Life, Liberty, Property #138: Washington’s Millionaires-Tax Doom Loop

Forward this issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

- Washington’s Millionaires-Tax Doom Loop

- Video of the Week: Space Mirrors to Save Solar Power? | The Climate Realism Show #194

- A ‘Positively Soviet’ Bipartisan Housing Bill

Space is limited and it’s coming soon, so act now!

Washington’s Millionaires-Tax Doom Loop

The state of Washington has passed a “millionaires tax” that Gov. Bob Ferguson has said he will sign.

Washington had no income tax before this. The legislation imposes a tax of 9.9 percent of income on households earning more than $1 million per year, and it would be assessed on all income above that number. The bill’s sponsors said the tax will raise more than $3 billion a year.

The revenue will be directed to a grab bag of interest groups, King 5 Media Group reports:

The tax would help fund public education, early learning, childcare, healthcare, and other services, according to supporters of the legislation. It would be used to eliminate sales tax on grooming and hygiene products. It would allow the state to exempt small businesses grossing less than $250,000 from the Business & Occupation Tax starting in 2029.

The tax would also allow for the expansion of the Working Families Tax Credit—a sales tax rebate for families with low to moderate income levels.

Finally, 5% of the revenue would be distributed to counties across the state to help pay for public defense and “strengthen public safety.”

Proponents of the bill stressed that the tax would hit less than half of 1 percent of the state’s population, affecting about 30,000 households, King 5 reports. Soon there will be much fewer than 30,000 such households in the state, you can be sure. People with incomes above a million dollars a year are not exactly chained to the soil like Russian serfs.

Republicans in the state argued that the tax will drive businesses away, which has already begun. On Tuesday, the day the Washington House passed the bill (which the state Senate had already passed), former Starbucks CEO Howard Schultz announced that he was leaving Seattle and moving to Florida, which has no income tax. Schultz had lived in Seattle for 44 years.

California has shown where this is headed, Business Insider reports:

Schultz’s move follows that of several wealthy Californians who have purchased homes in the Sunshine State.

Over the past few months, entities tied to Google cofounders Larry Page and Sergey Brin purchased homes in Miami, spending more than $180 million and $50 million, respectively. This month, Meta CEO Mark Zuckerberg broke Miami records by buying a home on Indian Creek for $170 million.

The three centibillionaires purchased their homes amid a proposed wealth tax in California that, if passed, would subject residents with a net worth of more than $1 billion to a one-time 5% tax on their wealth.

Amazon founder and CEO Jeff Bezos left the state of Washington in 2024 after lawmakers enacted a capital gains tax of 7 percent in 2022, saving himself at least $610 million in state tax last year alone. While living in Washington in 2022 and 2023, Bezos refrained from selling any stocks, so the state did not even get the hotly desired tax revenue while he was still there.

The state of Washington has decided to emulate the formerly Golden State and establish a doom loop. The state is pushing out productive people with high taxation, crime, public disorder, hostility to wealth, and a general descent into barbarism, all in the name of equality, fairness, and other sweet-sounding ideals that always end up in disaster.

Seattle is already struggling with an exodus of productive people and their replacement with people of much lower incomes, which will drive down tax revenues and make it increasingly difficult to pay for needed services and reverse the social, economic, and political decay that is driving businesses out, as I wrote last week about Portland, Oregon.

Opponents of the millionaires tax also argued that it is unconstitutional because it is not a flat tax, and they will challenge it in court. In addition, they argued, the tax will not stay limited to millionaires for long if the courts let it stand, King 5 reports:

Sen. Chris Gildon, R-Puyallup, is the Republican leader on the Senate Ways and Means Committee. Gildon said the proposal is a “tax on everyone, with a temporary exemption for the first $1 million.”

“Lawmakers could adjust the threshold at any time with a simple majority vote, and history shows they will,” Gildon said in a prepared statement.

That is exactly what happened when the federal government established an income tax in 1913 after passage of the Sixteenth Amendment.

At first, only 1 percent to 2 percent of the nation’s population paid the tax. It was publicized and designed as a tax on the wealthy, starting with a tax of 1 percent on income of $20,000, the equivalent of more than $660,000 today, and a top rate of 7 percent on incomes over $500,000, the equivalent of $16.5 million in today’s dollars. That went into effect in 1913, and those rates lasted for all of three years before the government doubled the rate in the lowest bracket and more than doubled the top rate to 15 percent, in 1916.

In 1917, the government raised the top rate to 67 percent, and then shoved it up to 77 percent in 1918, while cutting in half the income threshold for reaching the top rate. Presidents Warren Harding and Calvin Coolidge reduced the top rates below 50 percent and then to 25 percent, and President Franklin Roosevelt reversed that by signing tax hikes that pushed the top rate to 94 percent by 1944. The share of the population subject to the income tax rose to about 60 percent to 70 percent of the workforce, practically overnight.

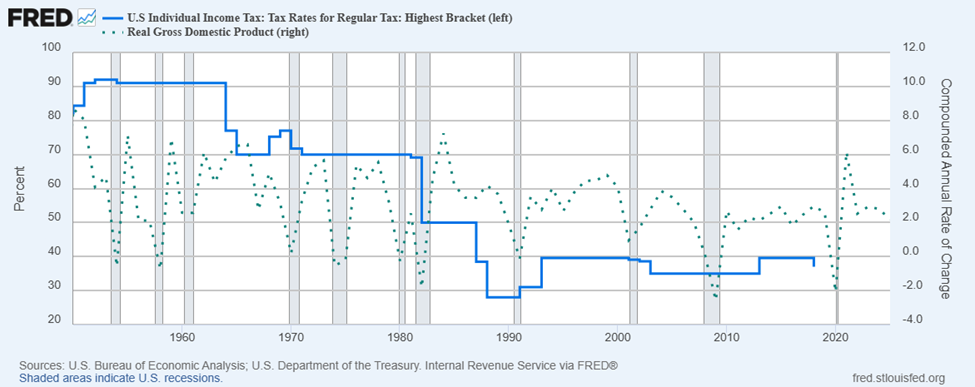

The top tax rates stayed between 70 percent and 90 percent from 1936 to 1982, when the Reagan tax cuts went into effect. Until that year, the tax rates were not indexed to inflation, thus artificially pushing people into higher tax brackets though their real incomes were not rising accordingly. The top federal income tax rate has generally been in the 30-40 percent range since then.

Source: Federal Reserve Bank of St. Louis

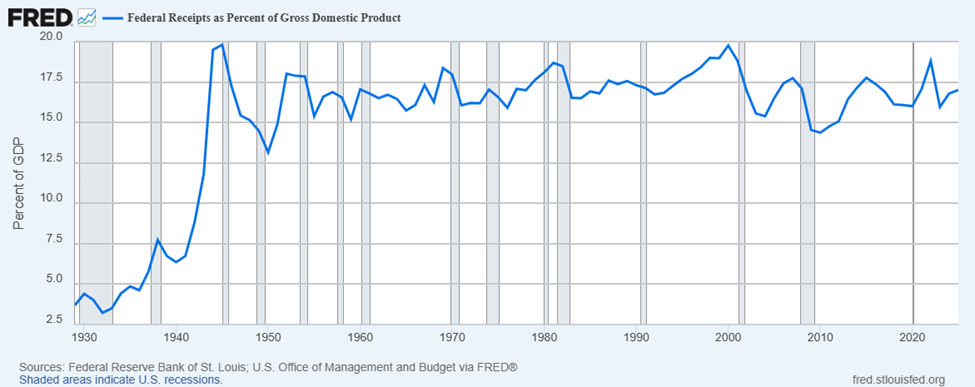

Federal revenues have remained steady as a percentage of gross domestic product for the past 80 years regardless of where the top tax rate has been set and at what income level it kicks in:

Source: Federal Reserve Bank of St. Louis

California, New York, Illinois, and other states have not learned this lesson, that there is only so much money you can squeeze out of people by force. At some point, productive people will stop earning money, hide their income, or move out altogether. That reduces tax revenues and makes it difficult for states and localities to pay for services essential to the public welfare. The state of Washington has now wrapped that doom loop around the people’s necks.

Sources: King 5 Media Group; Business Insider; Washington S.B. 6346, 2025-2026

Video of the Week

It sounds like something a Bond villain would think up. A startup wants to put giant mirrors into space to reflect sunlight back toward the Earth at night. Why would someone want to do this? To disturb the sleep of everyone on the “dark side” of the planet? No, but that would happen. To help plants grow faster and feed more people? Nope. It’s to keep giant solar power installations going after the sun goes down. This is a stupid, harmful idea, and we will explain why.

Get the latest best-seller from Heartland’s Justin Haskins!

America’s economy is teetering on the edge of disaster. Hidden beneath record stock market highs and reassuring headlines lies a fragile system riddled with debt, reckless speculation, and decades of political negligence. When the next big crash strikes—and it will—the fallout could be unlike anything we have ever experienced.

Click here to get it at Amazon.

A ‘Positively Soviet’ Bipartisan Housing Bill

In a stated bid to address the affordability crisis, the U.S. Senate passed the 21st Century ROAD to Housing Act last Thursday on an 89-9-1 vote. Nearly all the votes against the bill were from Republicans: Ted Budd (R-NC), Ted Cruz (R-TX), Ron Johnson (R-WI), Mike Lee (R-UT), Rand Paul (R-KY), Rick Scott (R-FL), Thom Tillis (R-NC), Tommy Tuberville (R-AL), and Todd Young (R-IN). The lone Democrat to vote against the bill was Brian Schatz of Hawaii.

In the debate over the bill on Tuesday morning, Majority Leader John Thune said, “This bill offers real solutions that will unlock new home construction, drive down prices, and increase the supply of affordable homes.”

The bill, introduced by Sen. Tim Scott (R-SC) and Sen. Elizabeth Warren (D-MA), follows up on President Donald Trump’s January 20 executive order directing the federal government to stop federal agencies from encouraging corporations’ purchases of residential property and to increase antitrust action against corporations that buy large quantities of single-family homes. (See Life, Liberty, Property #134, “Make Housing Affordable Again: Unlock the Supply Side.”)

The Senate bill includes some supply-side deregulation and a government efficiency measure for conservatives, plus an enormous regulatory expansion and additional spending for the left, though the Senate Committee on Banking, Housing, and Urban Affairs press release claims that it includes “no new mandatory federal spending,” suggesting that they will move current largesse into different buckets. NBC News reports:

The housing bill seeks to cut inspection delays for the Department of Housing and Urban Development by creating other avenues to satisfy requirements, while directing HUD and the Department of Agriculture to jointly coordinate environmental reviews for certain housing projects to boost construction in rural areas.

One key section, titled Homes Are For People, Not Corporations, “prohibits large institutional investors from purchasing certain single-family homes” as a way “to promote homeownership opportunities for American families, not corporations,” according to an official summary. Trump called on Congress to pass legislation banning large Wall Street firms from buying up thousands of single-family homes in his State of the Union address this year.

The Senate bill would require investors that own more than 350 single-family rental properties to sell the excess number after seven years. The Bipartisan Policy Center summarizes the provisions as follows:

- Restricts the purchase of new single-family homes by large institutional investors that directly or indirectly own at least 350 single-family homes.

- Provides exemptions, including for large institutional investors seeking to purchase or build new single-family homes specifically for the rental market, but requires these properties to be sold to an individual homeowner after seven years.

Democrat senator Schatz torched the seven-year selling requirement during the debate. NBC News reports,

Schatz said the package contains many good policies but slammed the seven-year provision as “a very bizarre thing” to apply more broadly than just to hedge funds.

“There’s literally no reason for this,” Schatz said on the floor. “Anyone who wants to build housing and then provide it for rent is going to be forced to sell after seven years. … A lot of these folks are not actually in a position to sell after seven years. They will not have made their money back.”

“This is positively Soviet,” he said.

The Senate bill also includes a clause preventing the Federal Reserve from issuing a central bank digital currency through the year 2030, which was in the House bill. That is a very good provision.

The bill the chamber passed on Thursday was presented as the Senate’s version of H.R. 6644, the Housing for the 21st Century Act, though it differs from the original significantly in tone and in the restrictive seven-year provision. The House bill stressed deregulation while creating new grant programs (funded by current appropriations), as the bill summary by the nonpartisan Congressional Research Service notes (paragraph breaks added for clarity):

This bill revises federal housing programs, including by expanding available financing for affordable housing and providing grants for planning and community development activities. For example, the bill increases the statutory maximum loan limits for mortgage insurance programs administered by the Federal Housing Administration for multifamily homes and requires the use of a more specific inflation index for such loans.

The bill also increases the maximum eligible income for the Department of Housing and Urban Development’s (HUD’s) HOME Investment Partnerships Program (grants to states and localities to support housing for low-income households) and establishes a grant program to assist regional, state, and local entities with strategies to support affordable housing.

In addition, the bill exempts certain housing-related activities from the environmental review process, including certain construction, improvement, or rehabilitation of residential buildings; excludes veterans’ disability benefits from being considered as income for purposes of determining eligibility for the Veterans Affairs Supportive Housing (VASH) program; establishes a pilot program to provide grants to public housing agencies (PHAs) and other owners of federally assisted housing to test the efficacy of temperature sensors to support compliance with temperature requirements; eliminates the requirement that manufactured homes must be constructed with a permanent chassis; and authorizes HUD to conduct performance reviews of organizations that provide housing counseling services.

The bill also expands oversight of HUD and PHAs, such as by requiring PHAs to post information about contracts on their websites.

The revised bill seems to have dubious prospects for passage as-is in the House. President Donald Trump said a week ago that he will not sign any bills until the Senate passes the SAVE Act election reforms, and House Majority Leader Mike Johnson (R-LA) affirmed that understanding.

Republicans are definitely divided over the bill. Writing at The Blaze, Senior Editor Christopher Bedford argues strenuously that the House of Representatives should pass a new version that accords with the Senate’s revision. Bedford views the Senate bill as “a compromise package, as any major bill must be without a filibuster-proof majority.” Bedford characterizes institutional investors as exploitative while he correctly notes that their activities are concentrated in certain areas of the country where healthy profits are most likely to be found:

Private equity has targeted entry-level homes in fast-growing markets, paying cash and converting starter neighborhoods into permanent rental pools. The D.C. commentariat loves to point out that institutional ownership is “small” nationally. That argument obscures the real numbers. The harm is local, concentrated, and immediate—exactly where young families are trying to buy.

Wall Street’s favorite targets sit in the Sun Belt: Atlanta, where a 2024 Government Accountability Office study put the share of single-family rental homes owned by investors at 25%; Jacksonville and Tampa, where the shares stood at 21% and 15%; Charlotte at 18%; and Phoenix at 14%. Other major targets include Dallas, Indianapolis, Nashville, Orlando, and Raleigh, North Carolina.

Those states, however, have the authority to regulate their housing markets in this way. They have chosen not to do so. Bedford’s observation about the problem being “local” and “concentrated” makes the case against a nationwide clampdown on these investments. The federal law would hit not just the alleged problem areas but also the rest of the housing market, where people do not consider institutional investing to be a problem, and the latter is the great majority of the market.

That is the wrong approach, even if one accepts the dubious premise that the Interstate Commerce Clause authorizes the federal government to interfere in everything it chooses to define as a problem or just wants to troll for potential campaign contributions.

Bedford approvingly cites an accusation that investors in housing are greedy and heartless, a characterization in full accord with the opinions of blatant socialists such as Warren, Sen. Bernie Sanders (I-VT), Rep. Alexandria Ocasio-Cortez (D-NY), and Mayor Zohran Mamdani of New York City, followed by a metaphor of violence:

“The interests of the American family and corporations diverge when it comes to housing prices,” Terry Schilling, president of the American Principles Project, told the Brief. “Their interest is to increase the housing costs so they can make more money, period. And if that’s not it, they’re not a very good corporation.” (Disclosure: I serve on the APP’s board of directors.) …

“Let me put this in a way Republicans can understand,” Schilling said with a grin. “We need a preemptive strike against the corporations that are jacking up our housing prices.”

Bedford appropriately brings up a point I have made regularly here and in other writings: the United States does not have a free market nor a fundamental respect for individual liberty and federalism:

Some conservatives also argue that Washington shouldn’t interfere. But Washington already interfered—it built the corporate legal structure that shields institutional players in ways ordinary families and small businesses cannot possibly match. Pretending the market is “pure” now is a choice, not a principle.

Bedford is correct about that, and his reference to this idea is laudable. Government reform requires government action to repudiate the laws that have caused all the problems, and to remove them from the books. I hope that Bedford will join me in frequently following up on it.

The Scott-Warren legislation does not do that. While removing some federal interference, it introduces new problems. That is how these so-called reforms usually go: they pretend to reduce the government’s power while actually expanding it. The legislation is also wrong from a practical perspective: pushing investors out of the market will raise prices, not reduce them, because it will decrease investment (by shrinking the pool of potential investors) and weaken the position of buyers (because they must compete for a smaller supply of the product they want and need).

Bedford says the Senate’s bill is “exactly the kind of policy populist conservatives have wanted for years” and that it acknowledges “the difference between market orthodoxy and the American dream.”

I differ strongly. “Market orthodoxy” is the key to the American Dream. Liberty and free enterprise are central to the American Way, which is the means for individuals and families to achieve the American Dream. The way to restore the American Dream is for government to get out of the way and let Americans do things the American Way.

Sources: NBC News; GovTrack.us.; Bipartisan Policy Center; Congressional Research Service (Library of Congress); The Blaze

Important Heartland Policy Study

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Contact Us

The Heartland Institute

1933 North Meacham Road, Suite 559

Schaumburg, IL 60173

p: 312/377-4000

f: 312/277-4122

e: [email protected]

Website: Heartland.org