Inflation-weary voters are now watching gas prices spike from $2.80 to nearly $4 per gallon, an increase expected to drain hundreds of dollars from the pockets of typical families if they persist for a year or longer. Rising prices and a global economic slowdown are also reviving recession fears. And yet these costs are entirely policy-driven and preventable—the result of President Donald Trump’s decision to attack Iran without first securing oil and liquified natural gas (LNG) shipping through the Strait of Hormuz. Once again, political leaders are asking voters to accept higher prices as the necessary cost of some other policy goal.

For the past four years, inflation has consistently polled as voters’ top economic concern—and often top concern overall. Nevertheless, President Joe Biden steadfastly ignored those concerns and pursued an inflationary agenda until it cost his party the White House. Then, after Trump campaigned on ending “Bidenflation,” he re-entered the White House and immediately unleashed his own aggressively inflationary agenda—tariffs, tax cuts, spending expansions, immigration deportations, and demands for Federal Reserve rate cuts. His

And the economists’ warnings? While debating new policy proposals, any resulting inflation or recession feels like a theoretical possibility rather than a predictable outcome. Maybe tariffs will raise prices—but what if they don’t? Who can say with certainty that a tax cut and spending spree will truly ignite inflation? Or that Federal Reserve rate cuts will do the same? After all, expert warnings of inflation following President Barack Obama’s 2009 stimulus and the Fed’s expansionary policies never materialized. And there is always some economist or organization willing to argue that a given president’s agenda carries no meaningful macroeconomic downside. So why sacrifice tangible benefits for a theoretical risk of broad economic harm?

Thus, presidents invariably decide to focus on offering tangible benefits and roll the dice on any macroeconomic consequences. Have a drink with former White House economic staff—from both Republican and Democratic administrations—and many will eventually concede with frustration that economic policy is increasingly run out of the White House political and communications departments, with economic staff routinely sidelined at key moments in policymaking.

It wasn’t always this way. In 1980, President Ronald Reagan ran on rescuing the economy from Jimmy Carter’s stagflation and asked voters to judge him by the reduction in the “Misery Index” of inflation rates plus unemployment rates. Twelve years later, President Bill Clinton won the White House on the slogan, “It’s the economy, stupid” and then assembled an economic plan that dismissed most targeted constituency demands in favor of a broader blueprint to reduce deficits, lift growth, and bring down borrowing costs for families and businesses. Today, the Reagan and Clinton economies are remembered as among the most prosperous of the modern era.

Biden ignored inflation risks.

When Biden was crafting the 2021 American Rescue Plan, the economy had already been stuffed with $4 trillion in fiscal stimulus (spending hikes and tax cuts) over the prior year—including $900 billion enacted just weeks earlier—on top of substantial monetary stimulus (Federal Reserve rate cuts and money supply expansions). The economy was already reopening, and performing only $420 billion short of its $22 trillion capacity. Economists warned that in a supply-constrained economy, all that additional purchasing power would have nowhere to go but into prices. So some degree of inflation was inevitable in most countries that had responded aggressively to the pandemic. Yet passing the American Rescue Plan and shooting yet another $1.9 trillion bazooka into a $420 billion output gap was essentially pouring gasoline on the inflationary fire. That was precisely the warning from leading Democratic economists Lawrence Summers, Jason Furman, and Olivier Blanchard.

Their warnings were ignored. Democrats had a wish list of constituencies that had helped elect Biden and expected to be rewarded: tax rebates for households, bailouts for state governments, large new K-12 education grants, union bailouts. The White House reviewed the soaring price tag and the inflation warnings, and—as Biden’s chief economist Jared Bernstein, himself an ARP defender, later conceded—“sometimes your best economic argument loses to a political one.” Many Democrats also believed they had gone too small with the 2009 Obama stimulus. Another common refrain was that after President Trump’s expensive tax cuts, Democrats were under no obligation to restrain their own spending appetites.

In the end, the economists were right. The Federal Reserve concluded that fiscal stimulus added roughly 3 percentage points to an inflation rate that eventually hit 9.8 percent. (Even Biden White House economists conceded a 1-to-2 percentage point inflationary effect from the ARP.) And yet, even as inflation wreaked havoc on the economy and Democrats’ hopes of retaining Congress after the 2022 midterms, the Biden White House steadfastly refused to take its foot off the inflationary gas.

It seems politically inconceivable for a president elected on a platform of ending his predecessor’s inflation to immediately pursue his own inflationary agenda. And yet that is precisely what happened.

Sure, the president did publish a Wall Street Journal op-ed titled “My Plan for Fighting Inflation,” declaring it his “top economic priority.” But the article mostly spun the White House’s economic record and previewed no meaningful changes of direction. The administration never trimmed its inflationary agenda of new deficit spending, student loan bailouts, tariffs, new regulations, and union benefits such as “Buy American” mandates, enhanced Davis-Bacon prevailing wage rules, and maintaining the Jones Act, which raises shipping costs. Far from being a genuine top priority, inflation concerns were repeatedly cast aside to deliver more tangible benefits to Democratic constituencies—college students, unions, and tariff-protected industries.

Rather than treat the resulting inflation as an economic problem to solve, the White House treated it as a communications problem to deflect. First, officials repeatedly denied that prices were rising at all, before labeling such increases as “transitory.” When that became untenable, Democrats pivoted to “Putin’s price hike” (backdated to before the Ukraine war had even begun). This was followed by the “Greedflation” narrative that American businesses, after several decades of apparent restraint, had suddenly decided in 2021 to become greedy and aggressively raise prices. For all the endless spin, at no point did the Biden White House feel it necessary to unveil or implement a serious plan to address the top voter concern of its presidency. And while the White House cycled through various scapegoats, prices rose a total of 20 percent, costing families more than $10,000.

This denial and spin forced the Federal Reserve to do the heavy lifting through significantly higher interest rates—slowing the economy and burdening businesses and homeowners with higher borrowing costs. It also effectively cost Democrats the White House in 2024.

Trump adopts Bidenomics.

It seems politically inconceivable for a president elected on a platform of ending his predecessor’s inflation to immediately pursue his own inflationary agenda. And yet that is precisely what happened. The centerpiece has been aggressive tariffs that—despite implausible White House denials that they will raise prices—are specifically designed to raise import prices high enough to redirect consumers toward American-made products, whose prices are also elevated by imported inputs and reduced foreign competition. Federal Reserve Chairman Jerome Powell has suggested that “between a half and three-quarters” of core inflation is currently attributable to tariffs. Those price effects will likely accelerate as businesses exhaust their pre-tariff inventories and lose their ability to absorb higher costs.

The rest of Trump’s economic agenda has been similarly inflationary. A substantial tax cut bill handed out new benefits while increasing spending in key areas. Immigration restrictions and deportations are likely to create worker shortages and force up wages and costs in industries dominated by immigrants. And while the Federal Reserve would typically be expected to maintain higher interest rates to mute these inflationary effects, Trump has waged an aggressive campaign to force Federal Reserve interest rates downward. All of these policies benefit some portion of Trump’s constituency, yet risk worsening inflation.

Rather than confront voters’ persistent inflation concerns, Trump has mocked affordability complaints and falsely asserted that “prices are plummeting downward.” Like Biden before him, Trump has treated inflation as a messaging problem to be solved with spin and partisan base-rallying rather than policy adjustments. Also like Biden, the Trump administration has even begun scapegoating “corporate greed.” At no point has the Trump team pared back its inflationary agenda.

Much of the White House spin has centered on low gas prices as proof that inflation is solved. Which makes it all the more difficult to understand how the administration could launch an air war against Iran without apparently planning for the effects on global oil markets. Accounts differ on whether the White House had any strategy for managing oil flows through the Strait of Hormuz. What is clear is that such concerns did not prevent the strikes from proceeding, nor did they produce any effective plan to contain the resulting oil price and market disruption now hitting American families. The White House did not even notably accelerate purchases for the Strategic Petroleum Reserve during the war-planning period. There is little evidence that gas prices were on the radar of Trump or his top advisers when planning a war in the Middle East.

Americans are consequently being told, once again, to accept higher prices in service of other goals. For Biden, those goals were spending, bailouts, tariffs, and pro-union policies. For Trump, they are tariffs, tax cuts, additional spending, immigration restrictions, lower Federal Reserve interest rates—and now, war with Iran.

The broader economic cost.

Today’s politicians are happy to declare their opposition to inflation—and to blame the opposing party for driving it higher. But when presidents are actually crafting an agenda, tangible benefits to key constituencies—tariffs, industry protections, tax cuts, spending expansions, even wars—invariably take precedence over more amorphous, intangible concerns about whether such policies worsen the broader economy or reignite inflation. White Houses no longer seem to trust macroeconomic forecasting and appear to believe that any resulting harm can simply be messaged away. After all, who can definitively prove that any particular policy caused the inflation or dampened the economic growth?

Politicians treat the broader economy the same way they treat soaring government debt. All else equal, they would prefer low deficits. But few are willing to sacrifice their expensive agenda over economic risks that may not even materialize—and can always be blamed on the other party. Politically, tangible benefits defeat intangible threats.

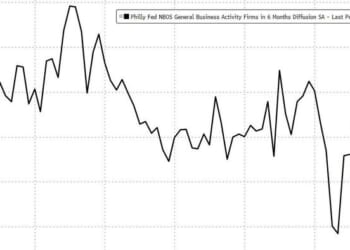

Except the “intangible” broader economy has suffered real, measurable consequences. Long-term economic growth projections have fallen to an anemic 1.8 percent annually. Inflation remains above the Federal Reserve’s target with significant upside risk. Elevated interest rates are suppressing business investment, hammering first-time homebuyers, and trapping current homeowners in place by making it too costly to surrender their lower mortgage rates. Consumer confidence is at a 12-year low, job growth is falling towards zero, and manufacturing—the very industry tariffs are supposed to benefit—is shedding jobs and output.

President Trump and congressional Republicans appear headed toward a significant midterm defeat, with the economy and inflation once again ranking as top voter priorities. But inflation-weary voters may wonder what it will take for the next group of political leaders to finally listen to their demands and stop sacrificing price stability for other pet priorities.