The attacks on upstream oil/gas assets across the Middle East this week sparked turmoil across global energy markets.

Israel set off the chain reaction with its attack on Iran’s South Pars gas field on Wednesday morning, followed by Iran’s retaliatory strikes on Qatar’s LNG plant, Saudi Arabia’s Red Sea export hub, and other targets across the surrounding Gulf states.

This week’s attacks on critical upstream energy facilities across the Middle East, by both Iran and Israel, suggest the risk of prolonged outages and tighter global gas markets.

Read:

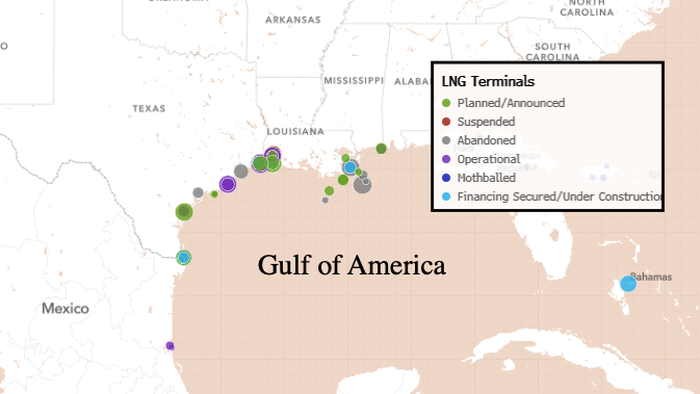

That is bullish for U.S. LNG exporters along the Gulf of America, where waters remain calm and the risk of major conflict is low.

But as Criterion Research President, James Bevan, details below, these U.S. export hubs are already operating at or near full capacity.

The Strike

Iranian ballistic missiles struck Qatar’s Ras Laffan Industrial City in two waves over 12 hours on March 18-19, causing extensive damage to both the Shell-QatarEnergy Pearl GTL facility and the LNG complex. The Pearl GTL complex, the world’s largest gas-to-liquids facility processing approximately 1.6 Bcf/d of feed gas, was hit first on Wednesday evening. A second wave early Thursday struck LNG facilities directly. QatarEnergy confirmed sizeable fires and extensive further damage but did not specify which trains were affected.

QatarEnergy Statement on Missile Attacks on its LNG Facilities

In addition to the previous attack on Ras Laffan Industrial City on Wednesday 18 March 2026 that resulted in extensive damage to the Pearl GTL (Gas-to-Liquids) facility, QatarEnergy confirms that in the early hours…

— QatarEnergy (@qatarenergy) March 19, 2026

Qatar’s Ministry of Defence reported five ballistic missiles were fired at the complex; four were intercepted, and the fifth struck home. No casualties were reported, and all personnel had been evacuated hours earlier after the IRGC issued explicit warnings naming Ras Laffan among five energy complexes across Saudi Arabia, the UAE, and Qatar that it designated as targets. The fires have been showing up on NASA satellite flyovers, affirming the situation on-site.

The attacks were retaliation for Israeli strikes on Iran’s South Pars gas field. The IRGC named five energy complexes across Saudi Arabia, the UAE, and Qatar as targets. Key developments across the Gulf:

-

Saudi Arabia intercepted missiles targeting Riyadh and the eastern region

-

UAE shut its Habshan gas facility and Bab oil and gas field after falling debris from intercepts

-

Brent crude briefly touched $119/bbl before settling around $114; TTF jumped 16%+ to 63.7 euros/MWh

-

Strait of Hormuz remains effectively closed to tanker traffic

-

Trump warned the U.S. would destroy the entirety of South Pars if Iran strikes Qatar’s LNG facilities again

What’s Offline

Ras Laffan houses roughly 77 MTPA of liquefaction capacity, approximately 20% of global LNG supply. That capacity had already been offline since March 2, when earlier Iranian drone strikes forced a halt and triggered force majeure. The market initially treated the shutdown as temporary. Confirmed physical damage from this week’s strikes changes the calculus:

-

Prior restart estimates assumed 2 weeks to resume + 2 weeks to stabilize

-

Structural damage to LNG trains, if confirmed, could push the timeline to months or years

-

Pearl GTL alone may face a multi-year outage if reports of destroyed air separation units prove accurate

US LNG: Running Full Out Into the Gap

While roughly a fifth of global LNG supply sits offline and damaged in Qatar, US export terminals are running at or near maximum capacity.

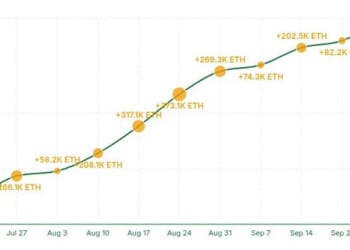

Per Criterion Research, total US LNG feed gas flows surged to 19,982 MMcf/d on March 19, recovering sharply from a brief dip the prior day. The current weekly average of approximately 19,883 MMcf/d represents a step-up from last week’s 19,731 MMcf/d, and forward nominations suggest flows could climb toward 20,234 MMcf/d in the days ahead as commissioning activity progresses at multiple facilities.

The Math

Qatar’s 77 MTPA offline equates to roughly 10.2 Bcf/d removed from the global market. US terminals at ~20 Bcf/d cannot physically replace it. No combination of non-Qatari suppliers can.

Goldman Sachs estimated a one-month Hormuz halt could drive TTF toward 74 euros/MWh, the threshold that triggered demand destruction during the 2022 European energy crisis. We are now well past one month of disruption, with infrastructure damage escalating. European storage sits at ~29% full, down 20+ points YoY, with injection season starting in April. In Asia, Qatar supplied ~53% of India’s LNG imports, 72% of Bangladesh’s, and 99% of Pakistan’s.

Cheniere just kicked off the commissioning process for CCL Stage 3 Train 6, requesting FERC approval to introduce propane to the thermal oxidizer and hot oil furnace. Fuel gas and feedgas requests should follow in the coming weeks. Commercial ops expected by late May or early…

— Criterion Research (@PipelineFlows) March 18, 2026

Every incremental MTPA of new US capacity, whether from Golden Pass, Corpus Christi Stage 3, or Plaquemines, now carries outsized significance. The commissioning trajectory at these facilities is no longer a corporate milestone. It is a global supply security question.