Authored by George Ford Smith via the Mises Institute,

Artificial intelligence is rapidly becoming one of the most capital-intensive industries in history. Consider: Semiconductor fabrication plants cost tens of billions of dollars. Massive data centers consume extraordinary amounts of electricity, sending power bills soaring. Specialized engineering talent commands premium wages. (Although the median salary for an AI professional is $160K annually, the top 1 percent of AI researchers receive compensation packages exceeding $1 million). Global supply chains must coordinate rare materials, precision manufacturing, and complex infrastructure.

Yet discussions about artificial intelligence almost never address the most important economic variable shaping its development: money.

From an Austrian perspective, the future of artificial intelligence ties directly to the monetary system that finances it. Whether AI produces sustainable prosperity or another boom-bust cycle depends less on algorithms than on interest rates.

As we’ve seen throughout history, interest rates in a fractional-reserve banking system trend ever lower when a new technology gets underway. This generates the illusion of prosperity called a boom, followed inevitably by a bust.

As a reminder of what is meant by a “bust,” keep in mind the figure $16.2 trillion—“The total net worth American households lost between 2007 and 2009 of the Great Recession.”

Artificial intelligence is best understood economically as a higher-order capital good—a tool that enhances the productivity of human performance. Like machinery during the Industrial Revolution or computers in the late twentieth century, AI operates within a time-structured production process involving multiple stages before consumer goods emerge. Here’s how ChatGPT works as a consumer good, for example, providing an indispensable research tool for millions.

Nobel laureate F.A. Hayek emphasized that production requires coordination of dispersed knowledge across time. Interest rates serve as the critical signal aligning savings with investment. When that signal is distorted, the capital structure becomes misaligned.

Artificial intelligence offers super-advanced intellectual performance, but as a capital good is still subject to interest rate signals. Economically, under our central bank fiat system, distorted interest rates intensifies capital misalignment.

The Neglected Relevance of the Monetary System

The current AI boom is unfolding after more than a decade of unprecedented monetary expansion. Following the 2008 financial crisis—and again after 2020—the Federal Reserve expanded its balance sheet dramatically while maintaining near-zero interest rates for extended periods. The Fed has been unwinding since its April 2022 peak, but is still 59 percent above pre-pandemic levels.

In the world of Federal Reserve economics, cheap credit is a necessary fuel for economic development. But as Mises warned,

What induces an entrepreneur to embark upon definite projects is neither high prices nor low prices as such, but a discrepancy between the costs of production, inclusive of interest on the capital required, and the anticipated prices of the products. A lowering of the gross market rate of interest as brought about by credit expansion always has the effect of making some projects appear profitable which did not appear so before. (emphasis added)

When the Fed artificially suppresses interest rates, entrepreneurs undertake projects that appear profitable but cannot be sustained once monetary conditions change. This is the core of Austrian business cycle theory: Credit expansion causes malinvestment.

Artificial intelligence investment is particularly vulnerable to this dynamic because it involves long time horizons, uncertain demand, and enormous upfront capital requirements.

Warning Signs of Malinvestment

Several familiar signals are already visible:

Technological revolutions often coincide with speculative manias. The railroad booms of the nineteenth century, the stock market excesses of the 1920s, the dot-com bubble of the 1990s, and the housing boom before 2008 all followed this pattern. In each case, the technology survived, while the speculative capital structure collapsed. Artificial intelligence may follow a similar trajectory if monetary conditions continue to distort investment signals. As long as money is under monopoly control of political appointees instead of the free market, distortion is guaranteed.

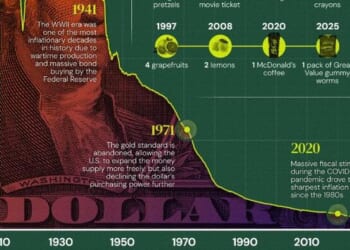

Gold historically constrained credit expansion because banks could not create unlimited claims without risking the wrath of defrauded depositors. Interest rates reflected real savings more accurately, and investment discipline was stronger.

Under a monetary system anchored by market forces rather than quarreling politicians, artificial intelligence would develop in a manner more closely aligned with genuine demand and less vulnerable to speculative collapse.

Conclusion

Artificial intelligence is likely to become the most transformative technology in history, but under the auspices of a money-printing counterfeiter such as the Federal Reserve it’s certain to create massive economic problems. The real threat is artificial credit, not artificial intelligence.

People rightfully fear losing their jobs. What actually threatens workers, though, is not automation but monetary distortion. When credit expansion drives speculative booms, capital is misdirected into unsustainable ventures. When the correction arrives, workers suffer the consequences of decisions made far above them. And they tend to direct their anger at the market, rather than the politically-influenced decision makers.

Ron Paul was right. We need to end the Fed and end the property rights violations of fractional reserve banking.

Loading recommendations…