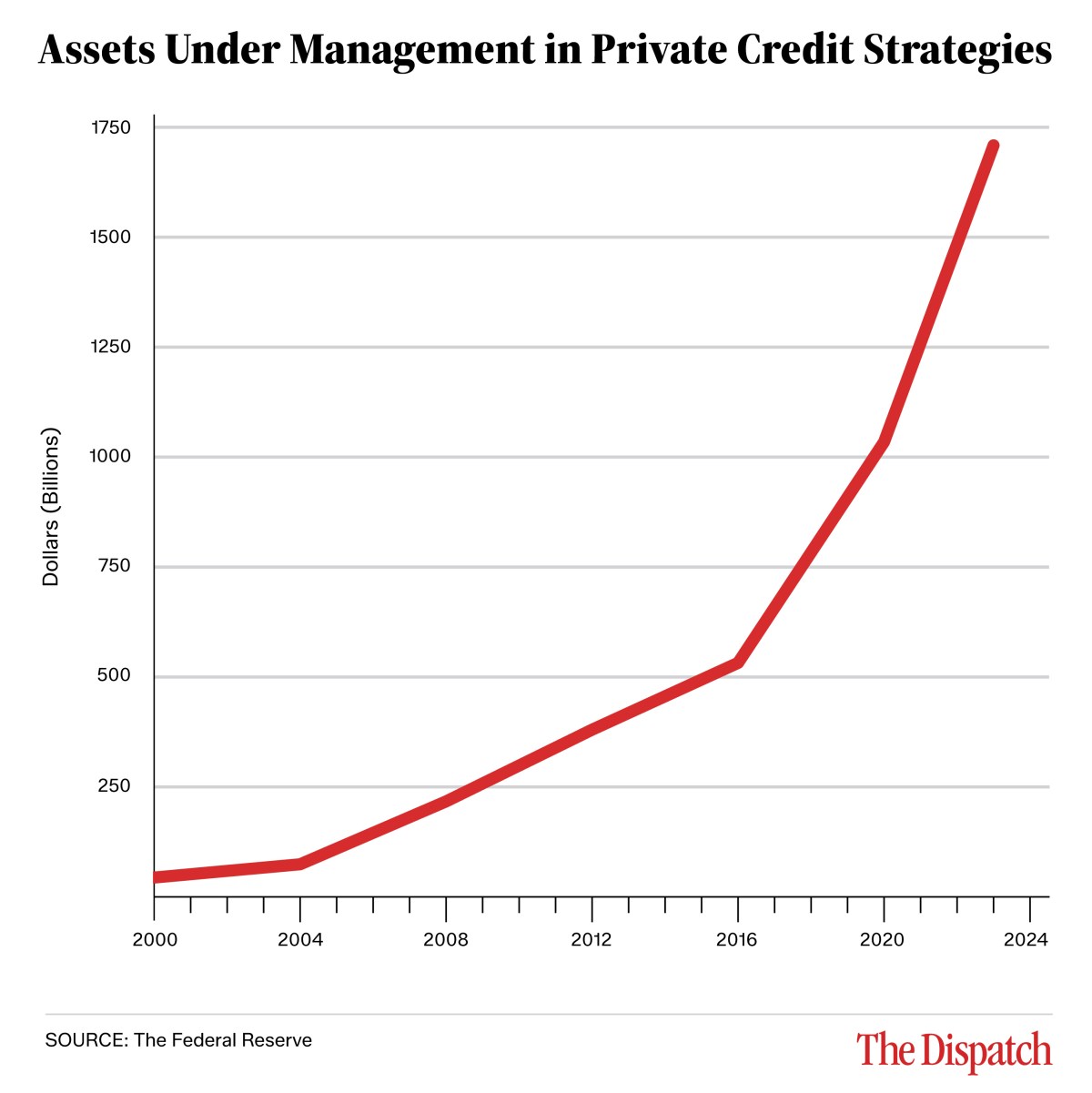

From 2010 through 2021, private credit became a mainstream option for institutional investors—pension funds, sovereign wealth funds, and insurers—attracted by returns that generally beat public credit markets. Post-2008 reforms like Basel III imposed stricter capital requirements on banks, making it significantly more expensive for them to originate riskier loans and effectively pricing them out of that segment of the market. “They more or less made it so that regional banks, and even major banks, cannot invest into riskier assets, which left a hole in the market,” Maxwell Baker, a chartered financial analyst at BTA Advisory Group, told TMD.

The rapid growth of semi-liquid investment vehicles—such as business development companies (BDCs) and interval funds—made private credit widely available to retail investors from around 2020 onward. BDC assets under management exploded from roughly $127 billion in 2020 to $451 billion by 2025, and interval fund assets under management quadrupled over the same period. Whereas traditional private capital funds require investors to lock up their assets for the lifetime of the fund (typically seven to 10 years), semi-liquid investment vehicles like BDCs and interval funds allow investors to redeem a limited portion of their holdings periodically—usually quarterly.

But in September 2025, First Brands Group and Tricolor—two companies that together used billions in private credit—declared bankruptcy, sparking concerns of a broader trend of poor underwriting and weakening credit markets. And if the bankruptcies weren’t enough to spark a sell-off, private credit’s heavy exposure to the software industry has amplified fears. Private equity firms have relied extensively on private credit to finance acquisitions of software companies, but now analysts are worried that AI may destroy these same firms.

The term “SaaSpocalypse” refers to the concern that software-as-a-service businesses will collapse as companies cancel subscriptions and replace SaaS products with AI-generated or “vibe coded” alternatives they can quickly (and cheaply) generate for their own businesses. According to banking giant UBS, as much as 35 percent of the private credit market is exposed to AI disruption risk. In a worst-case scenario, default rates could reach 15 percent—up from an already record 9.2 percent estimated default rate in 2025. “It’s very difficult to have a strong handle on what the true default rate is within private credit,” Craig Nicol, head of global credit strategy at Sona Asset Management, a London-based credit manager, told TMD. “The opacity of the asset class makes that far more challenging relative to public markets.”

Throughout the first quarter of 2026, investors have rushed to sell their positions in semi-liquid private credit funds and BDCs, in turn forcing many of those funds to restrict, or “gate,” fund redemptions. Caps on redemptions are normal. Private credit loans can’t be sold quickly to fund withdrawals, and forcing the liquidation of large portions of their portfolios at once would hurt remaining investors. But it produces alarming headlines, which push more investors toward the exits and feed fears of a broader implosion.

“What’s made things particularly bad right now is that [these redemption gates] are happening alongside all of the AI news,” one associate for a large private credit firm, who was not authorized to speak on the record, told TMD. “Those two things together have made it a very volatile time in the credit space.”

The opacity of private credit markets and their ties to the broader financial ecosystem have invited comparisons to the 2008 global financial meltdown. The exuberance over private credit echoes the pre-crisis enthusiasm for U.S. mortgage markets, and “One way that it does seem similar is the interlinking and interweaving of institutions,” Brad Lipton, director of the corporate power and financial regulation program at the Roosevelt Institute, told TMD. Many banks are lending to private credit managers under stress, and U.S. insurance companies hold significant investments in private credit.

But experts across the financial industry mostly downplayed the comparison, arguing that the global financial system is far less intertwined with private credit than it was with the mortgage-backed securities and collateralized debt obligations that triggered 2008’s emergency.

“These are asset managers, not investment banks,” Brian Judge, research director of the UC Berkeley Program on Finance and Democracy, told TMD. “They’re not funded overnight in the same way that Lehman was, so the idea that there’s going to be some sort of sudden heart attack moment, like over that weekend in September 2008, I don’t think is very likely.”

U.S. banks do lend to many of the private credit firms now under stress, but at far lower levels than their exposure to risky financial derivatives before 2008. “The exposure to private credit is relatively low from broader financial institutions,” Nicol said. “I don’t think this is a systemic problem, I don’t think what’s happening within the private credit markets is going to trigger a broader systemic crisis.” The pain, Nicol said, will be felt within the leveraged finance ecosystem itself rather than cascading into banks and insurers. Douglas Holtz-Eakin, president of the American Action Forum and a former director of the Congressional Budget Office, agreed: “They don’t rise to the level of systemic threat.”

Also, unlike 2008, the derivatives-on-derivatives architecture that amplified the mortgage crisis isn’t present. “Are we seeing CLO [collateralized loan obligations] squared? Are we seeing CLOs of CLOs? The answer is no,” Baker said.

The broader risks of tech disruption may also be having an outsized impact on markets based on irrationality. “In general, I think that the software sell-off is overblown,” Baker said. “The number of companies that will be destroyed by vibe coding solutions is much lower than the current sell-off would indicate.” Businesses with strong network effects, reliance on proprietary data, regulatory capture, or established trust in handling sensitive data—for example, in payment platforms—are unlikely to be replaced by homegrown software and could see substantial opportunities for growth.

Greater scrutiny of private credit could also prove beneficial. “There are many worrying and challenging elements facing private credit over the coming months and years, but you can also look at this as being a good thing,” Nicol said. “Downturns can correct or rectify some of the problems of the past, and you end up at a better place at the end.”

But even if the fallout stays within the financial industry, the private credit market is about to get a lot more crowded. Last week, the U.S. Department of Labor proposed a rule that would allow 401(k) plans to offer investments in alternative assets, opening up private credit and other low-liquidity assets for tens of millions of Americans. The rule followed an August 2025 executive order from President Donald Trump seeking to broaden access to alternative assets.

Some of the pressure on private credit may come from non-institutional investors who didn’t fully understand what they were buying, Scott Bishop, managing director at Presidio Wealth Partners, told TMD. When those investors try to exit and discover their money is locked up or gated, the resulting rush to redeem can intensify the very pressures that spooked them in the first place. “I’m big on the democratization of investments, but I don’t think it should be done without education,” Bishop told TMD. “I think many people are gonna be buying these things and aren’t gonna understand what they’re buying, and that’s just a problem.”

Many Americans already have meaningful exposure to private credit through their pension funds; alternative assets now make up roughly a third of public pension portfolios, double the share in 2008, and several major funds have recently increased their private credit allocations. “Hopefully this will have people start looking under the hood a little bit and doing some due diligence,” Bishop said. “Because if you’re not willing to do the due diligence, and you’re not buying with the proper expectations, you probably should just be buying stocks and bonds.”

Still, even those who are skeptical of the 2008 comparisons acknowledge that, in an opaque and fast-evolving market, the biggest risks are almost always the ones nobody has noticed.

“My crystal ball is in the shop,” Baker joked when asked whether private credit could spark the next great financial crisis. “You’re not killed by the car you see coming. You’re killed by the car you don’t.”