You’re reading Dispatch Markets, a weekly newsletter on economics featuring Scott Lincicome, Megan McArdle, Kyla Scanlon, Karl Smith, and Marian Tupy. To access more Dispatch reporting and analysis, become a member today.

Editor’s Note: Regular readers of Capitolism—our weekly newsletter analyzing economic policy, trade, and regulation—might remember that, back in January, its author Scott Lincicome announced he needed to cut back a bit due to his increasing work obligations and his “intense desire to stay somewhat sane and rested.” We understood, of course—and didn’t want to learn what a “somewhat less sane” Scott looked like—but fact-based, rigorous economic analysis remained a top institutional priority, particularly as partisans of all stripes seem to be sprinting away from first principles that lifted hundreds of millions out of poverty and unlocked unprecedented economic growth and quality-of-life increases over the course of American history.

We’ve assembled a roster of some of the brightest economic writers and thinkers in the country, and are thrilled to be offering their analysis as a part of The Dispatch bundle.

Scott will keep up his every-other-week cadence—we can’t let him get too well-rested—but the off weeks will now be authored by one Megan, Karl, Kyla, or Marian. Expect topics to range from how the Trump administration’s tariffs are rippling through the economy to the challenges facing the Federal Reserve to AI and the future of work. Underlying it all, though, will be intellectual honesty, respect for economic realities, and a willingness to grapple with tradeoffs. We’ll send the first few editions of Dispatch Markets widely—we’re grateful that it’s unlocked in partnership with the U.S. Chamber of Commerce—but check your newsletter preferences to ensure you are subscribed.

Without further ado, here’s Scott on the joy that is Tax Day …

For most people reading this newsletter, yesterday was Tax Day—the day when Americans officially settle up with Uncle Sam for the past calendar year and, in great American tradition, complain publicly about it. Like past Tax Days, the days leading up to this one featured plenty of commentary on how much we’re paying in taxes, how much some of us are getting back, and—for the libertarians out there, at least—how profligate federal spending continues to far outpace whatever eye-watering amount the federal government takes in. Given that Congress passed a big tax bill last year in the One Big Beautiful Bill Act (OBBBA), there’s surely lots to say on all these things and more.

Yet there’s another big tax we all paid today—one that didn’t go to the U.S. Treasury or get nearly the ink it deserves: the hundreds of billions of dollars in time and money spent on simply complying with a federal tax code that’s now more than 4 million words long. This tax doesn’t just cost us time and money; it reduces economic growth, encourages cheating, and breeds cronyism.

And, unfortunately, it just got worse.

U.S. tax complexity is increasingly costly.

Most people who have done their own taxes understand at some basic level that the U.S. system is weirdly, impenetrably complex. The late Donald Rumsfeld’s annual letter to the IRS—telling the agency up front that “I have absolutely no idea whether our tax returns and our tax payments are accurate”—annually goes viral for this very reason. (If you haven’t read it, you should: It’s really funny.)

Advertisement

Stay ahead of the policies shaping free enterprise and impacting American business.

Get the U.S. Chamber’s free newsletter for insights on the economic policy, workforce trends, and regulatory landscape that affect businesses and markets.

By subscribing you agree to receive communications from the U.S. Chamber of Commerce.

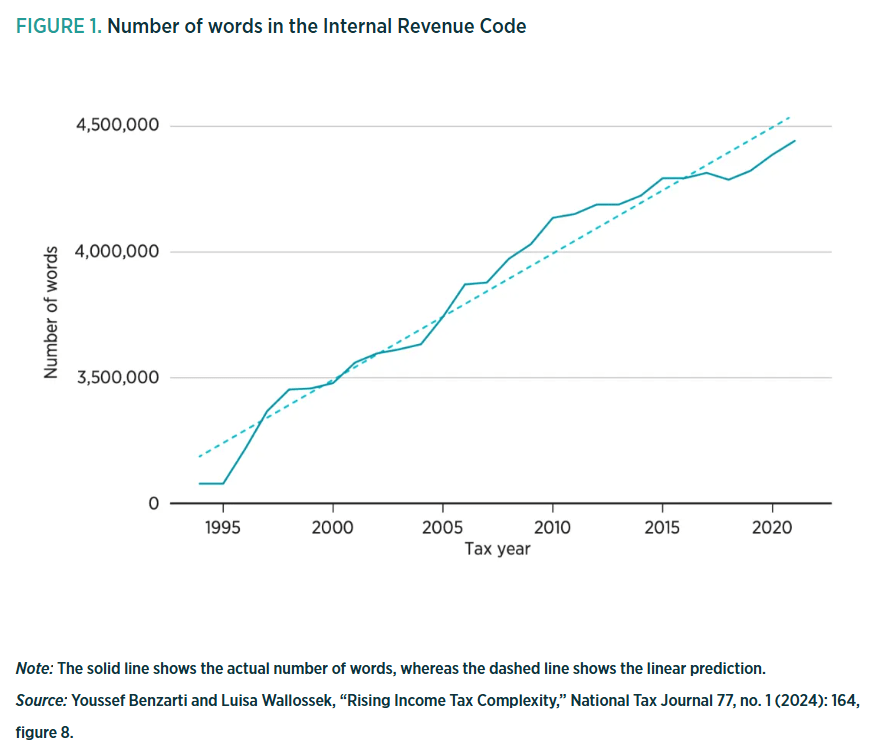

Yet the sheer magnitude of U.S. tax complexity is no laughing matter—nor are its economic costs—and the problem has worsened since Rummy started sending his famous letters. Recent research finds, for example, that the Internal Revenue Code had grown to 4.3 million words by 2021—up roughly 40 percent over the last three decades and far longer than the five other countries the authors examined (France, Germany, Switzerland, Canada, and Morocco). The next wordiest tax code, in fact, was in France—at a mere 1.25 million words. The statutory text, moreover, is supplemented by regulations and IRS guidance that dwarf the code itself.

That study’s authors add that, while a higher word count might not necessarily mean a more complex tax code, it tracks alternative measures of complexity in the United States. For example, there were 103 income tax sections in 1954 and 736 by 2005. Between 1991 and 2012, meanwhile, the code’s subdivisions and cross-references increased from around 50,000 to nearly 70,000. Data on the number of forms we have to file, as well as on Google searches for tax filing assistance, further support the conclusion that the U.S. tax code is an increasingly impenetrable mess. The tax code is also constantly changing: According to a 2012 report from the National Taxpayer Advocate, Congress amended the Internal Revenue Code more than 4,430 times between 2001 and 2010 alone—an average of more than one change per day, including weekends.

As detailed in a new Mercatus Center report, the tax code’s expansion has been driven by the proliferation of so-called “tax expenditures”—government spending via special tax deductions, credits, exclusions, and exemptions. The child tax credit is a common (and well-intended) example, but there are many others. And there’s been a 35 percent increase in these provisions—from roughly 130 to approximately 175—since 2000 alone.

Every tax expenditure program comes with its own rules, requirements, prohibitions, and exceptions, and Congress is constantly changing the terms to address perceived shortcomings, expand or limit beneficiaries, and make other tweaks. Throw in related case law, and the end result is 50 times longer than War and Peace—and, believe it or not, probably more boring.

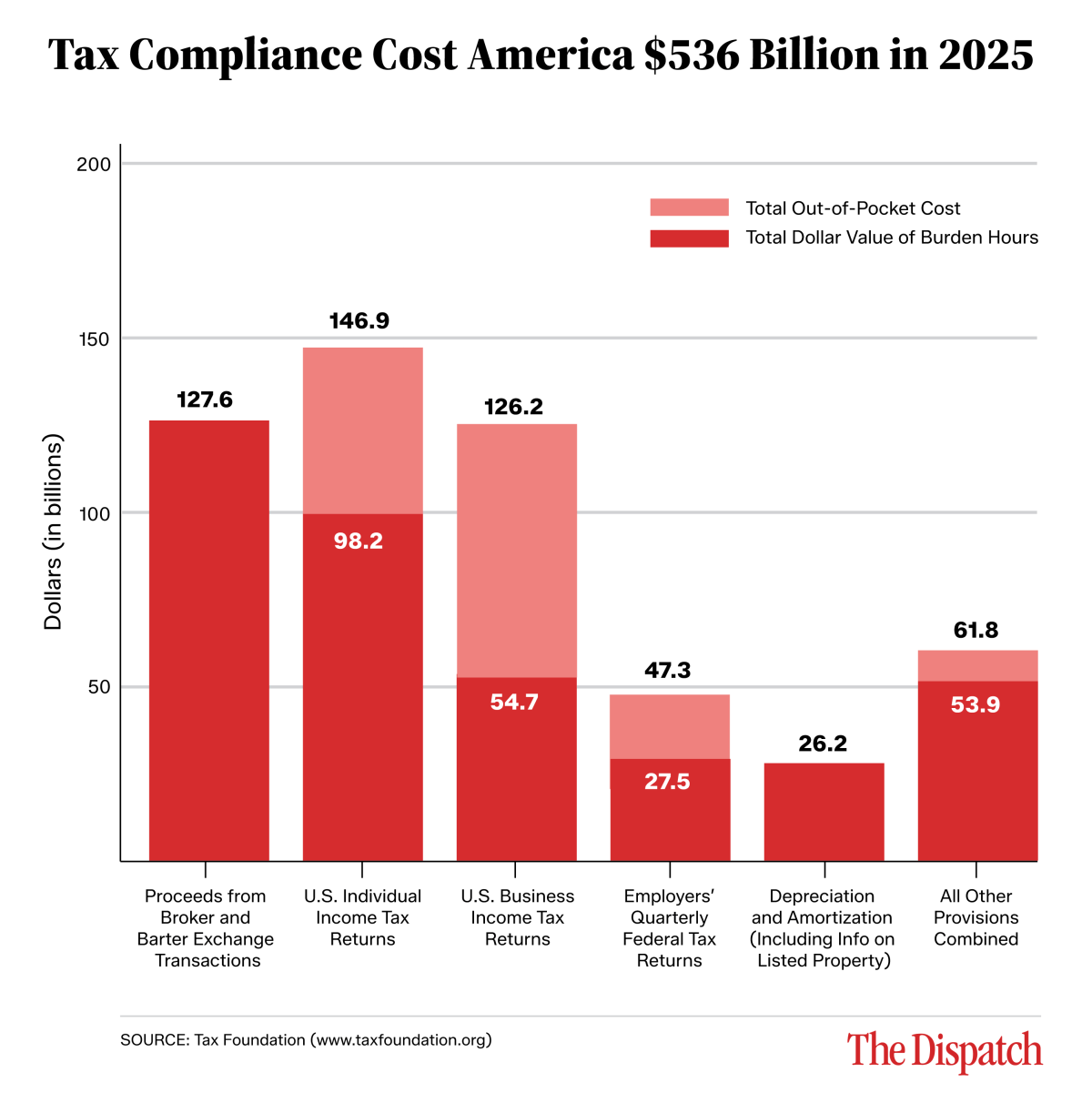

The economic costs of this complexity are enormous. For starters, there’s simply the time and money we have to spend complying with an ever-growing and always-changing tax system. According to the Tax Foundation, compliance with the federal tax code cost Americans roughly $536 billion in 2024-2025—or nearly 1.7 percent of 2025 gross domestic product. They conservatively derive this number from two sources: First, there’s $148 billion in out-of-pocket costs for software, tax preparers, and accountants. Second, there’s time: Using a reasonable hourly wage, the 7.1 billion hours Americans spent complying with the tax code translates to roughly $388 billion in lost productivity.

To put these figures in context, $536 billion is more than the corporate income tax will generate this year, around twice as much as Trump’s tariffs will raise, and more than 43 times the IRS budget. The 7.1 billion hours spent complying, meanwhile, is the equivalent to 3.4 million full-time American workers—almost the population of Los Angeles—doing nothing but tax paperwork for a full year. The National Taxpayers Union puts the total compliance burden at $464 billion for 2024, with the average filer spending 13 hours and $290 just to pay his taxes. For many Americans (including me—sigh), tax filing demands multiple spring weekends doing unpaid labor just so we can cut the government another check. (Yes, I am bitter.)

The Mercatus report finds extensive but less visible economic damage beyond the compliance headaches. Increased complexity reduces economic growth by discouraging entrepreneurship (it’s a clear barrier to entry) and encouraging businesses and individuals to make decisions based on obtaining favorable tax treatment instead of maximizing genuine productivity. A separate Mercatus paper estimated that these distortions reduce output by hundreds of billions of dollars each year. The tax code also encourages companies to spend billions on lobbying—for new tax benefits or to keep the ones they enjoy—instead of core business operations.

Tax complexity also makes it harder for people to comply with the law and encourages them to break it. When tax rules are an impossible labyrinth, errors inevitably multiply, outside auditing becomes more difficult, and scofflaws find it easier to hide in the legal weeds. As we’ve seen recently with Trump’s tariffs (see links for more), higher and more complex tax systems tend to feature more errors, avoidance and evasion. This happens with the U.S. income tax, too: Research here and abroad consistently shows a strong connection between tax complexity and evasion, avoidance, and unintentional misreporting. More such behavior also means more government resources devoted to enforcement instead of things like customer service and systems modernization.

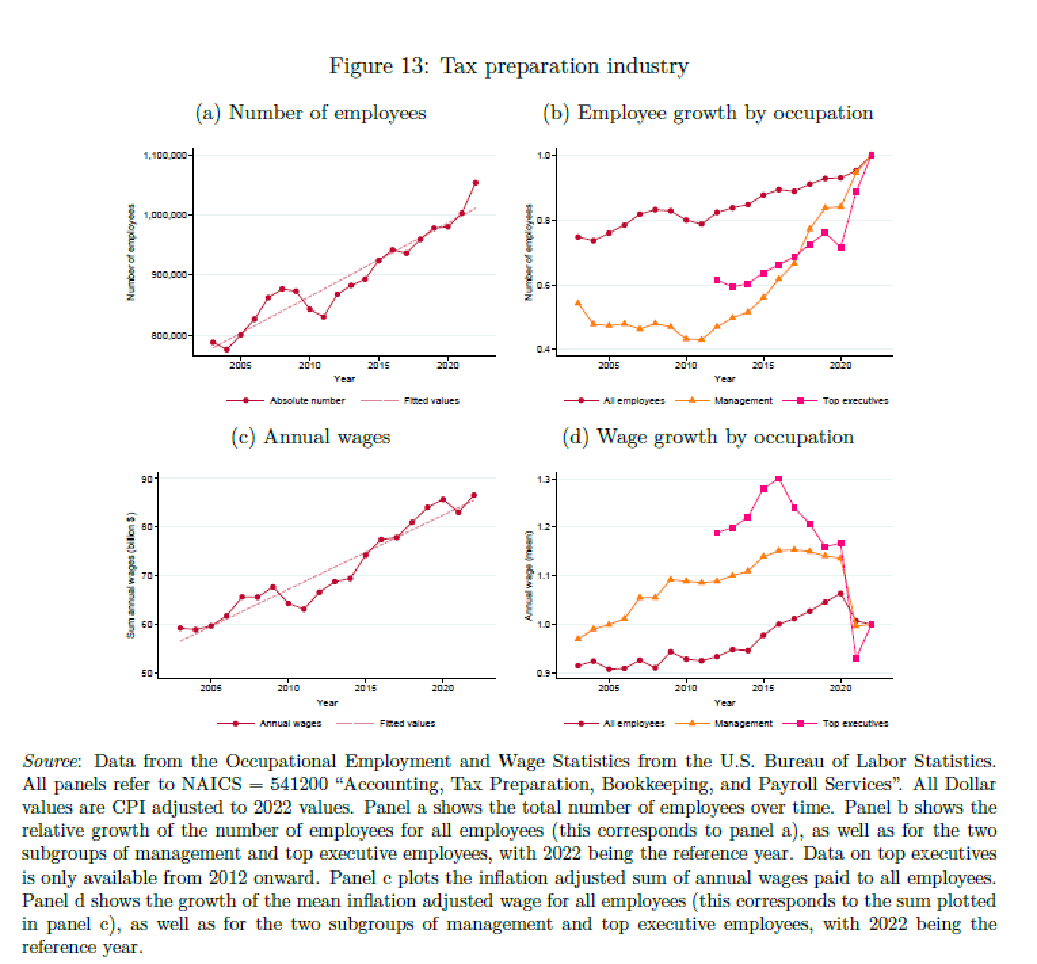

Finally, tax complexity has created an increasingly large and lucrative tax preparation industry, as well as a perverse lobbying machine that’s against simplification. Tax filing is costly for individual U.S. taxpayers but a bonanza for software companies, accountants, tax lawyers, and other pros that help us navigate the government maze (for a fee). No surprise, then, that the increase in U.S. tax complexity has coincided with remarkable growth in the tax preparation industry:

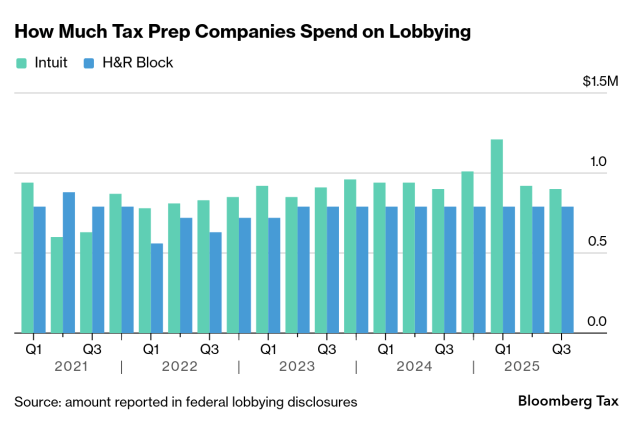

Also unsurprisingly, the industry has fought efforts to simplify the system. Most notably, Turbo Tax parent Intuit and accounting giant H&R Block have spent tens of millions of dollars lobbying against efforts to make doing our taxes faster and easier.

The merits of some of those reform efforts are debatable, but the industry’s motivation surely isn’t.

The one big beautiful mess.

Despite the harms of increased U.S. tax complexity, last year’s One Big Beautiful Bill Act (OBBBA) represents a depressing step backward from the simplifying Tax Cuts and Jobs Act. Instead of simply extending the TCJA, Congress used the OBBBA to implement a slate of targeted tax expenditures and carve-outs—each with its own eligibility rules, phaseouts, income caps, documentation requirements, and sunset dates—that make the tax code harder to navigate and administer.

The quadrupling of the state and local tax (SALT) deduction cap, from $10,000 to $40,000, not only was bad economic policy (it should be zero) but also undermined the TCJA’s most important simplification achievement: raising the standard deduction and instituting a relatively low SALT cap so that far fewer filers would have the financial incentive to itemize. Now under the OBBBA, millions of Americans (mostly upper-middle-income households) are again itemizing their deductions—documenting every expense (state/local taxes, charitable contributions, mortgage interest, medical costs, etc.) and filing more paperwork—to reduce their tax burden. This process not only means more time and money spent on taxes but also more opportunities for error, more incentive to fudge the numbers, and more exposure to an IRS audit.

The Tax Foundation preliminarily estimates that, compared to a 2025 baseline, the OBBBA will translate to roughly 6.9 million additional tax itemizers and a $1.7 billion increase in tax compliance costs this year, largely due to increasing the SALT deduction cap. The provision also ends in 2029, meaning Americans might have to rewire their financial planning again in just a few years—if, of course, blue state politicians and real estate lobbyists don’t get it extended further. Regardless, the SALT cap mess is precisely the kind of complicated and uncertain provision that makes the U.S. tax code such a burden.

A slew of other OBBBA carve-outs makes matters even worse. For example:

- As my Cato colleague Adam Michel wrote earlier this year, the “no tax on tips” and “no tax on overtime” deductions are each a witches’ brew of eligibility criteria, time and income limitations, and elaborate new IRS rules—and thus a “case study in how the tax code gets more complicated.”

- The new deduction for car loan interest — up to $10,000 annually for domestically assembled vehicles—requires additional paperwork (VIN verification, etc.) and phases out as income increases. (It’s also terrible economics.)

- The additional standard deduction for seniors, which allows eligible seniors to claim an additional $6,000 (single) to $12,000 (married), requires age verification, income calculations, and phase-out determinations.

- The new “Trump Accounts” for children, Michel explains separately, “offer only limited additional tax benefits compared to existing personal savings options and are wrapped in complex rules that will discourage widespread use.” They also add yet another tax-advantaged, special-purpose savings vehicle to the dozen-plus we already have (IRAs, Roth IRAs, 401(k)s, 529s, Coverdell ESAs, ABLE accounts, HSAs, FSAs, and on and on).

These and other provisions, such as requirements related to child tax credits, “foreign entities of concern” (FEOC), and partially repealed green energy subsidies, will increase tax complexity and compliance costs. The IRS estimates the OBBBA’s new provisions will generate nearly 26 million additional compliance hours. The Yale Budget Lab calculates that just the tips, overtime, and auto loan provisions will add almost two hours to many Americans’ tax compliance burden (and one hour on average) when compared to simply extending TCJA. And tax experts from Cato, the Tax Foundation, the Tax Law Center at NYU, the Brookings Institution, AEI, and the Manhattan Institute have each warned that the OBBBA carve-outs will substantially increase tax compliance costs going forward.

Problems are already arising. Earlier this month, for example, the Wall Street Journal reported that American taxpayers appear to be substantially overreporting their tax-free overtime, and that nearly twice as many people are reporting overtime than the 2025 OBBBA budgeting expected. Some of this might simply be due to the subsidy encouraging more overtime work (itself an economic distortion), but a lot of it is probably related to complexity:

[A] big reason, tax preparers and analysts say, is that taxpayers might be claiming deductions beyond what the law allows, both intentionally and accidentally. Many workers don’t have clear information from their employers this year about whether they received overtime pay that technically qualifies for the new deduction….

[T]he definition of what kinds of overtime pay qualify is much trickier than just looking at the overtime line on a pay stub. Overtime pay only generates a tax break if it is required by the federal Fair Labor Standards Act. That means taxpayers aren’t allowed to claim the deduction for overtime worked because of state laws, agreements with employers or federal laws covering railroad and airline employees.

Adding to the problem here is that, “in the race to implement the tax cuts,” the IRS hasn’t required U.S. employers to report to the agency or to their employees whether the latter had received qualifying overtime. Without this “cornerstone of tax compliance,” they add, “confusion and fudging can take hold.” They even interviewed one local tax preparer who claimed to have lost clients because she resisted such, ahem, fudging.

It’s textbook stuff. Sigh.

To be clear, not everything in the OBBBA was bad on this front. It repealed various green energy credits from the Inflation Reduction Act, each of which had its own murky compliance burdens. And, of course, it made much of the tax-simplifying TCJA permanent. Those are genuine wins, but they’re heavily tainted by the losses—especially when compared to a simple TCJA-extending alternative.

Summing it all up.

The U.S. tax code is a costly mess. Everyone seems to know it and—save the tax preparers and subsidy lobbyists—hate it. Yet Congress can’t resist making things worse because it’s an easy way to reward friends and punish enemies.

On the bright side, it’s possible that AI will reduce our tax compliance burdens in the future—stories have proliferated this season about people using Claude, ChatGPT and other versions of the technology to save time and money on their taxes. But this is a relatively small silver lining: Not only does AI also cost money, but it’s also not available to all taxpayers or guaranteed to be error-free. It’s also only as good as its users, who will still need to ask the right questions and spend countless hours collecting and parsing whatever paperwork they feed into the machine.

AI also won’t touch the economic distortions and bad incentives that a complex tax code creates—including for more evasion—and might actually serve as an excuse to lard on even more complexity. (“My new subsidy is fine, Senator; AI will figure out the tax forms.”) Indeed, as the Tax Foundation found, 94 percent of tax returns are prepared using software and 90 percent are filed electronically, yet compliance costs keep rising because “efficiency gains from increased computing speeds have proved no match for tax complexity, which increases steadily decade after decade.” In other words, AI might help you calculate your overtime subsidy, but it won’t collect the documentation or fix the reason you need to calculate it. (And it won’t be there if the IRS ever comes knocking, either.)

The only real solution is structural tax reform. The obvious place to start—especially for a libertarian like me—is nixing most of the targeted subsidies (especially corporate welfare) now buried in the tax code. Taxes should be about efficiently raising revenue, not social or economic engineering. Yet there are also more practical, less political reforms available. As Michel lays out in a recent briefing paper, for example, complexity on the personal income side would be significantly reduced if Congress simply consolidated the six different child-related subsidies and the 15 different education credits into one benefit each, turned the dozen-plus savings and retirement programs into three (employer-based, individual IRA, and universal savings account), and eliminated all itemized deductions (and, if possible, lowering tax rates with the additional revenue). That alone would go a long way to fixing our tax complexity mess, boosting economic efficiency, too.

It wouldn’t, however, make for a great campaign soundbite, deliver targeted benefits to influential political groups, and let lobbyists and tax prep companies collect their annual $350 billion tithe via the complex system they helped create.

Markets FTW

Satellite internet is an ideal technology for a sparsely populated nation like Argentina, with 47 million people spread out over an area roughly one-third the size of the United States. But until Javier Millei took power in 2023, it was forbidden, and the country had spent $7 billion laying fiber-optic cables. But Millei opened Argentina’s market to satellite-internet providers such as Starlink, and within 18 months, 2 million Argentinians signed up. As Federico Sturzenegger, the country’s minister of deregulation, wrote recently, “Mining and energy operations became more efficient, tourism expanded (a lodge owner in Patagonia told me recently he now gets clients who come precisely because they know they can work remotely), and precision agriculture became viable by simply mounting a satellite dish on farm machinery.”

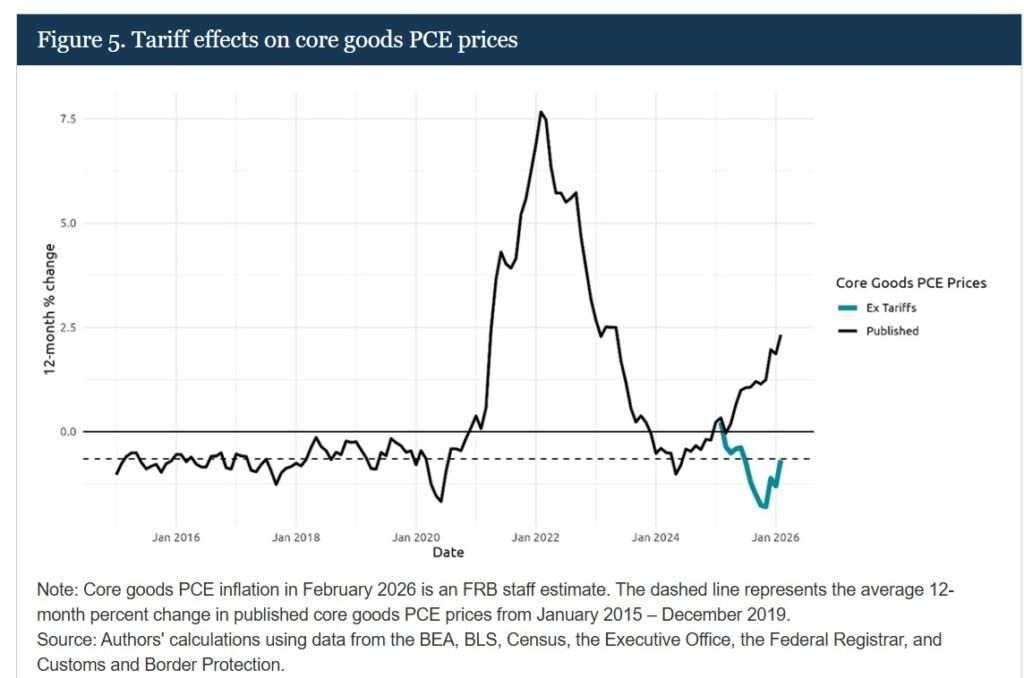

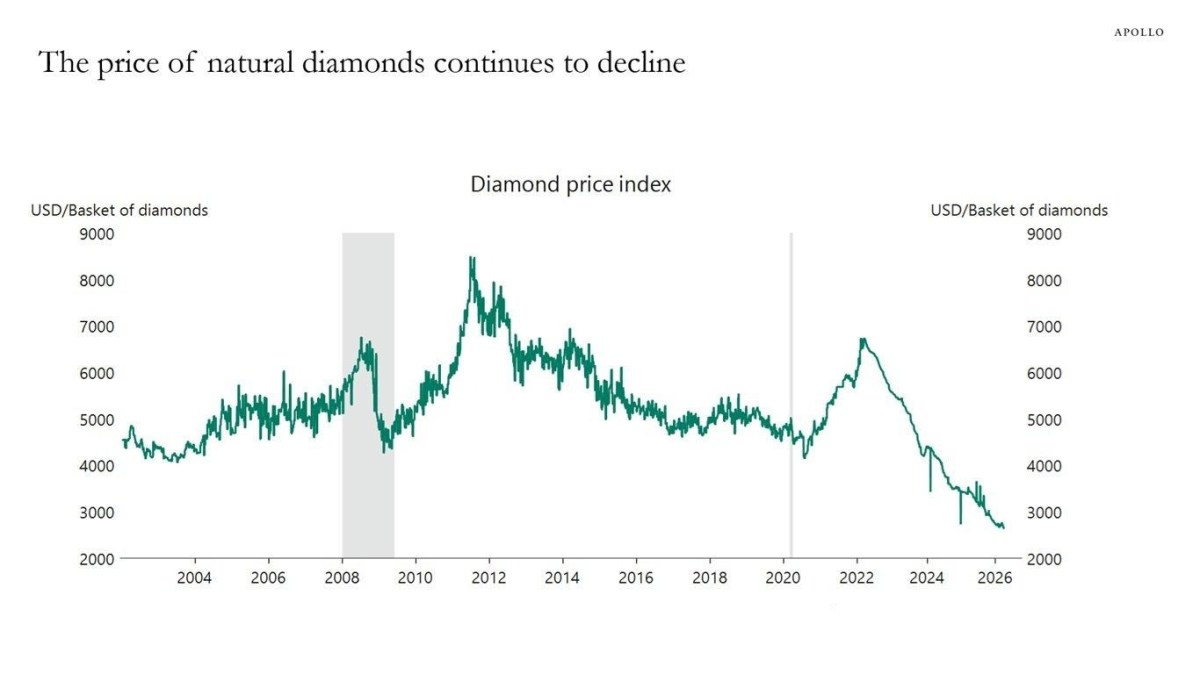

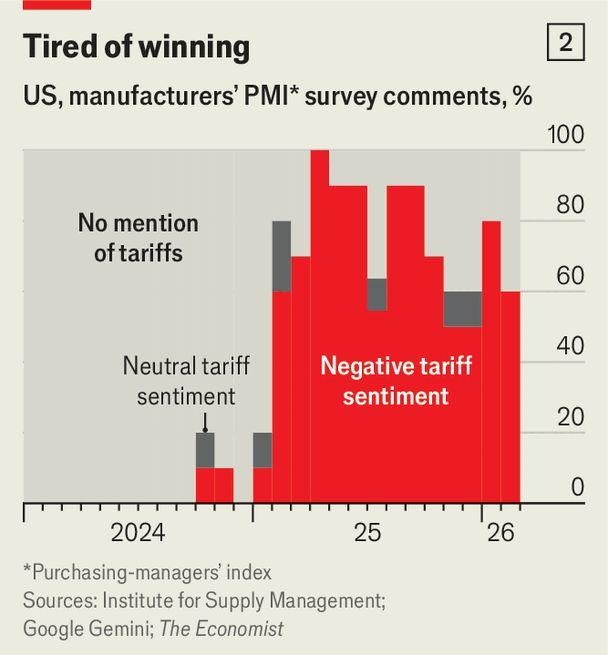

Chart(s) of the Week

What I’m Watching

Disclaimer: The opinions expressed above do not necessarily reflect those of the presenting sponsor.