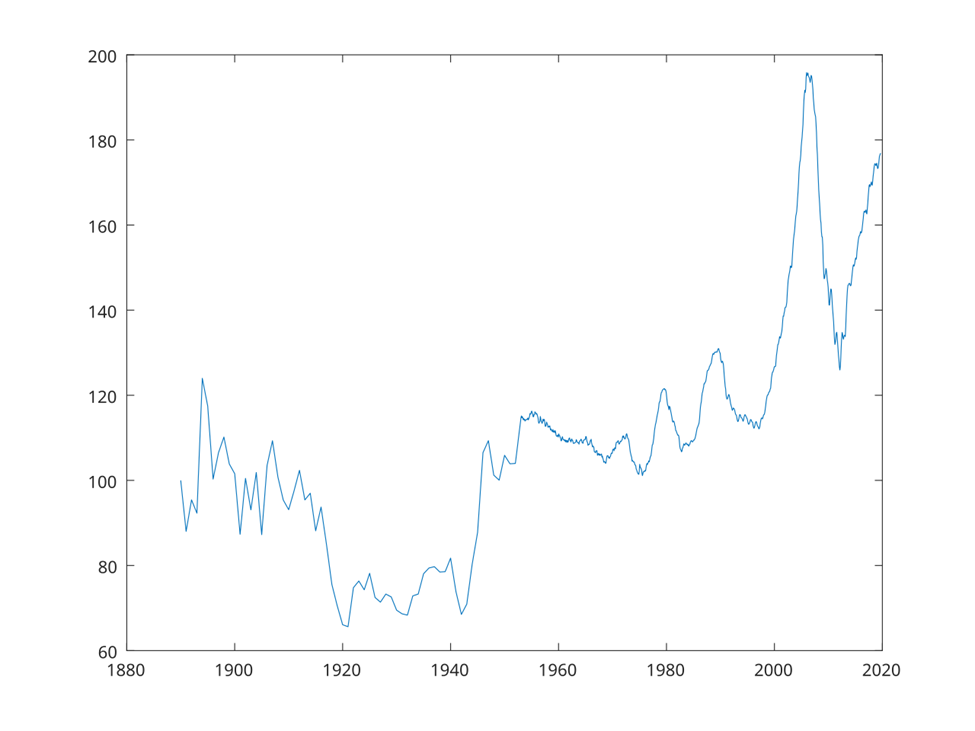

The full Case-Shiller [U.S. housing price] index going back to 1890—not 1980, 1890—tells a tale. Home prices were generally flat, actually going down a little (check out the modernization of this index on page 23 here), for three quarters of a century until the late 1960s. Then home prices went up by over 50 percent in the 1970s. This is all in real terms, adjusted for inflation. In the 1980s they dipped down, recovered a little in the 1990s, and then powered up like never before in the new millennium.

Wait, home prices generally modestly declined for seventy-five years from 1890 to 1965? You read that right. For the bulk of American history, as our best evidence has it, the trend for home prices was down. This stuff about home prices soaring is exclusively a story of basically 1970 to the present.

To paraphrase the famous X feed, What the devil happened in 1971? That’s when we went off the gold standard. Here is the origin of the housing crisis.

Here’s what the Case-Shiller chart looks like:

Source: The Case–Shiller Real Home Price Index, with values from 1890 until August 2019. By Gabbe—own work, CC0, https://commons.wikimedia.org/w/index.php?curid=50996877. Created with Octave 4.4.0 based on data from http://www.econ.yale.edu/~shiller/data.htm

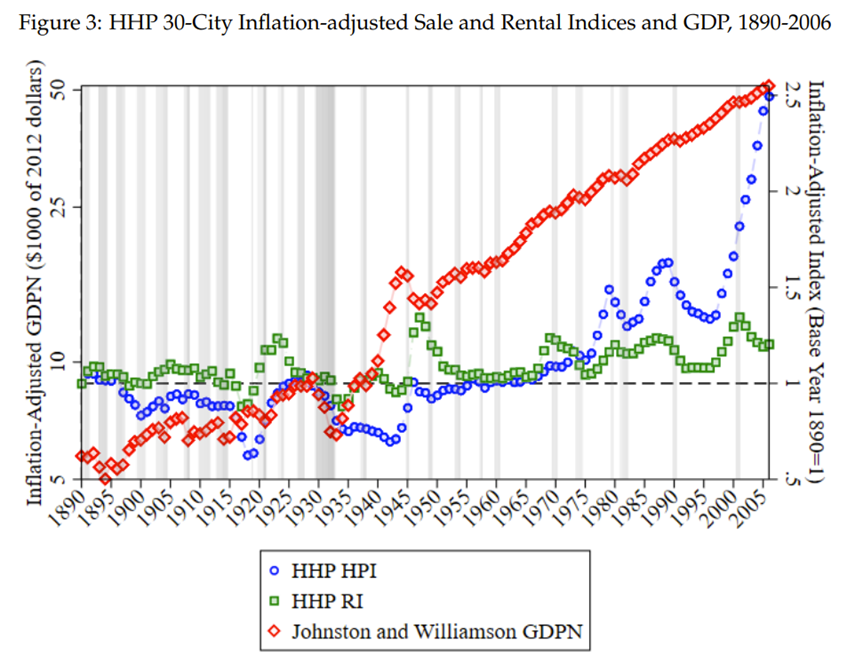

Here’s the chart Domitrovic refers to above; it is really stunning:

Note: This figure shows the baseline national HHP sales and rental indices against the Johnston & Williamson (2008) GDP per capita measure, with the indices based to 1890 and GDP per capita expressed in 1890 dollars. Intensity of recession indicated by gradient of shading from light (minor) to dark (major). Left y-axis is log scaled.

The fiat-money system that President Richard Nixon established in 1971 continually devaluates the dollar and forces people to put their money in harder assets to the extent possible, to avoid deterioration of dollar-denominated asset holdings. That, in turn, raises the prices for such assets. For most people, the biggest asset they have is their house and the land on which it sits. The ever-shrinking value of the dollar turns every household into a mini hedge fund.

Thus, the fiat-money system relentlessly pushes up the demand for housing and (ceteris parabis) the cost of housing, Domitrovic explains:

Going off gold prompted mass dubiousness about currencies and sparked interest in currency hedges. This new state of affairs has waxed and waned, generally waxed, for fifty some years now. Any asset or useful product limited in supply by geology—land (the basis of housing), gold, oil, you name it—has attractive hedge characteristics in a non-gold standard environment. These hedge characteristics were not apparent, not relevant before the late 1960s, when it became clear the money masters were going to make the gold standard kaputt. Stable low-priced housing for the age before, big time housing bubbles after.

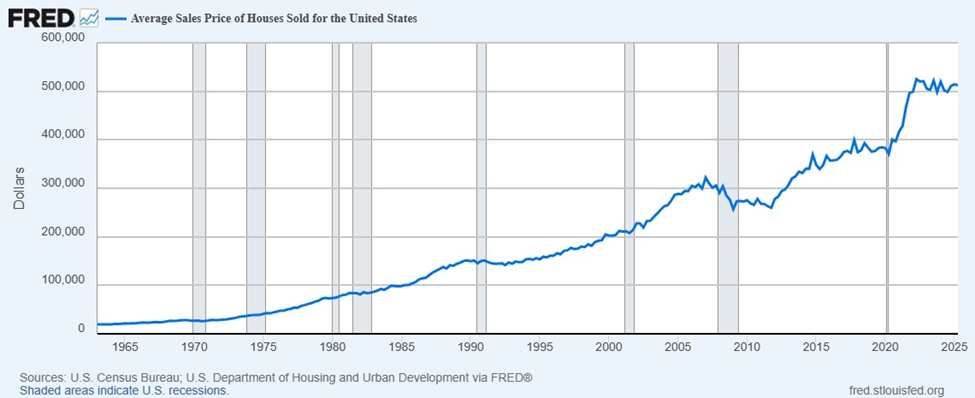

This chart from the St. Louis Fed illustrates the stunning rise in nominal housing prices as the dollar has consistently declined in value since 1971 (the chart for the median price looks the same, in case you’re wondering):

If we had “a real currency system,” people would allocate less of their portfolio to housing, Domitrovic notes, and thus the continual devaluation of the dollar through inflation is distorting the market radically:

The predicament today is that the normal person’s financial/asset portfolio has an outsized share of housing (or fails to because it is too expensive) because the premium continues to attach to hedging the fiat monetary system. Who talks about going back on gold today? Nobody? Then cue the housing boom.

Domitrovic argues that Bitcoin can solve this problem by serving as a reliable, reality-based alternative to the U.S. dollar, with proponents basically saying, “if you are not going to return to classical money, we’ll force you,” as Domitrovic puts it:

Here’s the future of housing prices. As Bitcoin either forces the world back on to classical money or becomes the approximation of classical money itself, dispatching fiat to the ash-bin of history, the demand for hedges against the whole currency system will fall. Housing is one of the first examples of these hedges. Living quarters will revert to normal pricing, housing will fall as a share of portfolios, everyone will be snug as a bug in a great place, and we will be off to better uses of our time and energy and resources.

Whatever the solution may be, it is clear that the fundamental unsoundness of the U.S. dollar since 1971 has created enormous economic distortions, which also create social problems. Only establishment of a reality-based currency can solve that massive problem.

Just because a war is abroad—and between countries other than your own—doesn’t mean it won’t have impacts at home. In the USA, history shows that U.S. intervention in foreign wars increases federal intervention in our everyday lives; constant involvement in wars has led to much of the creeping expansion of our government over time. The whole world seems to be watching as Trump attempts to broker a peace deal between Russia and Ukraine. We’ll talk about why it’s good for domestic freedom that Trump is resisting getting the U.S. directly into the war.

Moving out of the parental home, getting a job, tying the knot and having kids used to be the most common pathway to adulthood, with almost half of 25- to 34-year-olds having experienced all four milestones in 1975.

Nearly 50 years later, less than a quarter of U.S. adults this age had done the same.

Referring to these milestones as “the traditional pathway to adulthood,” CBS News summarizes the paper as finding “more young adults between the ages of 25 and 34 are facing economic barriers compared with previous generations,” and “[c]hanging societal attitudes around family formation are also contributing to the sharp decline in the share of young people reaching what the U.S. Census Bureau considers to be ‘key milestones.’”

Representative of the reaction to this report and the media coverage is writer Michael Snyder at ZeroHedge:

What I am about to share with you is some of the clearest evidence yet that the middle class in America is being systematically destroyed. Young adults are forming middle class households at an extremely depressed rate, and that is because the American Dream is simply out of reach for most of them in this very harsh economic environment. If you can’t get a good job that pays an adequate wage, you aren’t going to be able to live a middle class lifestyle. Sadly, many older Americans simply do not understand how difficult things have become for our young adults in this day and age.

The U.S. economy is not serving middle-income people the way it used to, Snyder argues:

If our society was in good shape, most of our young adults would be in a position to achieve all 5 milestones by the age of 25.

But our society is not in good shape. According to the Census Bureau paper, the primary reason why young adults are not achieving these milestones is because they are “facing economic barriers” …

Snyder argues that today’s young people want decent jobs, but many cannot get them:

To be a part of the middle class, you have to be able to get a middle class job.

And right now the competition for middle class jobs among our young people is extremely fierce.

If you doubt this, just consider what a 23-year-old college graduate recently admitted to NBC News…

“Every guy I know that is without a job right now wants to work, but they just can’t get it,” said Eli McCullick, who has been looking for a job for more than a year after he graduated with a degree in sociology from the University of Colorado Boulder. “It’s demoralizing for guys who really want to get ahead and it’s just not happening.”

McCullick, 23, said he hasn’t even been able to get an hourly job at a restaurant or doing cleaning work at a hotel in the Boulder area, where he’s living at a property his father owns. The only way he has been able to earn money to cover his food and daily expenses has been to do odd jobs for friends and relatives, like shoveling horse manure, mowing lawns and helping an older woman prepare for a yard sale.

There is no way that I would want to be a fresh college graduate looking for a job right now.

It is terrible out there.

Unemployment is on the rise and is hitting young people the hardest, Snyder writes:

Those that keep insisting that “everything is fine” just need to stop.

Layoffs have risen 140 percent from a year ago, a new report reveals.

Companies have already announced more than 800,000 job cuts this year alone, the highest since the pandemic upended the economy in 2020.

US-based employers cut 62,075 jobs in July compared to 25,885 in the same month last year.

Those numbers are staggering.

This is a “very harsh economic environment,” and workers are fearful, Snyder says:

That may help to explain why “job hugging” has become a thing in 2025…

Job hugging is the act of holding onto a job “for dear life,” consultants at Korn Ferry, an organizational consulting firm, wrote last week.

The rate at which workers are voluntarily leaving their jobs—known as the quits rate—has hovered around 2% since the start of the year, according to data from the U.S. Labor Department’s Job Openings and Labor Turnover Survey. Outside of the initial days of the Covid-19 pandemic, levels haven’t been that consistently low since early 2016.

The quits rate is a barometer of workers’ perceptions of the broader labor market, said Laura Ullrich, director of economic research in North America at the Indeed Hiring Lab. In this case, they may be nervous about getting another job or aren’t enthusiastic about their ability to find one, she said.

Snyder’s concerns are valid, even if much of what he writes in his article is anecdotal. The composition of the U.S. economy has certainly become grossly distorted in the 54 years since President Richard Nixon fully divorced the U.S. dollar from its last tenuous connections to gold in 1971.

Fortunately, the situation is not quite as dire as Snyder and others suggest. Crucially, Snyder is confusing short-term facts with long-term ones. The U.S. economy is certainly in a difficult recovery from the damage done by grossly expanded government spending and regulation in 2021 through 2024, which is a short-term problem, and a big one. (I think we are headed for a recession, though it is possible to avert it.)

Getting the U.S. economy into more-normal conditions would alleviate the employment problems to which Snyder refers.

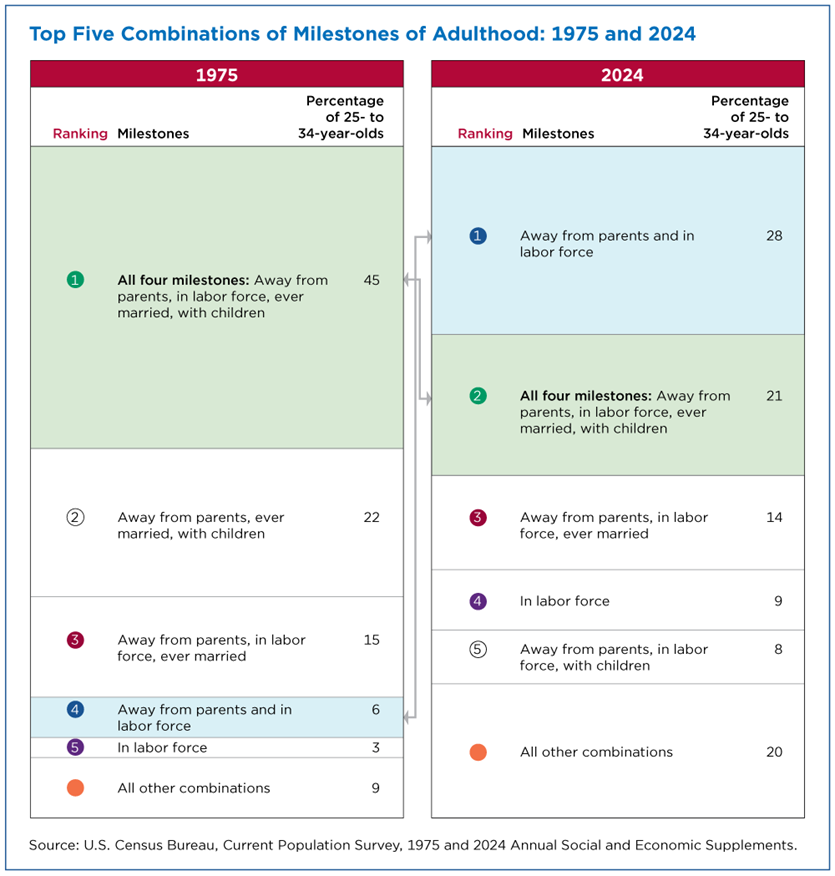

Even more important to Snyder’s point, however, is that getting a job and moving out of the family home are not what is driving the change in milestone accomplishment. The key deficiency is in marriage and having children, as this table from the study authors’ press release shows:

The factor keeping young people from establishing traditional bourgeois lives is not the cruel American economy; it’s their own choice to put off marriage and family. Young U.S. adults are successfully entering the labor force while choosing to delay getting married and having children, the Census working paper states:

Changing economic opportunities and attitudes toward family formation have contributed to new experiences during young adulthood. Results from Figure 1 [“Top Five Combinations of Milestones,” above] provide evidence of a divergence in the types of milestones young adults achieve. Specifically, as the proportion of young men and women who experienced economic milestones (such as labor force participation and completed education) increased, the proportion who formed a family through marriage or parenthood declined. These patterns reflect the notion that young adults continue to prioritize economic security over starting a family. Furthermore, the diverging trends between economic and family formation milestones could suggest the perceived economic bar to marriage and parenthood are [sic] shifting such that contemporary young adults feel the need to achieve higher levels of economic security before starting a family than their counterparts did 18 years earlier.

It is unfair to expect people to take lifechanging steps such as marriage and having children when they cannot feel secure in their household prospects. Housing costs pose significantly more difficulty than in previous years for young people setting out in life, the Census working paper states. The significant rise in crime and social disturbance in the past decade creates an added economic burden (even if we accept the reports of recent decreases in crime, which I find dubious). Childless people might feel comfortable in funky, less-safe neighborhoods, but those raising children do not, and they therefore have a much-higher cost of housing to meet.

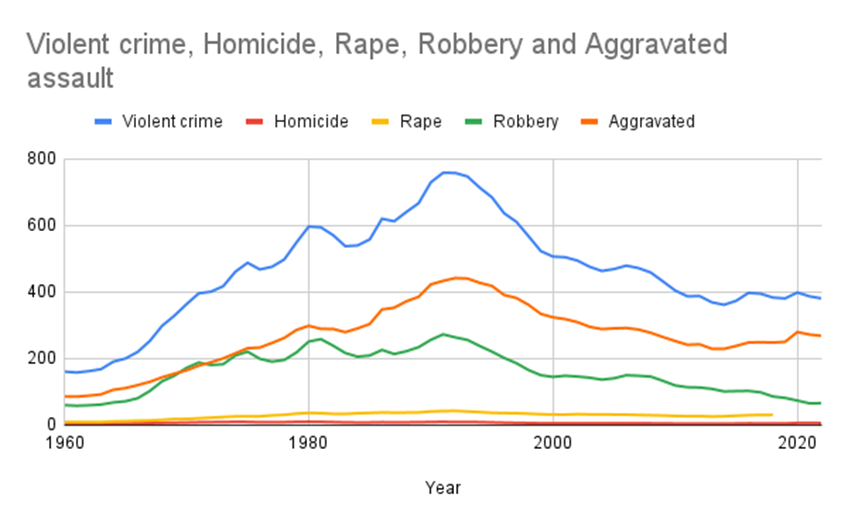

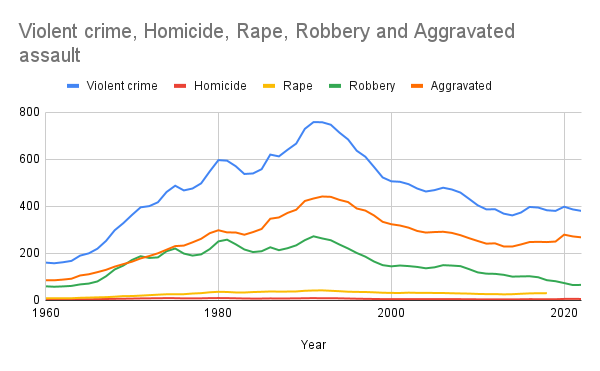

People who have reached adulthood in recent decades have been hit hard financiallyby this crime wave even if they have avoided becoming victims of direct violence. Violent crime in the United States has more than doubled since 1960, and the rate was three to four times the 1960 incidence for two decades in the 1980s and 1990s:

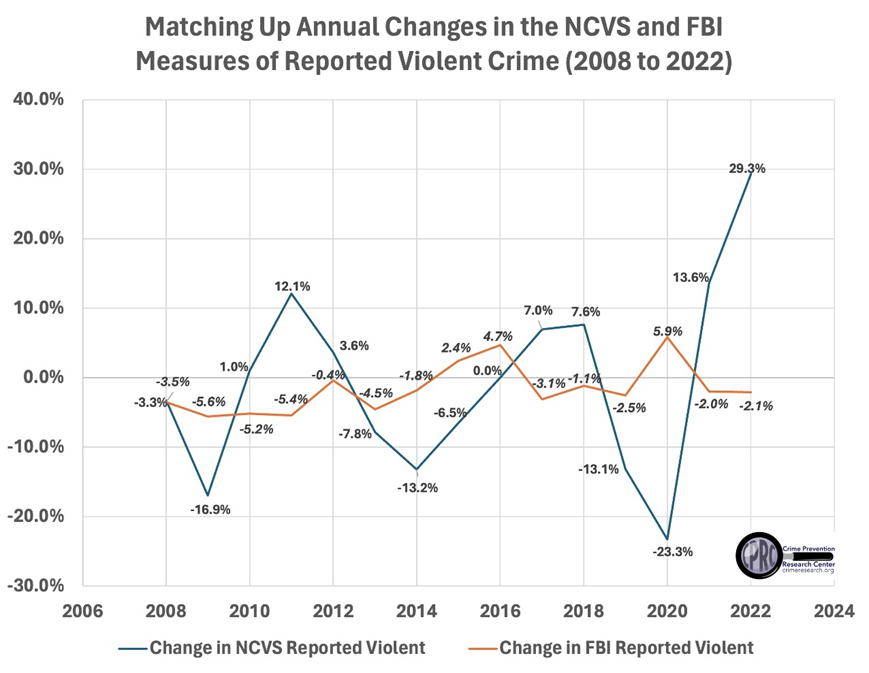

The much-ballyhooed recent decreases in murder rates in some cities barely made a dent in the overall trend for the twenty-first century. There is vastly more violent crime being reported now than when the baby boomers were reaching adulthood, and there is good reason to believe that the widely quoted FBI numbers have been increasingly undercounted for at least two decades, as John Lott and his team at the Crime Prevention Research Center have documented:

Cutting urban crime can reduce housing costs considerably, writes Robert Weissberg at American Thinker:

Consider how reducing crime facilitates affordable housing, and this benefit arrives without any new buildings, subsidies, or government-mandated affordable housing. Imagine crime eliminated in many currently crime-ridden, unlivable areas of the city. This includes all street crime plus “quality of life” crime—open-air drug markets, homeless encampments, vagrants in parks, loitering street gangs, plus public nuisances such as excessive noise, public intoxication, and graffiti that undermine civility. Further imagine the city granting landlords full power to operate their buildings—for example, making it easier to evict troublesome tenants.

With crime sharply reduced and landlords empowered, once uninviting neighborhoods will attract real estate developers who will buy up thousands of cheap, structurally sound but dilapidated buildings; refurbish them; and thus increase the city’s housing supply. With this expanded supply, prices would fall. Moreover, new residents will encourage local businesses and conceivably provide convenient jobs for recent arrivals. In an instant, the “greedy” developer—not commissars—becomes the creator of much needed affordable housing.

Moreover, with crime down, real estate developers can now build less expensive apartment buildings since they no longer must include anti-crime measures such as 24/7 doormen, off-street parking, and security systems. Even buildings lacking these anti-crime amenities will now be more desirable. Again, greater supply enhances affordability.

Crime reduction also increases overall wealth by freeing up resources for better uses, as New York City Mayor Rudy Guiliani demonstrated in the mid-1990s through the year 2000. Weissberg writes,

Reduced crime would fuel an overall economic boom via increased tourism and greater utilization of now unrented offices and retail space, and residents would feel sufficiently safe to attend night clubs and late-night sporting events. Corporations could now attract workers who previously avoided the city due to its high rents and crime. New Yorkers would return to local shopping now that merchandise is not locked behind Plexiglas, while now-vacant stores would be re-occupied.

While earlier generations of Americans moved to the suburbs to escape the rising crime and disorder, those who have entered adulthood since the early 1960s have had less freedom to do so, given that young people’s incomes are lower than those of older workers. They have had to take what they could get. In the race for better economic prospects to allow them to escape the risng danger and disorder, young people have pursued higher education in much-greater numbers, which involves putting off marriage and family.

The Census paper states that “increasing levels of college enrollment” have resulted in “contemporary cohorts spending a longer portion of their young adult lives enrolled in higher education, potentially delaying other markers of adulthood such as entering the labor force or marriage.” On top of that, young people emerge from those educational institutions burdened with tens of thousands of dollars in student debt, further undermining their economic security and their ability to pay for housing.

All those factors and others are forcing America’s young people to work very hard if they want to navigate the contemporary economy. Young people are delaying marriage and family formation for economic reasons. Fixing the nation’s housing market and reducing crime would be a boon for America’s young people and is clearly an urgent matter for redress.

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Poor, Poor Pitiful UBI Performance

Universal Basic Income (UBI) payments do not improve recipients’ lives, a proponent of such plans has reluctantly concluded with laudable honesty. Gold-standard studies show that UBI does not work, writes Kelsey Piper at The Argument:

Just give people money. It’s the simple, brute-force solution to so many problems. In low-income countries, charities are sometimes measured against whether their interventions are better than simply giving people cash. Even in high-income countries like the U.S., when disaster strikes, often the best thing you can do is get money into the hands of affected people immediately. They know whether they should use it to buy gas, rent an Airbnb or fly to their cousin’s house one state over.

So it wasn’t that crazy to assume—particularly once promising pilots were released—that the same should be true for addressing chronic poverty in high-income countries. If you give a new mom a few hundred dollars a month or a homeless man one thousand dollars a month, that’s gotta show up in the data, right?

Although it “wasn’t that crazy to assume” that money makes people better off regardless of how it is obtained, it is untrue, Piper writes:

Alas.

A few years back we got really serious about studying cash transfers, and rigorous research began in cities all across America. Some programs targeted the homeless, some new mothers and some families living beneath the poverty line. The goal was to figure out whether sizable monthly payments help people lead better lives, get better educations and jobs, care more for their children and achieve better health outcomes.

Many of the studies are still ongoing, but, at this point, the results aren’t “uncertain.” They’re pretty consistent and very weird. Multiple large, high-quality randomized studies are finding that guaranteed income transfers do not appear to produce sustained improvements in mental health, stress levels, physical health, child development outcomes or employment. Treated participants do work a little less, but shockingly, this doesn’t correspond with either lower stress levels or higher overall reported life satisfaction.

Homeless people, new mothers and low-income Americans all over the country received thousands of dollars. And it’s practically invisible in the data. On so many important metrics, these people are statistically indistinguishable from those who did not receive this aid.

Piper recounts gold-standard (randomized controlled trial) studies that consistently and uniformly show the extra money has little to no effect on the recipients’ overall well-being even though they are not “blowing it all on ‘vices’ like gambling, tobacco or alcohol.” The payments do not improve “their health, not their sleep, not their jobs, not their education, and not even time spent with their children,” Piper writes. “They did experience a reduction in stress at the start of the study, but it quickly went away.”

The studies are comprehensive, accurate, and true, Piper writes:

I cannot stress how shocking I find this and I want to be clear that this is not “we got some weak counterevidence.” These are careful, well-conducted studies. They are large enough to rule out even small positive effects and they are all very similar. This is an amount of evidence that in almost any other context we’d consider definitive. And yet, you’d be hard-pressed to hear about it in the media.”

The American press consistently mislead the public about this research, as do the authors of less-reliable studies, through “death by a thousand press releases,” Piper notes:

The depressing facts I’ve recounted for you are largely missing, obscured or glossed over in the public communications about these studies. Articles focus on tiny positives or, at best, will note the evidence is uncertain. Very few articles or press releases put the big picture together even if they cover one disappointing result.

Perhaps the most egregious offender is the Denver Basic Income Project—the most bizarre set of findings I reviewed. This is what a prominent part of the report section of their website looks like:

“All payment groups showed significant improvements in housing outcomes, including a remarkable increase in home rent and ownership, and decrease in nights spent unsheltered.”

I guess I can’t call this a lie per se, but in reality they gave $1,000 a month to homeless people and they were barely more likely than the control group to get housing.

The American press has been mendacious in covering this issue, consistently concealing the failure of studies to indicate that UBI works. Piper writes,

It’s not just the researchers’ fault. Even when researchers don’t understate a null or negative result, they told me that journalists are often less eager to go to press with it. “[Researchers have] written a dozen null effect papers, they’re trying to get the result out there,” [study author Sarah] Miller told me. “People aren’t interested in reading [them].”

Piper rightly laments this mass denial of reality in which “widespread agreement on basic facts is scarce and noble lies have permeated the halls of truth-seeking organizations like the media.” (The media are not “truth-seeking organizations,” unfortunately.) Piper’s solution is to let the truth come out, whatever it is, and act accordingly. That is the position of a real scientist, policy analyst, policymaker, or decent human being.

During COVID, power‑mad government officials around the globe shut down society to protect us from a contagious virus that killed a small percentage of those who got it. Restaurants, parks, and beaches were closed. Gatherings larger than what could fit in a phone booth were canceled. They even told us not to celebrate Thanksgiving with our loved ones for “the greater good.”

Today, power‑grabbers in Canada are banning hikers from the woods in the Maritimes and imposing enormous fines on those who dare set foot in their own public forests. Why? Because of the Canadian wildfires. And this kind of madness is just the beginning.

Contact Us

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org

{kind=link}