Forwardthis issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

IN THIS ISSUE:

WSJ Article Finds Sanity in Trump’s Economic Policies

Video of the Week: Do We Need An AI Bill Of Rights? – In The Tank #516

The Trouble with MAHA

Hot off the presses! Our latest Best-Seller

WSJ Article Finds Sanity in Trump’s Economic Policies

Prominent economists have consistently dismissed President Donald Trump’s ideas on money and trade as ill-informed and foolish. Trump is brash and opinionated and generally unsophisticated in his arguments, yet the conventional wisdom on President Ronald Reagan was equally dismissive. Democrats and the press (which was a redundancy even then) referred to Reagan as an “amiable dunce” and assumed that their view of him was dispositive.

Except for a few supply-siders on Reagan’s team, nearly all economists expressed the conviction that the 1981 cuts would balloon the deficit. The deficit did rise, but because Congress raised spending radically: federal tax revenues rose as a result of the Reagan tax cuts, from $593 billion in 1981 to $666.4 billion in 1985 and $909.2 billion in 1988.

Federal revenue grew by 53 percent over eight years as the Reagan tax cuts unleashed a stunning amount of economic growth across the United States. Unfortunately, Congress and Reagan raised spending by an even higher percentage, 58 percent, from $543 billion in 1981 to $860 billion in 1988. Ever since then, commentators have regularly said that Reagan’s tax cuts increased the budget deficit. Nothing could be further from the truth.

The big issue in the 1980s was stagflation, a phenomenon that the reigning, Keynesian economic orthodoxy could not make sense of. Since Trump’s election in 2016, the big concerns have been wage stagnation and economic inequality. As good Keynesians, Democrats have consistently pushed for greater government spending—which sparked a truly terrifying increase in the federal debt and, accompanied by massive increases in regulation during the Biden presidency, suppressed the private sector’s production of goods and services.

Conventional Reaganite Republicans in the 2000s have pushed for lower taxes and less regulation, which are both good things to do. They have not, however, held the line on spending, just like Reagan. Trump has signed big budgets, though except for the Covid year the great majority of the spending increases were locked-in rises in entitlements which were expanded giddily during the Obama and Biden years.

The one thing both parties have agreed on since the Reagan years is free trade. (It is important to note that Reagan was not a doctrinaire free-trader: he approved of tariffs as a reaction to unfair trade practices, and he imposed major tariffs on Japan, including extremely high duties on imported Japanese automobiles.) Trump’s rejection of all the Democrats’ Keynesian policies and of Reaganite Republicans’ devotion to free trade has resulted in derogation from economists and analysts on both sides of the political divide.

That explains why The Wall Street Journal has been as critical of Trump’s economic policies as any of the overtly left-leaning legacy media outlets. It is interesting, then, that the Journal published a very fair and sophisticated analysis of Trump’s economic policies last week. In what might at first seem to be faint praise, Hoover Institution senior fellow and Cato Institute scholar John H. Cochrane writes, “The policy world is aghast, but President Trump’s desires for monetary affairs aren’t as crazy as conventional wisdom portrays.”

“Not that crazy” is the equivalent of radical praise for Trump in a mainstream media outlet. Cochrane, who is an innovative economic thinker himself (and hence has much experience at being dismissed by conventional minds), has been anything but a cheerleader for Trump in the past. In his WSJ op-ed, Cochrane analyzes what Trump is trying to do and gives fair consideration to whether the president’s policies are plausible attempts at accomplishing those goals.

Trump is pursuing three main objectives, Cochrane writes:

I see three broad desires: Interest rates should be lower, in part to lower interest costs on the debt. The Federal Reserve should be less independent, subject to more democratic accountability. And “exorbitant privilege” or “reserve currency status”—that the world wants to hold our money and buy our debt, sending us goods in return—damages the U.S.

Looking at “the standard response” of critics regarding each of these aims, Cochrane finds their arguments fall short. The claim that “[l]ower interest rates will quickly lead to more inflation,” for example, does not fit the historical facts, Cochrane notes:

That inflation went nowhere over a decade of near-zero interest rates, and three decades in Japan, seems to confirm this theoretical view that inflation is stable with a fixed interest rate—and that inflation will eventually follow higher or lower interest rates. Yes, low interest rates that financed large deficits contributed to inflation in many countries. But if a government doesn’t expand fiscal policy, the record is less clear. Yes, low interest rates in response to “supply” shocks, such as in the 1970s and 2020s, coincided with inflation. But the exact effect of low rates, and of other fiscal and nonfiscal responses, is also murky.

Regarding Trump’s criticisms of the Federal Reserve (Fed), Cochrane is equally openminded, finding much merit in the president’s position. The Fed has intervened into the nation’s economy far beyond what Congress appears to have intended, to the point where the central bank is acting as a legislative and executive body on its own, and it has been spectacularly incompetent at executing its expansive ambitions. Cochrane writes,

The Fed has vastly expanded its scope of operations, propping up asset prices, monetizing debt, channeling credit, directing banks how to invest, straying into climate and inequality, and denying whole business models such as narrow banks and segregated accounts. These actions are political and cross over into fiscal policy and credit allocation. It has had no reckoning with its great institutional failures, including 10% inflation and repeated bailouts.

Like any government-created agency, public-private or otherwise, the Fed should have to face some reckoning and accountability for errors and overreach, Cochrane notes:

Independence isn’t an absolute virtue. Our constitutional order doesn’t include completely independent officials who can print money and regulate banks as they wish. It is reasonable to discuss reform. Either the Fed must be more “democratically accountable,” which is the same thing as “politically influenced” when the other party is in power, or it must be reformed to a narrow, enforced and accountable mandate so it can remain independent. As a small-government advocate, I favor the latter. But limited-government reforms are out of fashion and perhaps unrealistic. In any case, simply pulling up the drawbridge, hoisting the “independence” flag, and pouring boiling scorn on the barbarians at the gate isn’t a viable response.

Finally, Cochrane echoes Trump’s concerns about the major, long-term macroeconomic domestic U.S. effects of the dollar’s status as the global reserve currency. The dollar’s use as a reserve currency creates immense demand for dollars. That increases the value of the dollar, making foreign goods and services cheaper for us to purchase and rendering U.S. goods and services more expensive for other countries. A nation supplying the world’s reserve currency runs perpetual trade deficits, exchanging fiat money for real goods and services.

It looks like money for nothing. Just print and spend. A nation with this status has two choices of how to spend that reserve-currency bounty: invest it in domestic, private-sector production of goods and services, or consume it in current spending, with high government spending an additional powerfully damaging factor.

Britain is a cautionary example of this, having lost the pound’s centuries-old reserve-currency status and the nation’s global empire after a couple of decades of government overspending early in the twentieth century.

In a highly astute comparison, Cochrane notes that two other once-prosperous European nations ravaged their economies by wasting their temporary international currency power on current consumption instead of investment:

In the consensus view, if the world wants our money and debt so much that we can just print it, send it abroad, and get consumer goods in return, the proper answer is a nice thank-you note. But one must admit this strategy has had downsides. Spain and Portugal minted the world’s money when they found gold and silver in the Americas and used it to buy consumer goods. Their industries languished and then ended up poor. Money is a form of the “resource curse” that befalls many producers of oil and other vital commodities. Switzerland refuses the world’s offer and remains productive.

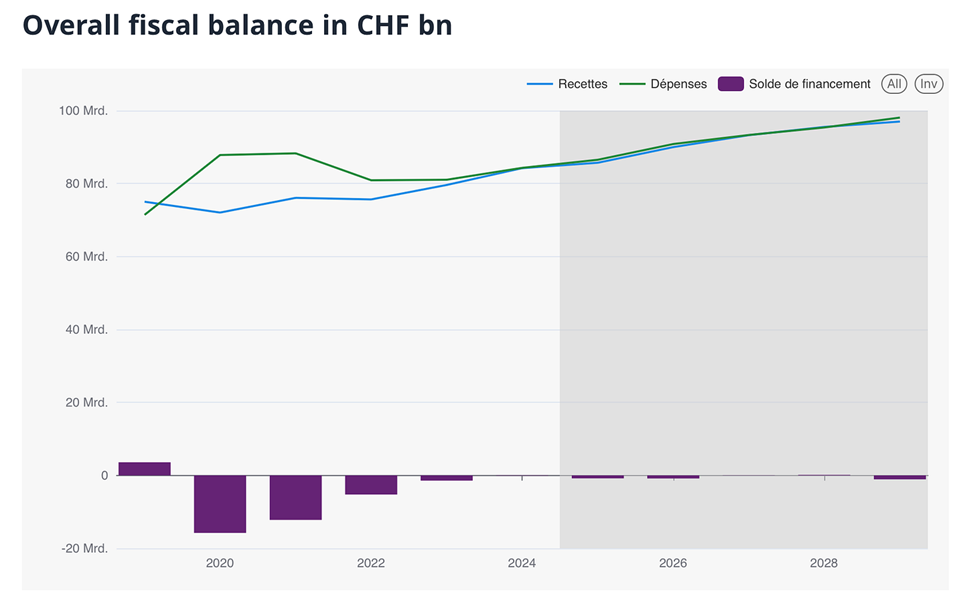

Cochrane’s October 13, 2025 article on Switzerland’s monetary and fiscal policies does a great job of explaining the great benefits of that country’s refusal to accept the temptation to spend a strong-currency bounty (not even reserve currency status) on current consumption during and after the Covid lockdowns:

Why did Switzerland have so little inflation, and why did inflation go away so quickly? Well, if you’re a blog follower you know I think the recent inflation in the US and Europe came from unfunded fiscal deficits.

Here is recent Swiss fiscal policy. The worst deficit in the pandemic was under 20 billion, or about 3% of GDP. The US by contrast hit 25% of GDP deficit. The budget went quickly back to balance—total balance not just primary balance. Debt is a tiny 16.8% of GDP. Yes, 16.8, not 168. The SNB literally could not provide 420 billion reserves by buying domestic government debt.

Heartland Institute Policy Advisor Barry S. Poulson has written extensively on the Swiss government’s constitutionally mandated “debt brake” and how it ensures that government spending does not continually outpace economic growth as it does in other countries:

The Swiss “debt brake” is a rule that requires the legislature to bring expenditures into balance with revenue in the near term. The rule caps the rate of growth in federal spending at the long-term rate of growth in the economy. If deficits are incurred, the legislature must use surplus revenue to offset deficits in the near term.

The effectiveness of the Swiss “debt brake” was revealed in recent years when expenditures did in fact exceed the spending cap. Over the past two years, the Swiss legislature cut spending on a wide range of government services and is now reviewing future budgets to ensure that they are in compliance with the spending cap.

The Swiss anticipate more cost-cutting in the future because of higher spending on pensions for older adults, children and defense. The U.S. can learn several important lessons from the experience with second-generation fiscal rules in Switzerland and other European countries.

The policy applies also at the canton (state) and local levels. The debt brake ensures that Switzerland does not run big trade deficits and spend down revenue from what Cochrane calls the “extraordinary privilege” the nation’s strong currency creates. That has been a continual theme of Trump over the years and especially in his second presidential term. Trump’s thinking on this subject is based on a simple but powerfully true premise about the long-term effects of spending and saving, Cochrane acknowledges in his Substack article:

I am also softening a bit my standard economists’ disparagement of the school that says trade deficits and exorbitant privilege are bad, such as the Mar-a-Lago Accord and Stephen Miran’s essay. After all, the Swiss don’t want exorbitant privilege either.

Your mother told you that it is good to save. That’s what running a trade surplus and capital account deficit means to a country: Work, earn more than you consume, accumulate foreign securities, so that in a rainy day or when you get old you can turn it around, cash in those chips, and enjoy consumption without working so hard. Borrowing to finance consumption is dangerous. Trade deficits that finance consumption mean eventually turning around and working hard to put things on boats in return for our pieces of paper, or at least promising to do so.

Now, trade deficits used to finance investment in high-productivity projects are fine, just as borrowing to invest in a good business is a good idea. The main problem with our trade deficits is that they financed government spending which subsidized consumption. Still, [Trump’s] mercantilist disparagement of a persistent overall trade deficit is not totally misplaced.

That is some truly eloquent economic writing and reflects a laudable willingness to apply fundamental truths to current controversies without trying to force reality into one’s preferred policy positions.

Cochrane states the same point succinctly in his Journal article, and it merits quoting here because of its immense importance:

Countries that run perpetual trade deficits to finance consumption, borrowing abroad to do so, eventually must pay back the debt. Saving and investing rather than borrowing and consuming is good for an economy as it is for a family.

The central problem in our case—and in much of history—is the bounty was consumed rather than invested. That choice flows from government deficits to finance consumption, and legal, tax and regulatory barriers that make private investment less profitable.

Cochrane does not endorse Trump’s economic plans, concentrating instead on how the government’s policies affect economic fundamentals, as he explains in his Grumpy Economist article on Switzerland:

[I]t’s not so easy as the Mar-a-Lago crowd would have it. Trade deficit financed investment also needs good high marginal product projects, which Portugal might have lacked, and the US might have lacked too. And the Mar-a-Lago interventions seem unwise to me. Figure out why the US is consuming and not investing seems the answer.

But it was brought home to me that the Swiss do not want to print the world’s money and rake in consumption goods either, and I cannot say they are unwise for doing so.

That is the right approach: seek ever-greater understanding of causes and effects, and then base policies on what you observe. In another article at The Grumpy Economist, Cochrane summarizes the reaction to Trump’s economic policy statements as overwrought, tendentious, dismissive, and incurious:

My fellow macroeconomists, mostly Trump-hating Democrats or Never-Trump Republicans, are mostly treating this monetary policy news as if it is completely delusional. Unlike the economic effects of tariffs, though, that’s not really honest. We would do better to have a respectful debate.

Cochrane’s call for an honest, unbiased debate about Trump’s crazy (to conventional thinkers) and innovative (to sympathetic minds) fiscal and monetary policy prescriptions identifies something that everyone should have done from the start. It is unlikely to happen now, for the same reasons that it did not happen in the first place. Nonetheless, Cochrane’s dismantling of some contemporary economic shibboleths clears the way for a rational, fact-based discussion should anyone want to engage in it.

The AI Revolution is happening at an incredible speed. New AI products, like OpenAI’s Sora 2, continue to push the envelope and blur the lines between reality and fabrication. Should there be a framework—an “AI Bill of Rights”—to protect individuals from algorithmic abuse, data manipulation, and government or corporate overreach?

The Trouble with MAHA

Vaccination pioneer Dr. Robert Malone identifies great contradictions between the Make America Healthy Again (MAHA) and Make America Great Again (MAGA) movements in an interesting and informative article at The Misesian from this past June, which I’ve just run across and think is very important to current discussions of health care policy. Malone is the inventor of mRNA vaccination technology, DNA vaccination, and multiple nonviral DNA and RNA/mRNA delivery technologies.

The distinguished doctor-scientist finds both the origins and current aims of MAHA and MAGA to be fundamentally at odds with one another: “they have different constituencies and different drivers,” Malone writes. The two movements “resolve into proregulatory big government initiatives versus promotion of deregulation and small government,” Malone observes. “In theory, Make America Great Again is more aligned with libertarian principles. Make America Healthy Again, in my opinion, is much more aligned with big government and regulation.”

MAHA originated on the left and is still on that side of the political divide, with HHS Secretary Robert F. Kennedy Jr., a lifelong Democrat, as its current political spearhead, Malone writes:

For this discussion, I’m primarily concerned with the MAHA directives within the government, but MAHA is much bigger than that. I just want to make that key point: it’s bigger than Robert F. Kennedy Jr. It’s been going on for years. And in many ways, it was Calley and Casey Means, through a series of interviews, including, I think, four hits on Tucker and one on Rogan, that really brought this to the fore. In their logic, for example, Big Food and Big Ag have been contaminated with the money from Philip Morris that was required to be moved out of Big Tobacco and was moved into Big Food. And in Calley and Casey Means’s thesis, Big Food and Big Ag applied the marketing strategies and approach that had characterized Big Tobacco, making for an addicted consumer base, as a great business model. When you see a lot of the activities that are associated with Big Food and Big Ag, it’s hard to escape the underlying truth of that metaphor. …

Now, MAHA as we know it now has emerged mainly from the left out of frustration with the Democratic Party’s corruption and rejection, and it has embraced the center-right.

The center-right has largely returned the compliment, embracing MAHA, Malone notes. (Malone himself was “very close” to Kennedy’s political campaign team last year, he acknowledges.) “So, MAHA originates from the left, but the appeal crosses all party lines. Who does not want to be more healthy?” Malone writes.

MAHA remains a movement of the left and looks directly to the federal government to solve the American people’s health problems, Malone notes:

At its core, MAHA is predominantly proregulation. Let that sink in. The logic is that we must use regulatory authority to improve transparency and eliminate that which leads to unhealthy outcomes. Examples include drugs with side effects that, when considered in whole, do not have a strongly favorable risk-benefit ratio, an example being glyphosate (or Roundup) contamination of our grain and soybeans. Of course, recently, we have the removal of food dyes. However, there’s also a deregulatory aspect to the MAHA movement. For example, is unpasteurized milk really a health risk? What health-promoting properties are associated with unpasteurized milk?

Similarly, there is the move toward backyard poultry and eating locally slaughtered grass-fed beef, and reexamination of the widespread US policy of fluoridating municipal water supplies. These are all pushes against big government mandates. There’s also an investigational research aspect. For example, what are the drivers behind the explosion of autism, obesity, and other childhood chronic diseases? This is the explicit mandate coming from Donald Trump through the MAHA Commission. To date, the MAHA movement has primarily focused on things that big government can do to promote improved health. This is where MAHA is going currently.

The “deregulatory” elements Malone cites are actually calls for the federal government to override state and local laws restricting various food-production and sales practices and other health-affecting goods and services. These proposals would not reduce government power but expand it and concentrate it on the federal level. Though Malone does not make that distinction in his article, I think my recognition of it buttresses his case.

MAHA proponents oppose countless past decisions by the Food and Drug Administration to approve the manufacture, sale, and use of various products, along with federal agencies’ decisions to expand the schedule of recommended vaccines for children, Malone notes. Those very decisions, however, and the agencies’ refusal to revisit them, represent the very danger MAHA is courting in pressing for greater federal government intervention. Malone writes,

The whole structure of the approval process is driven by approving the thing in front of them right now, not going back and looking at whether or not there’ve been interactions between any of these drugs or compounds or vaccines, whether or not that decision was a good decision, or whether or not they missed some long-term safety signal because they were only looking at short-term data. It’s not done because that is kind of fundamental to the nature of bureaucracy. Once they make a decision, they don’t ever want to revisit it. It becomes locked in stone, and they move forward from that.

A derivative of this is that behind the potential of the MAHA initiative to improve our lives, and, importantly, improve childhood chronic disease, is the threat that if this gets institutionalized and bureaucratized, it will morph into another overbearing set of state mandates. There is no way to avoid that.

MAHA is nothing like MAGA. It would lead to an enormous further expansion of federal government power and the removal of any remaining decision-making ability from the American people and their doctors in health matters. Malone urges his readers to push for serious limits on MAHA:

And, basically, my talk here is a plea to you folks, who are kind of at the tip of the spear concerning bureaucracy and the administrative state. We need you. We need your intellectual input to help set the boundaries and parameters around the MAHA initiative. It’s not being done right now. Nobody’s talking about what the proper boundary should be. We seem to have a consensus that this is necessary. That actually is debatable, but that is the current consensus. But no one is talking about what happens once the administrative state gets its teeth into this initiative.

Malone provides much additional useful information about MAHA issues and how the “modern public health enterprise” “seeks to optimize collective health outcomes rather than optimizing health opportunities coupled with respect for individual autonomy and choice—which is what I advocate.” The article is well worth reading in its entirety.

‘The CSDDD is the greatest threat to America’s sovereignty since the fall of the Soviet Union.’

Contact Us

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org