It’s a common tactic. A company providing internet service or car insurance offers you an enticing introductory price for the first year or two—only to raise it after that initial period expires. Since it’s a hassle to switch providers, companies bet you’ll stick with them, and they’re often right.

It turns out, private colleges seem to use this tactic as well.

Most students attending private colleges don’t pay the high “sticker prices” you see online. Over 80 percent of first-year students receive some financial aid directly from their institution, which reduces the student’s net price to what the institution thinks the student might be able or willing to pay. A generous aid offer might often lead a first-year student to choose a particular college over its competitors.

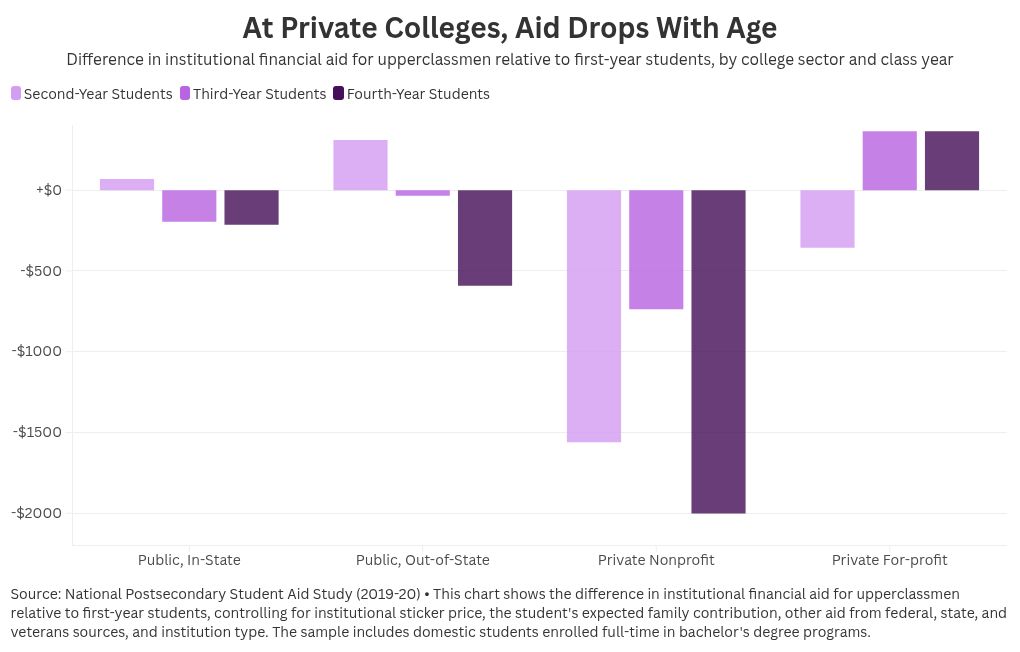

But as with internet service or car insurance, the introductory rate doesn’t seem to last—at least at private colleges. An analysis of data from the National Postsecondary Student Aid Study (NPSAS) shows that at private nonprofit institutions, upperclassmen receive far less institutional financial aid than first-year students, after controlling for other factors. (Changes in aid are not statistically significant for other institutional sectors.)

For instance, second-year students at private nonprofit schools receive over $1,500 less institutional financial aid than similarly situated first-year students (those attending similar schools with similar financial circumstances). Juniors and seniors also receive less aid. If private colleges provided the same amount of financial aid to upperclassmen as they do to similarly situated freshmen, the average student would receive $4,300 more in institutional aid over the course of her college career.

Sample sizes in NPSAS are too small to examine how financial aid changes at individual colleges, so we cannot definitively conclude that individual schools are “cutting” financial aid for upperclassmen—just that upperclassmen overall tend to receive less aid. The analysis also looks at a point in time—the 2019-20 academic year—and so doesn’t consider how changes in sticker prices may interact with reductions in aid. If a college hikes its sticker price at the same time that it cuts institutional aid for upperclassmen, the rise in net price for returning students may be even larger than implied here.

The government is starting to collect better data on how much colleges charge individual students. The Trump administration has proposed the Student Tuition and Transparency System, an amended version of a data-collection effort begun under its predecessor, which requires colleges to report tuition and institutional aid for each student. Where possible, the Education Department should calculate average net tuition each institution charges, disaggregated by class year, so students and their families know which colleges are using the bait-and-switch strategy.

An even bolder proposal, included in Rep. Virginia Foxx’s College Cost Reduction Act, would have required colleges receiving certain federal funds to offer students a “maximum total price guarantee”—that is, schools would be required to disclose the total price they will charge students over the course of their college careers, provided they finished their degrees on time. This would give students advance warning of price hikes before they even enroll, rather than leaving them to deal with surprise cuts to their financial aid once they become captive upperclassmen.

Price transparency is critical for well-functioning markets. Students should be able to understand the full price of their education before they enroll—not just a rosy first-year “introductory offer.” Better information about how colleges hike prices for upperclassmen could make the higher education market more price-competitive—and might even bring down overall prices, too.

The post The College Financial Aid Bait-and-Switch appeared first on American Enterprise Institute – AEI.