We’d appreciate your input on a few questions about environmental and energy policy. This brief survey should only take one minute to complete.

Your responses will help us better understand different perspectives on these important issues. All responses are confidential.

Welcome to Dispatch Energy! Venezuelan President Nicolás Maduro is currently sitting in custody in New York, indicted on numerous narco-terrorism, drug, and gun charges. The dictator was captured along with his wife in a raid by U.S. forces over the weekend. President Donald Trump then announced that Washington was “in charge” of Venezuela and its vast oil reserves and boasted of ambitious plans to have American companies revitalize the dilapidated industry. Even more tangibly, Trump has proclaimed that 30 million to 50 million barrels of sanctioned Venezuelan oil will be sold to the U.S. at market price, and Energy Secretary Chris Wright has announced that “indefinitely, going forward, we will sell the production that comes out of Venezuela.”

What this historic development means for Venezuela—or for the United States, for that matter—remains a wide-open question. The volume of Venezuelan oil that could reasonably hit U.S. shores over the coming weeks, months, and years will depend largely on 1) the stability of new leadership in Caracas, 2) the future of the current U.S. blockade, 3) the status of U.S. sanctions, and 4) the durable policy environment in Venezuela going forward.

Let’s review what we know about this evolving situation.

Caracas Context

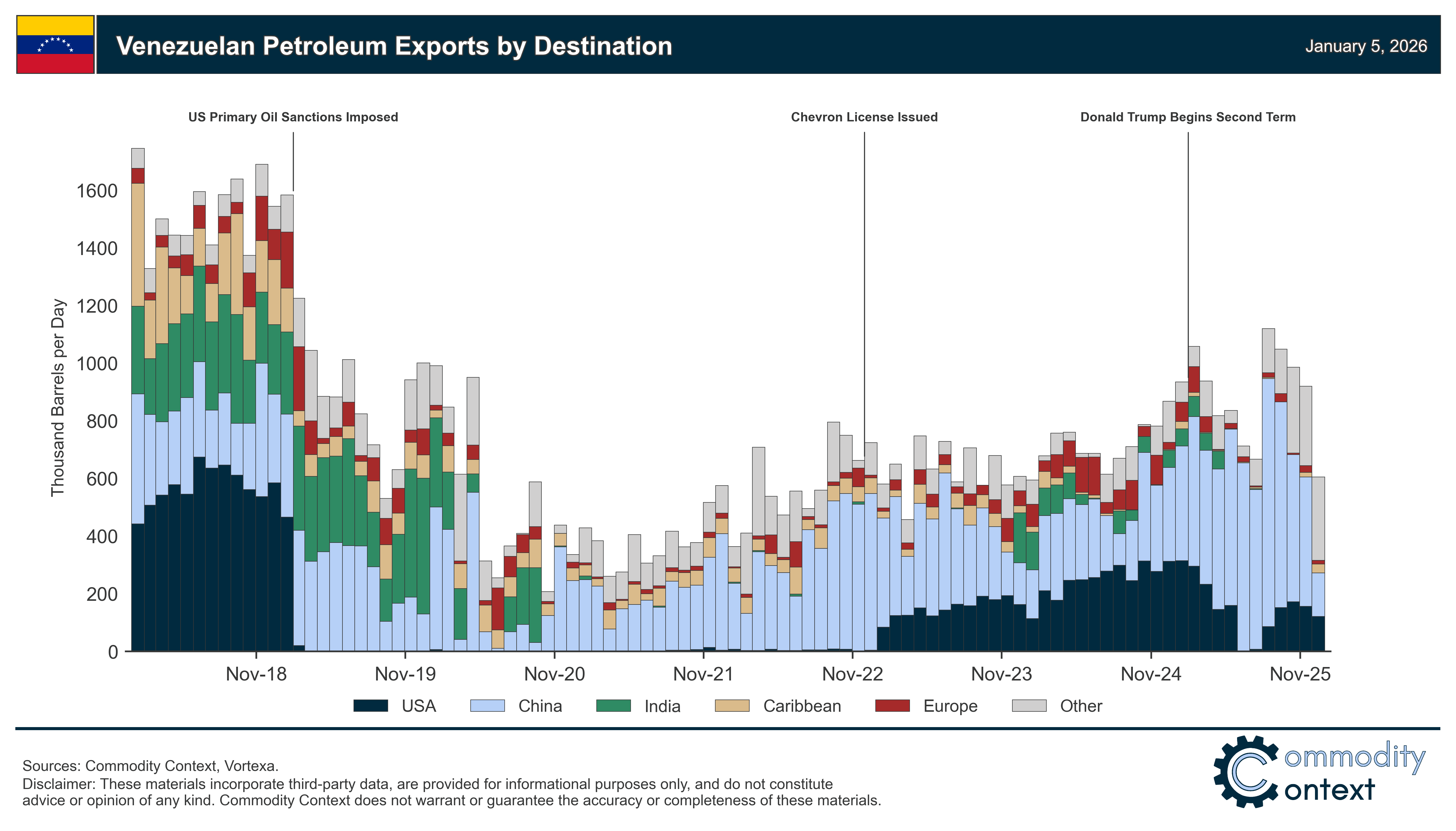

As you may have heard, Venezuela holds the largest oil reserves in the world. The South American country reports having more than 300 billion barrels in its proven reserve base, larger than the in-ground reserves claimed by OPEC kingpin Saudi Arabia. While there are debates about the ultimate size, no one disputes that Venezuela holds substantial crude oil resources. Despite this massive potential, Venezuela today produces a relatively paltry 900,000 barrels per day (bpd), which is more on par with minor OPEC+ members like Oman than the group’s heavyweights. In fact, Venezuelan oil production has fallen from roughly 2.4 million bpd in 2015, from all-time highs of more than 3.7 million bpd in 1970, and from a slightly lower—but more immediately relevant—peak of 3.4 million bpd in the late 1990s. The founding OPEC member continues to produce significantly below its potential due to severely incompetent governance—not to mention rampant corruption—combined with a healthy dollop of U.S. sanctions.

U.S. sanctions have been volatile over recent years. Trump imposed harsh sanctions on the Venezuelan national oil company PDVSA during his first term in early 2019, sinking Venezuelan petroleum exports from around 1.5 million bpd to a low of around 200,000 bpd in early 2020, according to tanker tracking data from Vortexa. Production and exports began to climb gradually again during the Biden administration, thanks in part to the issuance of sanctions exemption licenses, or waivers, in an effort to get Maduro to agree to freer and fairer presidential elections in 2024 (spoiler: It didn’t work). Exports grew to more than 1 million bpd before Trump entered office in early 2025, but production growth then stalled out upon his return. The new administration then canceled sanctions waivers for all oil and gas companies except Chevron, which saw tighter terms. While the move stunted Venezuelan production growth, it didn’t crush export volumes, which instead largely rerouted to China, the world’s sanctioned barrel buyer of last resort.

In the final months of 2025, Trump looked to military action to build pressure on Maduro. The Trump administration has undertaken a major U.S. naval buildup off Venezuela’s coast, imposed a blockade on the export of Venezuelan crude shipped on sanctioned tankers, and even went so far as to seize four tankers—two before Maduro’s capture, two after—and counting. The blockade had a serious bite: Crude exports stood at less than 600,000 bpd on average in December, down about 40 percent from November levels, and have declined further since. Upstream production has been similarly throttled, by about 15 percent in December, as export offtake was halted and wells were forced to shut for lack of sufficient storage space to stash the overflowing barrels.

Near-Term Supply Solutions

The most immediate question is whether Maduro’s successor will be able to hold the current government together. The Constitutional Chamber of Venezuela’s Supreme Court has ordered that Vice President (and Oil Minister) Delcy Rodríguez “assume the role of acting president,” which isn’t exactly regime change—the regime simply auto-promoted the next in line. At minimum, the immediate risk to the oil industry is that Venezuela’s exports remain paralyzed by this shakeup of the country’s leadership. Worse, a failed transition of power could lead to the outbreak of open hostilities between various competing factions that Maduro had been holding together. A decree from the new acting government ordered police to “immediately begin the national search and capture of everyone involved in the promotion or support for the armed attack by the United States.” Yet, despite this response from Caracas, Trump has signaled that he is willing to work with Rodríguez if she meets Washington’s demands.

The next question is what action, if any, the U.S. will take to remove its blockade and increase the flow of Venezuelan oil. The U.S. blockade was initially imposed to build pressure on Maduro, and the U.S. now has Maduro in custody. But Trump has indicated plans to keep the blockade in place as a means of forcing compliance from the Rodríguez government: “The American armada remains poised in position, and the United States retains all military options until United States demands have been fully met and fully satisfied.” While those demands have been loose and still evolving, a few key themes have emerged: Venezuela needs to 1) “kick out” operatives from countries hostile to the U.S. (namely China, Russia, Iran, and Cuba), 2) partner exclusively with U.S. companies on production, and 3) favor the U.S. when selling its crude.

Any U.S. reversal of the embargo will have ripple effects across the global oil industry. Indeed, the Venezuelan blockade was one of several key factors keeping prices higher over the past month. So, any loosening of the U.S.-imposed “quarantine” would increase Venezuelan supply—and thus put downward pressure on global prices. However, as things technically stand, the restored flow of Venezuelan barrels would largely go to China—not the U.S.—given American sanctions on Venezuelan oil and the fact that China is the only real buyer of sanctioned barrels. There has been some movement on “selectively rolling back sanctions to enable the transport and sale of Venezuelan crude and oil products to global markets” based on recent comments from the Department of Energy, but the timing and terms of the possible rollback remain unclear.

The medium-term question is what that sanctions relief will look like. U.S. sanctions were forcing the majority of Venezuelan crude to make the long journey to China rather than to the U.S. Gulf Coast. With the exception of the roughly 150,000 bpd of Chevron joint-venture flow, Venezuelan crude could not and will not reach the nearby Gulf Coast refinery hub until these sanctions are repealed or additional waivers are issued to exempt participants (as we saw during the Biden years). Only then will Venezuelan barrels again land at U.S. refineries and more freely compete with other heavy sour grade crudes, including Western Canadian Select and Mexican Maya.

In this scenario, we could expect a modest few dollars per barrel widening of regional heavy crude differentials. But bear in mind that any reduction in demand for non-Venezuelan heavy barrels from refineries in the U.S. Gulf would reduce their cost and, thus, increase their attractiveness to other buyers further afield. It’s also important to note that, prior to Trump’s imposition of heavier sanctions on PDVSA in early 2019, only roughly one-third of Venezuelan crude exports were going to the U.S. So there’s no reason to think that all of Venezuela’s exports, if they recover and are released from sanctions, will flow to U.S. shores unless forced to by some non-market mechanisms (such as a deal between Washington and Caracas to prevent shipments to China or induce preferential lower prices for American buyers).

Long-Term Growth Realities

The long-term question is whether Trump can use this catalyst to meaningfully influence a turnaround of Venezuela’s oil industry. Venezuela can clearly produce much, much more oil—easily 2 million to 2.5 million bpd over the next five-plus years, en route to more—with freer, unsanctioned access to global markets and a flood of inbound investment. But decades of underinvestment and resulting loss of operational expertise have rotted the physical infrastructure that underpins the Venezuelan oil industry. And American oil companies are broadly wary of investing tens of billions of dollars in a country in a state of acute political uncertainty, especially given that many of these companies have operated in Venezuela before and had their assets expropriated.

In the best-case scenario, the revitalization of Venezuela’s oil industry back to where it stood a decade ago, let alone the state of the late-1990s, would require between $50 billion and $100 billion in upstream and supporting infrastructure investment—and the better part of a decade. In 2021, an official PDVSA document put the cost of restoring output to a higher threshold of the late-1990s levels (i.e., more than 3 million bpd) at $58 billion. Today, that figure feels charitable given more impartial estimates as well as the propensity of these projects to run vastly over budget in the best of circumstances—which, again, these are not. Consultancies like Rystad have put the required investment at more than $100 billion. In addition, there’s another $10 billion to $20 billion needed for associated pipeline, storage, and shipping infrastructure—and still more for Venezuela’s blackout-prone electrical grid to get refineries back in proper working order. (For more on the immensely degraded state of Venezuela’s oil industry, see some of the visuals in this piece by the Financial Times.) Essentially the only good news is that all of Venezuela’s major producing regions are either onshore (like the Orinoco Belt) or in shallow water (like Lake Maracaibo), which creates a far lower barrier to entry than the deepwater projects in Guyana and Brazil.

Moreover, it’s not going to be easy to find that investment appetite among American oil companies. Following the expropriation drive of the 2000s, Chevron worked out a deal with the then-Chávez government—involving increased cooperation with PDVSA—to remain in the country. Others, like ExxonMobil and ConocoPhillips, are still owed substantial sums. In the case of ConocoPhillips, an international arbitration tribunal in 2019 “unanimously ordered the government of Venezuela to pay the company $8.7 billion in compensation for the government’s unlawful expropriation of ConocoPhillips’ investments in Venezuela in 2007, plus interest,” and Reuters has more recently put the total sum the company is seeking at around $12 billion. There are reports that the Trump administration has been stressing to oil industry executives that to see a dime of money owed to them by Caracas, they should be ready to invest large amounts of capital in Venezuela’s oil industry. But, at a moment of acute political uncertainty, few companies are likely willing to jump headfirst back into Venezuelan oil. Indeed, these companies reportedly want “serious guarantees” from the Trump administration before they put anywhere near the required volume of capital to work in the acutely risky jurisdiction.

In Conclusion

Thus far, the oil market remains unsure what to make of Maduro’s capture. Prices initially slipped lower, briefly falling below $60 per barrel of Brent crude oil before rising again to end Monday roughly $1 per barrel higher, and have bounced around in the low $60s for the rest of the week. The next few days and weeks will remain uncertain, and the flow of news will almost certainly remain fast and furious, likely putting upward pressure on prices. But after that initial dust settles, most forward scenarios are likely to result in lower oil prices given the eventual easing of the U.S. blockade, which would allow Venezuelan supply back onto the global market, and reversal of U.S. sanctions, which would allow those barrels to more freely flow to refineries along the U.S. Gulf Coast.

Longer term, the outlook is broadly positive for Venezuelan oil production and, thus, negative for prices, all else equal.Crude output remains exceptionally low relative to the country’s potential, with decades of capital starvation now creating numerous opportunities for investment. However, it will take monumental investment from firms that have already been burned in Venezuela to regain the production capacity of even a decade ago, let alone the more than 3 million bpd last seen in the late ’90s. And many, many questions remain unanswered about what exactly it will look like if, as has been reported, the Trump administration really does plan to “control Venezuelan oil for years to come.”

Alabama family wins fight with Fish & Wildlife Service

Since 1902, the Skipper family has managed Alabama forestland with sustainability in mind. For 60 years, they even partnered with the state to open their land for public recreation and aid wildlife recovery.

But that relationship collapsed in February 2020, when federal officials designated over 10,000 acres of the family’s land as “critical habitat” based on a single snake sighting. With PLF’s help, the Skippers fought back—and won.

Stories We Think You’ll Like

Innovation Spotlight

- ExxonMobil has been pioneering a new “lightweight proppant technology” that is derived from petroleum coke. The Shale Revolution of the early 2000s was driven by a combination of horizontal drilling, which exposed far more of the thinner, flatter reserve, and hydraulic fracturing (i.e., fracking), which cracked open that source rock to help the trapped oil flow. Fracking uses sand as “proppant” to, quite literally, slip into fractured cracks to prevent them from closing again under the immense pressure. Historically, companies used specific types of sand as proppants. But now, ExxonMobil is increasingly using a proppant derived from petroleum coke, one of the heaviest residual elements naturally left over from the refining process. This petcoke-derived proppant, according to Exxon, “opens greater fracture areas than traditional sand” and “has improved our resource recovery by up to 15%.” The proppant “looks like black sand to the naked eye,” but actually improves recovery by flowing to areas that regular sand generally doesn’t. In doing so, petcoke-derived proppant has the potential to transform one of the least valuable products coming out of a refinery into a competitive advantage. This innovation helps shale patch producers increase their recovery factor, a productive boost with tremendous upside given how little of the oil in place is typically extracted from a given tight oil well.

Further Reading

- I host a podcast called Oil Ground Up and, in November, I hosted Venezuelan oil industry expert Francisco Monaldi for a timely discussion about Venezuela’s current production constraints and what it would take to turn the dilapidated industry around. The episode is a great primer for those seeking to learn the context behind still-evolving efforts by Trump to revitalize, or seize, Venezuela’s oil industry. For an even deeper dive, check out this 2020 report by Monaldi and his colleagues at Rice University, which provides granular detail on the historic looting and mismanagement of the South American country’s petroleum sector.

- Elsewhere in The Dispatch, be sure to read Alex Demas on the difficulties facing Trump as he seeks to bring American oil companies back to Venezuela. “Venezuela still operates under the same laws that forced American companies out nearly two decades ago, the country’s oil industry infrastructure has deteriorated to an unknown extent, and major oil companies remain wary of reentering a market where their assets were once seized without compensation,” he writes. “On top of that, the Trump administration has been largely silent, at least publicly, about its long-term plans for Venezuela, leaving the very investors it’s depending on to rebuild the country’s oil industry torn between the wishes of the White House and an uncertain reality in Caracas.”

{kind=link}