“Yes, it’s true there are extensive foreign ties, and I think it would be a very valid step to take,” said Miller.

The designation is significant because of the much greater latitude it gives the federal government in countering a designated terror organization. “An FTO designation effectively functions as a ban by making it unlawful for any person in the United States to knowingly provide “material support or resources” to the entity concerned, The Raw Story reports.

“This network of Antifa is just as sophisticated as MS-13, as TDA, as ISIS, as Hezbollah, as Hamas, as all of them,” said Homeland Security Secretary Kristi Noem early in the meeting. “They are just as dangerous. They have an agenda to destroy us, just like the other terrorists we’ve dealt with for many, many years.”

An associate of former vice president Mike Pence quickly suggested that the Trump administration might use massive, indiscriminate military force in countering Antifa, the Raw Story article states:

Olivia Troye, who was counterterrorism advisor to Vice President Mike Pence in the first Trump administration, raised the question of whether the administration is signaling a willingness to use lethal force against individuals deemed to be “antifa.”

“I guess the question is, are we just going to start bombing random buildings where they think antifa is residing?” Troye said on Thursday, on the podcast The Left Hook with Wajahat Ali, after the host observed that the U.S. military has recently carried out strikes against alleged drug boats in the Caribbean.

“I know that sounds hyperbolic,” Troye said, “but what does that mean when Pam Bondi says that?”

In that same podcast, Trump first-term Department of Homeland Security Chief of Staff Miles Taylor echoed that panic by claiming that Trump and Defense Secretary Pete Hegseth are training the U.S. military for invasions on American soil, the Raw Story article reports:

“We’re not talking about loosening the rules of engagement to go after Taliban fighters,” Taylor said. “We’re talking about loosening the rules of engagement to go after the domestic opposition. This is not hyperbole.”

At MSNBC, commentator Paul Waldman repeated the hoary claim that Antifa is a fairy tale: “‘Antifa’ is not a network, or a collective, or a syndicate,” said Waldman. Waldman continued in that vein:

It is essentially an idea, one that begins in a place all Americans should support, but unfortunately don’t: opposition to fascism. Then there are a tiny number of (mostly young) people who take antifa to a different place—people who like to go to public gatherings of far-right groups and get into street fights. If a video of someone punching a white nationalist comes up on your social media feed, the one doing the punching probably calls themself antifa.

There being no such thing as Antifa, the White House effort is merely … a pretext for fascist oppression of all political opponents, Waldman writes:

For all the buffoonery on display, the Trump administration is doing something sinister. Shortly after Trump issued an executive order declaring antifa a domestic terror organization, the White House issued a “national security presidential memorandum” on “Countering Domestic Terrorism and Organized Political Violence.” According to the memo, “common threads animating this violent conduct include anti-Americanism, anti-capitalism, and anti-Christianity; support for the overthrow of the United States Government; extremism on migration, race, and gender; and hostility towards those who hold traditional American views on family, religion, and morality.”

These remarkably broad terms make it quite clear that the administration sees the war on antifa, at least in part, as a way to designate its political opponents as adjuncts to terrorism, then target them for official harassment. In other words, the war on antifa can, quite easily, become the justification for further steps toward actual fascism. But if you say that, you’re probably antifa.

Trump’s use of the term “violent conduct” in the memorandum certainly suggests that the government does not intend to attack people merely for thinking things. It is not a “broad term” at all, much less “remarkably” so.

In the White House meeting, Trump and his cabinet members emphasized their intent to go directly after foreign organizations that supply money, organizational activities, training, weapons, and other resources to Antifa. Federal law allows this under the foreign terror designation, the Raw Story article acknowledges:

The federal statute defines “material support and resources” to include “any property, tangible or intangible, or service, including currency or monetary instruments or financial securities, financial services, lodging, training, expert advice or assistance, safehouses, false documentation or identification, communications equipment, facilities, weapons, lethal substances, explosives, personnel… and transportation.”

Designation of Antifa as a foreign terrorist organization would enable the federal government to root out all the people and organizations that support it and dismantle its entire network of sponsorship and collaboration, said Attorney General Pam Bondi at the meeting:

“We’re not going to stop at just arresting the violent criminals we can see in the streets,” Bondi said. “Fighting crime is more than just getting the bad guy off the street. It’s breaking down the organization brick by brick. Just like we did with cartels. We’re going to take this same approach, President Trump, with Antifa: destroy the entire organization from top to bottom. We’re going to take them apart.”

Even before Trump announced he would further increase the federal government’s efforts against Antifa via the new designation, Portland, Oregon-based Rose City Antifa founder Johan Victorin was seen on camera in his new home base of Vaberg, Sweden on October 6, and State University of New Jersey professor Mark Bray announced to his students that he was relocating to Spain, The Epoch Times reports.

Bray is the author of Antifa: The Antifascist Handbook and has openly endorsed lawbreaking in furthering the organization’s goals. “Only mass antifascism, legal or not, can save us,” Bray wrote on the Bluesky social media platform on Oct. 4, the story notes.

In addition, Antifa funder Antifa International “shut down its operations in the United States out of concern about engaging in prohibited activity,” The Epoch Times reports in the same story. “‘As a precaution, we have shut down the donation infrastructure for The International Anti-Fascist Defense Fund to protect our donors and recipients,’ the organization wrote on its website.”

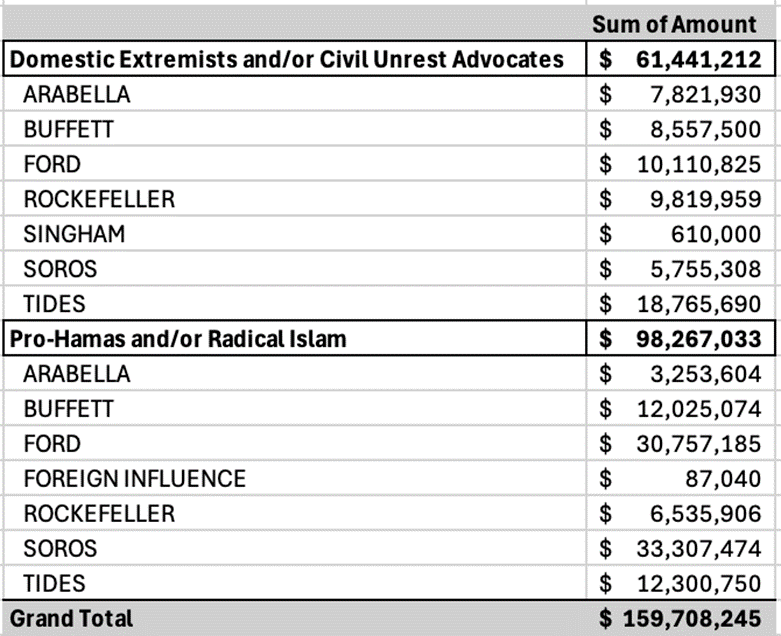

A very large Antifa funder remains intact though technically shut down at present: the U.S. government. At the Wednesday White House meeting, Seamus Bruner, director of research for the Government Accountability Institute (GAI), “briefed the president and his cabinet on a complex network of dark-money NGOs and activist groups fueling unrest nationwide via the permanent protest-industrial complex,” a large amount of it through American taxpayer money “laundered by Democrats,” “Wall Street Apes” tweeted, ZeroHedge reports:

“We have identified dozens of radical organizations, not just the decentralized Antifa organizations, but dozens of radical organizations that have received more than $100 million from the Riot Inc investors,” Bruner told Trump.

Elon Musk chimed in on X, commenting on a video featuring Bruner’s public briefing to the president about the dark-money NGOs, saying, “Way more than $100M of US taxpayer money.”

GAI President Peter Schweizer affirmed Musk’s assertion that same day, tweeting, “@elonmusk is RIGHT! @seamusbruner and our team is still following the money and the numbers keep getting bigger. SHUT IT DOWN!”

The very different reactions to the Trump administration’s anti-Antifa effort are both entirely predictable and worthy of consideration. Government action against groups known for violence, arson, trespassing, intimidation, illegal occupation of others’ property, blocking of public rights of way, and other such crimes must be conducted with a respect for the rights of the accused. A government’s essential responsibility, however, is the protection of people’s life, liberty, and property. There is plenty of room for action within those boundaries.

The Trump administration’s stated intentions do not indicate an excessive response to the rise of Antifa and its apparent network of support from foreign nations. The administration’s opponents will reflexively oppose the effort and attempt to convince the public that it is an overreaction, as is their right. It is important for the political right to be careful in supporting federal police operations such as this, endorsing only actions that truly defend the American people’s life, liberty, and property while ensuring respect for the rights of the accused.

That it is a difficult line to define, and opinions will differ. It is nonetheless essential to be clear on what the goal is and what means of achieving it are legal and just.

Are Democrat-led cities spiraling out of control? Weeks of unrest, weak law enforcement, and rising violence are testing the limits of left-wing policies.

In Portland, ANTIFA attacks ICE facilities by night while petty crime dominates by day. In Chicago, local leaders defend policies that fuel gang violence and lawlessness. As the Trump administration vows to crack down, the question is — how far should it go?Plus: President Trump threatens Hollywood with tariffs on movies filmed overseas, and in UNHINGED, we reveal shocking text messages from a Democrat AG candidate showing violent hatred toward a GOP legislator.

Join Linnea Lueken, Jim Lakely, S. T. Karnick, and Chris Talgo for a fiery discussion on all this and more in Episode #514 of the In the Tank Podcast.

Federal Housing Policy Holds Back Home Ownership

I’ve noted in recent issues of this newsletter that millennials are correct in thinking they have more difficulty in achieving the American Dream than previous generations, particularly in terms of buying a home—which is of course central to that ideal.

There are multiple reasons for the difficulties facing first-time home buyers today, several of which I discussed in Life, Liberty, Property issue number 114. Writing in The Wall Street Journal, Southwest Public Policy Institute President Patrick M. Brenner identifies another major impediment to homeownership: 30-year mortgages. Brenner writes,

Millennials reached the 50% homeownership milestone later than any previous generation, burdened by record-high housing costs, elevated mortgage rates, and struggles with down payments. Nearly a quarter say they expect to rent forever.

But the obstacle is more than prices or supply: It’s an insidious financial instrument so predatory and deceptive that it has warped the housing market for nearly a century. Ladies and gentlemen, I present the 30-year mortgage.

The federal government pushed the public and the nation’s banking system into longer mortgages during the Great Depression, starting in 1933, through loan guarantees, subsidies, regulation, and other market manipulation, to increase people’s ability to buy houses.

Before the government stepped in, nearly all American mortgages were for only three to five year terms, in which the borrower would pay interest only, with the principle due in a big balloon payment at the end of the term. Buyers would typically take out another mortgage at that time, essentially renting a house in five-year increments.

The new system included Fannie Mae and, starting in 1970, Freddie Mac purchasing mortgages and thus guaranteeing their value to lenders. That gave banks much greater incentives to lend to home buyers, while making the loans more affordable for the buyers.

The banks got a far better deal out of this than the home buyers did (surprise, surprise!). Brenner writes,

But the change came at a steep price: The 30-year mortgage locked families into a lifetime of interest payments that cost the borrower far more than the original price.

Today someone who buys a $400,000 property at 6% interest effectively pays for the home almost twice. By the end of the loan, a family can expect to pay more than $690,000 in principal and interest, assuming a 20% down payment. The problem isn’t interest rates or housing costs—it’s the loan itself. Lower down payments make entry to the market easier, but the borrower pays dearly for that privilege. An FHA loan on that same house with its minimum down payment of only 3.5% means the borrower eventually shells out $833,000. Inflation may erode some of the burden but can’t keep up with the scale of interest charges.

Of course, making houses more-immediately affordable greatly increases the number of people interested in buying them, and this higher demand raises prices (even as builders work to increase the supply as quickly as they can). Brenner writes,

As this model grew across the 20th century, it dramatically raised base housing prices relative to income. Postwar programs such as the GI Bill turbocharged the mortgage model. Easy credit powered an artificial demand boom, which, over time, inflated home prices. When buyers had to pay cash, sellers were constrained by what households could actually afford. But when banks are dangling decades of borrowed money, buyers bid higher, sellers raise prices, and lenders pocket the spread.

Lenders and the federal government engaged in multiple schemes starting in the 1970s to keep the game going, which led to the financial crisis of 2007 and Great Recession in 2008. The millennials were beginning to enter the workforce at this time and were hit by low employment demand (and thus suppressed compensation) and high housing costs, which continued to rise rapidly with the government’s “encouragement” of homeownership (which was simply ham-handed intrusion into the housing market). Millennials got the worst of it, Brenner writes:

Which leaves millennials struggling to afford a home of any kind. Gone are the 1970s, when an average home could be secured for about $26,300 against an annual household income of $9,870. Today’s latest data shows that the annual household income is $83,730 and the average home costs $410,800.

A particularly damaging government action was the 1968 Truth in Lending Act, which allowed lenders to emphasize a loan’s annual percentage rate, or APR. The APR highlights a benign number, say, 5 percent per year, while diverting the borrower’s attention from the magic of compound interest, which in this case is very dark witchcraft. Brenner writes,

Todd Zywicki, in his work on mortgage law and economics, notes that APR hides the cumulative cost and distorts borrower behavior. Families anchor on the “rate” without understanding how compound interest quietly siphons away their wealth. This further inflates prices.

This is the same process by which recent generations of Americans got snookered into pouring money into greedy hedge funds masquerading as colleges and universities, Brenner notes:

We’ve seen this dynamic before. In higher education, government-backed loans artificially inflated tuition, saddling students with generational debt. The mechanism is the same with housing: Subsidized credit raises prices.

The federal government’s promotion of homeownership has consistently benefited everyone involved—except buyers of homes. The fact that regulation of the nation’s entire housing market has obviously been captured by the banking industry ought to be a national scandal. “Like every centrally planned system, the [30-year] mortgage distorts markets, inflates prices, and serves institutions rather than individuals,” Brenner writes.

The lesson in this doleful history is that there are no short cuts to wealth—unless you can get the government to use force and/or fraud to manipulate people into forking it over to you. That describes what is now nearly a century of federal government “improvement” of housing finance.

Brenner’s short article is an excellent analysis of this nearly century-long outrage and the enormous damage government does in a central area of life. His conclusion is incontestable:

The mortgage isn’t the foundation of the American Dream. It’s the scam of the century: a loan so exploitative it required a federal law to disguise its true nature. For generations, lenders, regulators and politicians have normalized a system that drains family wealth under the guise of opportunity. Until Americans demand honesty, the scam will continue—and homeownership will remain a dream sold on indebted servitude.

Colossal government manipulation of the housing market to benefit lenders and deceive borrowers is certainly not the American Dream. It is in fact emblematic of what has been killing the American Dream.

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Contact Us

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org